Securitization

A risk management tool used to reduce idiosyncratic risk associated with the default of individual assets

What is Securitization?

Securitization is a risk management tool used to reduce the idiosyncratic risk associated with the default of individual assets. Banks and other financial institutions use securitization to lower their risk exposure and reduce the size of their overall balance sheet.

The Securitization Process

Securitization can be best described as a two-step process:

Step 1: Packaging

The bank (or financial institution) combines multiple assets into a single “compound asset.” The return offered by the compound asset is some weighted average of the return offered by the individual assets that make up the “compound asset.”

Step 2: Sale

The bank (or financial institution) sells the “compound asset” to global capital market investors.

How Securitization Works

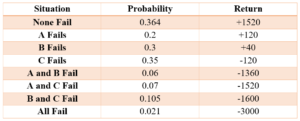

Securitization works on the assumption that the probability of several assets defaulting is lower than the probability of a single asset defaulting. It assumes that the default probability of different assets is independently distributed. The logic underlying the practice of securitization can be best described using an example.

Three investors invested $1,000 in three separate assets: Asset A, Asset B, and Asset C. They sell the assets to a bank. The expected return from the investment is (40%*1000*0.8) + (48%*1000*0.7) + (64%*1000*0.65) = 320+336+416 = $1072 = 35.73% return. However, the variance associated with the above investments is very high.

Therefore, the bank wants to remove the assets from its balance sheet. The bank creates a Compound Asset X by combining Simple Assets A, B, and C. Consider an investor who purchases $100 worth of X. The investor will receive a 50.66% rate of return. However, the investor faces considerably less risk than an individual investor who only owns one of the assets A, B, or C.

History of Securitization

Banks in the U.S. first started securitizing home mortgages in the 1970s. The initial “mortgage-backed securities” were seen as relatively safe and allowed banks to give out more mortgage loans to prospective homeowners. The practice created a housing boom in the U.S. and resulted in a tremendous increase in house prices.

In the 1980s, Wall Street investment banks extended the idea of mortgage-backed securities to other types of assets. They realized that securitization drastically increased the number of securities available in the market without raising any real economic variable. The number of securities available raised the number of potential transactions the banks could make (most banks were paid according to the number of transactions they were involved in).

The rapid deterioration in the quality of the underlying assets within the market for asset-backed securities and a general lack of government regulation were key reasons for the 2008 recession.

Additional Resources

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: