Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The highest level of value that an investment account or portfolio has reached

High-water mark is the highest level of value reached by an investment account or portfolio. It is often used as a threshold to determine whether a fund manager can gain a performance fee. Investors benefit from a high-water mark by avoiding paying performance-based bonuses for poor performance or for the same performance twice.

Investors typically pay a fixed management fee and a performance-based fee to a fund manager. The management fee is calculated as a fixed rate of the asset under management (AUM), as the performance fee is calculated as a percentage of the increase in AUM over a certain period. The fund management contracts include clauses that elaborate on such fees with the purpose of protecting the investors’ benefits.

A high-water mark is the minimum level that a fund manager needs to achieve to receive a performance bonus. The high-water mark clause protects investors by avoiding paying the performance fee for the same part of return when an investment fund or account recovers from the previous loss.

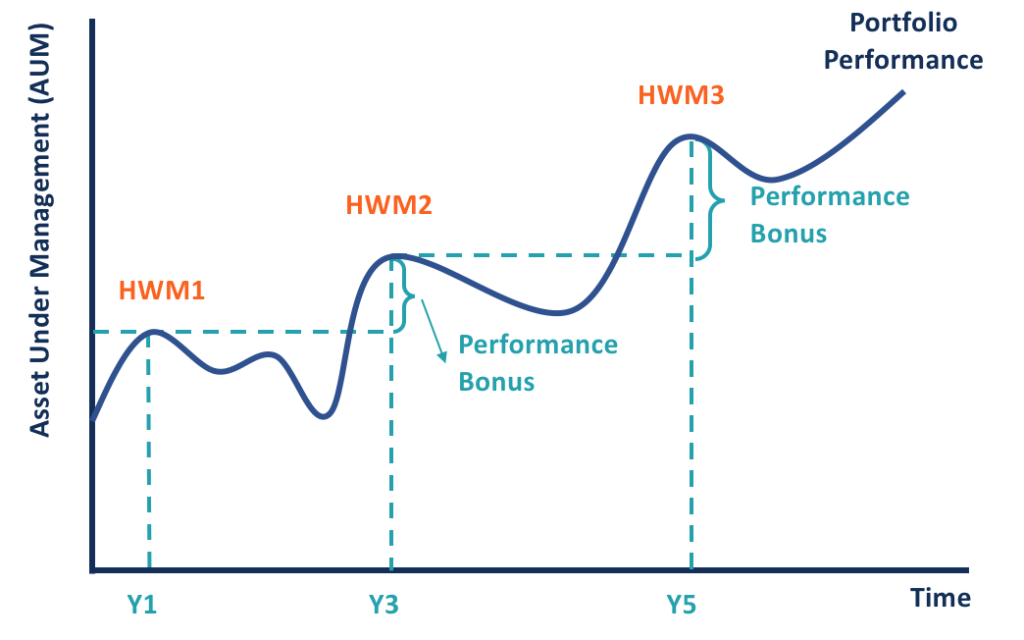

As the diagram above shows, an investment portfolio reached its first high-water mark in the first year, but the value dropped during Year 2. Since the AUM is below the high-water mark, investors are not charged performance fees in Year 2. In Year 3, the portfolio retrieved its growth potential and reached an AUM that is higher than in Year 1.

Thus, a new high-water market is reached, and the portfolio manager gains a performance bonus for the portion of AUM above the previous high-water mark.

Let’s assume an investment fund charges a 2% management fee and a 20% performance fee annually, which are typical industry rates. An investor invested $100,000 into the fund, which generated a return of 10% in Year 1, -3% in Year 2, and 20% in Year 3.

In the first scenario, there is no high-water mark clause for the performance fee. For Year 1, the management fee is $2,000 (2% * $100,000), and the performance fee is also $2,000 [($100,000 * 10% * 20%]. The AUM at the end of Year 1 is $106,000 ($110,000 – $4,000), which gives the investor a net return of 6%.

For Year 2, since the fund experienced a loss, there is no performance fee, but a management fee of $2,120 (2% * $106,000) is still charged, which gives an ending value of the fund worth $100,700 [$106,000 * (1-3%) – $2120].

For Year 3, the value of the fund reaches $120,840 [$100,700 * (1+20%)] before the management fee. After paying a management fee of $2,417 and a performance fee of $4,028 [($120,840 – $100,700) * 20%], the investor’s net return for this year is 13.6% [($120,840 – $100,700 – $2,417 – $4,028) / $100,700].

In the second scenario, let’s assume that the high-water mark limits the performance fee. The management fees are not impacted by this clause, and the performance fees for the first two years remain the same as the first scenario.

The fund reaches a high-water market of $110,000 ($10,000 * 10%) at the end of Year 1, which limits the third-year performance fee to the return above this level, which is $10,840 ($120,840 – $110,000). For Year 3 the performance fee is $2,168 ($10,840 * 20%), and the investor’s net return is 15.4% [($120,840 – $2,417 – $2,168 – $100,700) / $100,700].

Comparing the two scenarios, the high-water mark prevents the investor from paying for the $9,300 return again in Year 3, which was achieved and charged in Year 1 but partially lost in Year 2. The investor, who is protected by a high-water mark, will be able to pay a lower amount of performance fee and earn a higher net return.

Hurdle rate refers to a minimum level of return that a fund manager must reach to receive a performance bonus.

For example, if an investment fund grew from $1,000,000 to $1,040,000 with a 4% return in a year and a 20% incentive rate, investors need to pay a performance fee worth $8,000 ($40,000 * 20%). If a 5% hurdle rate is applied, investors do not need to pay a performance fee since the return does not exceed the hurdle rate.

Like the high-water mark, it also helps investors to pay performance fees for returns below expectation. The major difference is that under the high-water mark clause, the performance fee of the current term can be impacted by the previous performance of the fund. However, the current performance bonus is independent of the fund’s historical return under the hurdle rate.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on High-Water Mark. To keep advancing your career, the additional resources below will be useful: