Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

An investment method in which an investor holds a call and a put option with the same maturity date, but has different strike prices

Strangle is an investment method in which an investor holds a call and a put option with the same maturity date, but has different strike prices. In a strangle strategy, a holder in effect, combines the features of both a call and a put option into a single trade, and the overall position is the net of the two options.

A strangle is a good investing strategy if the investor thinks that the underlying security is vulnerable to a large near term price movement. Executing a strangle means that the investor is betting for a large price movement upwards or downwards in the underlying stock.

Although a strangle and straddle are similar, the former involves two different strike prices. In a straddle, both call and put options share similar strike prices and expiration dates.

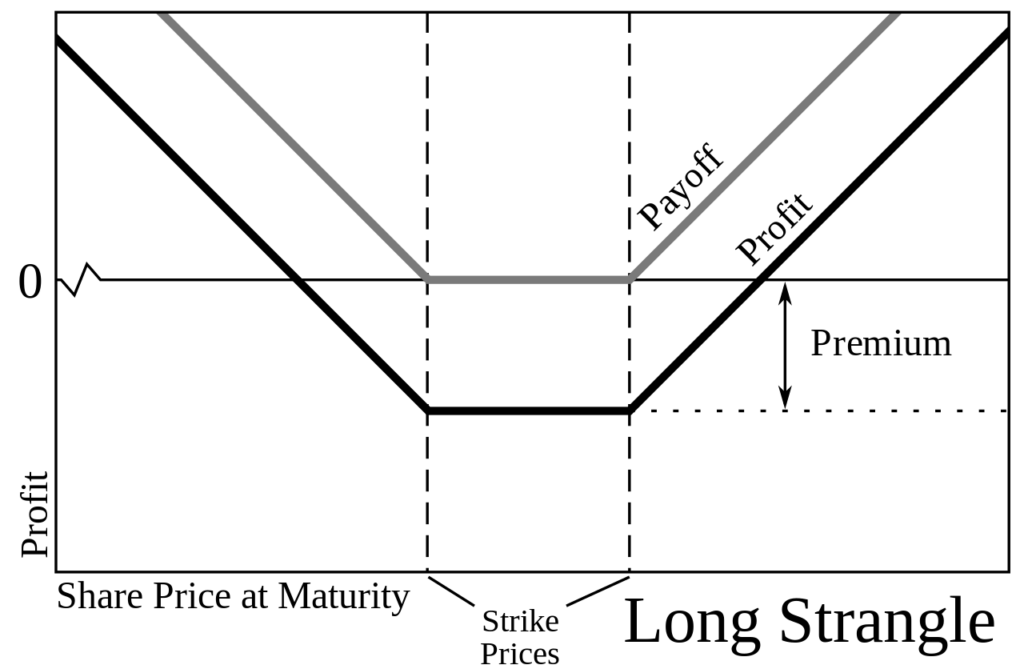

A long strangle is a popular strategy among investors, where both a long call and long put with different strike prices – but with the same expiration date – are purchased simultaneously.

Typically, the call option has a higher strike price than the current market price of the underlying stock, while the put option has a strike price that is lower than the current market price. This trading strategy has unlimited profit potential on both sides of the market. Profit is earned when the underlying asset moves beyond a break-even point in either direction.

The maximum loss is limited to the premium paid for the two options and occurs when the underlying asset, at expiration, is between the market prices. It has two break-even points – the call strike option’s market price plus the debit, and the strike price of the put option less the debit.

A long strangle is affected by the time decay’s effects. Before the expiration date, a strangle value increases with an increase in volatility and decreases with a decrease in volatility.

On the other hand, a short strangle involves the investor simultaneously selling call and put options at different market prices but with the same maturity date. The strategy is beneficial to investors since a premium is collected from the sale of both options, but only if the price of the underlying asset stays within the two strike prices and the options both expire.

Investors execute the short strangle strategy with the expectation that the underlying stock’s price will fluctuate back and forth within a range, resulting in the time decay of both options. If the price increases beyond the call options strike price or below the put options strike price the option will be exercised and the short strangle will lead to a loss.

Investors realize the maximum profit which is the net premium for writing the two options, when the underlying asset stays between the strike prices of both options. The back-and-forth fluctuation leads to a profit since the options will not be exercised by the holder of the options.

As with long strangle, short strangle has two break-even points – the sum of the premium credit collected and the short call’s market price, and the short put’s strike price less the collected premium.

A strangle and a straddle share a few characteristics because they earn profits when there are large back-and-forth movements in an underlying security. Similarly, a short straddle and short strangle are the same, with a limited profit equal to the collected premium from both options less trading costs.

Nevertheless, a long straddle involves buying both the call and put options at the same strike price, where profits can be made when prices are either up or down. The options purchased are in-the-money options.

With a long straddle, investors profit before expiration when the strike price of a call or put option exceeds the total premium paid from both sides of a trade. This implies that a straddle does not necessarily require a large price jump to be profitable.

Another difference that sets the two strategies apart is that a strangle is generally less expensive but laden with higher risk because the underlying asset must make a bigger movement to generate a profit. This is because out of the money options are purchased.

CFI offers the Capital Markets & Securities Analyst (CMSA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: