Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

An option Greek that represents the sensitivity of vega to the change of the implied volatility of an option

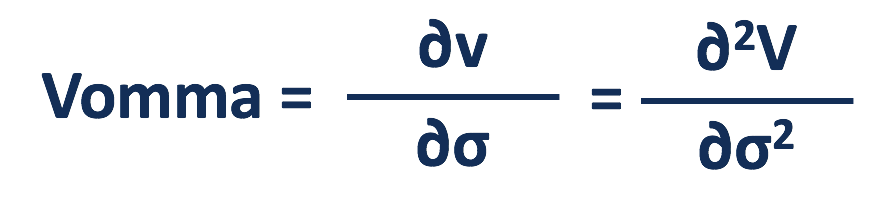

Vomma is an option Greek that represents the sensitivity of vega to the change of the implied volatility of an option. It is the second derivative of the option value to the volatility. Thus, it is also known as a second-order Greek. Other second-order Greeks include gamma, vanna, veta, and so on.

An option refers to a type of financial derivative that offers the buyer a right, instead of an obligation, to purchase the underlying asset at a pre-determined price. Businesses, individual investors, and investment institutes hold options as a method to hedge risks or generate profits.

Many factors impact the value of an option. They include the price and volatility of the underlying asset, time to execution, risk-free interest rate, and so on.

First-order Greeks are used to measure the sensitivity of option values to the changes in the factors. One of such Greeks is vega, which shows the percentage change of an option price, as the implied volatility of the underlying asset moves by 1%.

Investors and companies are more willing to buy options to hedge risks when the assets are more volatile, which leads to higher option prices, and vice versa. Therefore, for both call and put options, long positions always have a positive vega, and short positions always have a negative vega.

Second-order Greeks calculate the sensitivity of first-order Greeks to the change in the corresponding factors. Vomma is a second-order Greek that measures the change in vega responding to the change in volatility. Also known as vega convexity, vomma takes the second derivative of the value to the volatility of an option

If an option has a positive vomma, its vega increases (decreases) when the implied volatility rises (drops). If the vomma is negative, the vega increases (decreases) as the volatility drops (rises).

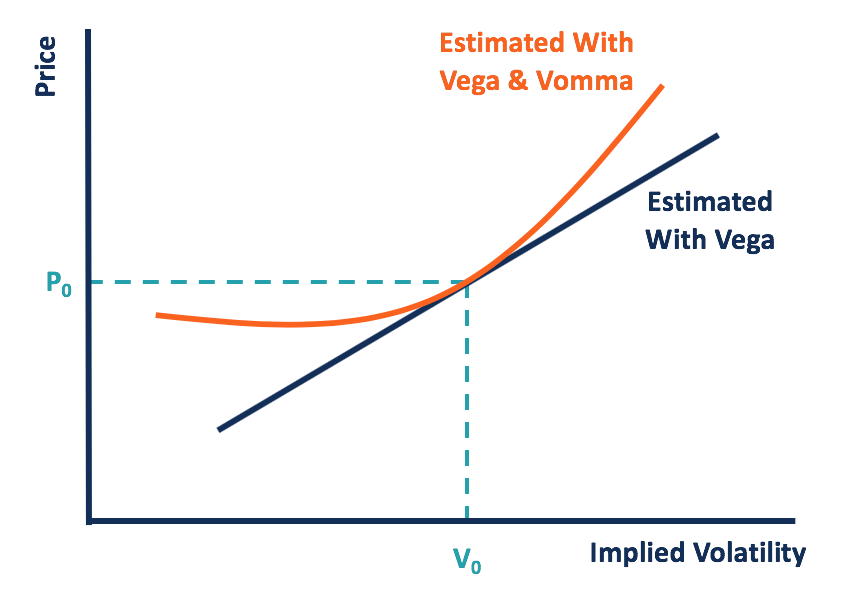

As vega assumes a linear relationship between the price and volatility of an option, vomma shows the relationship in a convex. This means that while using vega alone, larger changes in the implied volatility lead to greater gaps between the estimated price change and the actual price movement.

By combining vega and vomma, traders can estimate the price movement more accurately, especially for substantial changes in volatility.

Let’s assume that an option is positive in both vomma and vega. When the volatility rises (drops), the price increase (decrease) estimated with vega is smaller than that estimated with both vega and vomma. Thus, the price of the option is always underestimated by only using vega, compared with taking vomma into consideration.

Vomma can be calculated as the derivative of vega to implied volatility, or the second-derivative of the option value to volatility.

Where:

v = Vega

V = Option value

σ = Implied volatility of the underlying asset

Vomma calculates the percentage change of vega for each percentage change in the implied volatility.

For example, a call option has a vega of 5 and a vomma of 2. It means that when the implied volatility of the underlying asset increases by 1%, the vega will increase by 2%, and thus the option value will increase by more than 5%.

Vega and vomma are both positive for long positions and negative for short positions, no matter if it is a call or put. For long positions, vega is always positive, and the closer the option is at-the-money (ATM), the higher the vega. For short positions, vega is always negative and is lowest when the option is ATM.

Also, a non-ATM option is more like an ATM option when it has higher implied volatility. Hence, the greater the implied volatility, the higher the vega is for long positions, which indicates a positive vomma.

It is the same for short positions, that an increase in implied volatility leads to a lower vega, which indicates a negative vomma. A vega approaches its highest or lowest level at a decelerating rate, keeping other characteristics constant, the non-ATM options have higher vomma than the at-the-money ones.

Ultima measures the percentage change in vomma for each percentage change in volatility. It is a third-order Greek and can be calculated as the third derivative of the option value with respect to implied volatility.

Traders tend to seek increasing vomma in long positions and decreasing vomma in short positions. Ultima helps to determine whether the vomma will increase or decrease when volatility changes. A positive ultima indicates an increase in vomma as the volatility rises and a decrease in vomma as the volatility drops.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: