Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Beta is a financial metric used to evaluate a stock’s volatility and risk relative to the broader market — essential for understanding investment performance.

The beta (β) of an investment security (i.e., a stock) is a measurement of its volatility of returns relative to the entire market. It is used as a measure of risk and is an integral part of the Capital Asset Pricing Model (CAPM). A company with a higher beta has greater risk and also greater expected returns.

In finance, beta refers to a security’s sensitivity to systematic risk, or market risk. It tells us how much a stock’s price is likely to move in response to market changes. Beta is typically benchmarked against a broad market index, like the S&P 500.

The beta coefficient can be interpreted as follows:

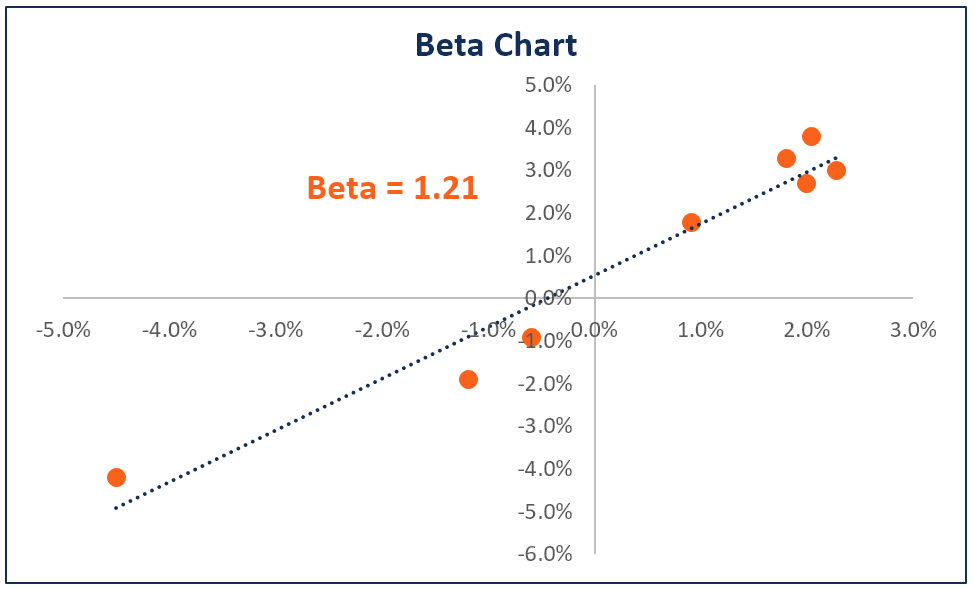

Here is a chart illustrating the data points from the β calculator (below):

Note: Beta measures only market-related risk, not total volatility. A stock can have high total volatility but a low beta if its price swings are largely unrelated to the market.

High β – A company with a β that’s greater than 1 is more volatile than the market. For example, a high-risk technology company with a β of 1.75 would have returned 175% of what the market returned in a given period (typically measured weekly).

Low β – A company with a β that’s lower than 1 is less volatile than the whole market. As an example, consider an electric utility company with a β of 0.45, which would have returned only 45% of what the market returned in a given period.

Negative β – A company with a negative β is negatively correlated to the returns of the market. For example, a gold company with a β of -0.2, which would have returned -2% when the market was up 10%.

Beta can be calculated using historical price data and regression analysis, or with Excel’s SLOPE function. Here is the general beta equation:

Where:

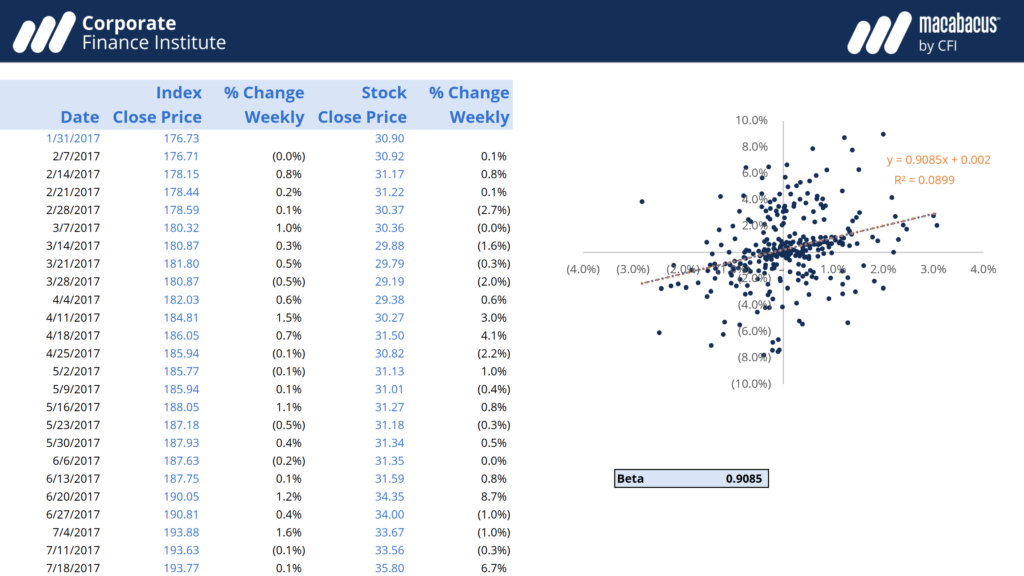

Below is an Excel β calculator that you can download and use to calculate β on your own in Excel using the SLOPE function.

Steps to Calculate Beta in Excel:

a. =SLOPE(stock returns, market returns)

Congrats! The output from the SLOPE function is the β.

Want to try it yourself? Download CFI’s free beta calculator template.

Levered beta, also known as equity beta or stock beta, is the volatility of returns for a stock, taking into account the impact of the company’s leverage from its capital structure. It compares the volatility (risk) of a levered company to the risk of the market.

Levered beta includes both business risk and the risk that comes from taking on debt. It is also commonly referred to as “equity beta” because it is the volatility of an equity based on its capital structure.

Asset beta, or unlevered beta, on the other hand, shows the risk of an unlevered company relative to the market. It includes business risk but does not include leverage risk.

![Formula for calculating levered or equity beta: Levered Beta = Unlevered Beta × [1 + (1 – Tax Rate) × (Debt / Equity)].](https://cdn.corporatefinanceinstitute.com/assets/levered-beta-1024x228.png)

Levered beta (equity beta) is a measurement that compares the volatility of returns of a company’s stock against that of the broader market. In other words, it is a measure of risk, and it includes the impact of a company’s capital structure and leverage. Equity beta allows investors to assess how sensitive a security might be to macro-market risks. For example, a company with a β of 1.5 denotes returns that are 150% as volatile as the market it is being compared to.

When you look up a company’s beta on Bloomberg, the default number you see is levered, and it reflects the debt of that company. Since each company’s capital structure is different, an analyst will often want to look at how “risky” the assets of a company are, regardless of the percentage of its debt or equity funding.

The higher a company’s debt or leverage, the more of its earnings that are committed to servicing the debt. As a company adds more debt, the uncertainty of the company’s future earnings also rises. It increases the risk associated with the company’s stock, but it is not a result of the market or industry risk. Therefore, by removing the financial leverage (debt impact), the unlevered beta can capture the risk of the company’s assets only.

There are two ways to estimate the levered beta of a stock. The first, and simplest, way is to use the company’s historical β or just select the company’s beta from Bloomberg. The second, and more popular, way is to make a new estimate for β using public company comparables. To use the comparables approach, the β of comparable companies is taken from Bloomberg and the unlevered beta for each company is calculated.

Levered beta includes both business risk and the risk that comes from taking on debt. However, since different firms have different capital structures, unlevered beta is calculated to remove additional risk from debt in order to view pure business risk. The average of the unlevered betas is then calculated and re-levered based on the capital structure of the company that is being valued.

Note: In most cases, the firm’s current capital structure is used when β is re-levered. However, if there is information that the firm’s capital structure might change in the future, then β would be re-levered using the firm’s target capital structure.

A security’s β should only be used when its high R-squared value is higher than the benchmark. The R-squared value measures the percentage of variation in the share price of a security that can be explained by movements in the benchmark index. For example, a gold ETF will show a low β and R-squared in relation to a benchmark equity index, as gold is negatively correlated with equities.

For example, the β of most technology companies tends to be higher than 1. Also, a company with a β of 1.30 is theoretically 30% more volatile than the market. Similarly, a company with a β of 0.79 is theoretically 21% less volatile than the market.

For a company with a negative β, it means that it moves in the opposite direction of the market. Theoretically, this is possible; however, it is extremely rare to find a stock with a negative β.

Understanding beta helps investors:

Beta is especially valuable for comparing a stock’s volatility to the broader market and estimating future performance under different economic scenarios. Whether you’re evaluating long-term investments, balancing portfolio risk, or analyzing the performance of sector-specific assets, beta provides insight into how a security might behave in various market conditions.

While beta is a powerful tool, it has some limitations:

Beta should be used in combination with other financial metrics and qualitative factors to provide a robust basis for investment analysis.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to beta (β) of an investment security. To continue learning and advancing your career, these additional resources will be helpful: