Net Interest Rate Differential (NIRD)

Occurs when there is a difference in interest rates between two countries or regions

What is the Net Interest Rate Differential (NIRD)?

Net interest rate differential (NIRD) occurs when there is a difference in interest rates between two countries or regions. It normally takes place in the international foreign exchange markets when a person takes a long position in one currency and a short position in another currency. The difference between the interest received and the interest paid for the currency pair is the NIRD.

NIRD is specifically used in currency markets and is an important aspect of carry trade. Carry trade is a strategy that is employed to benefit from arbitrage, or simply put, the difference between the interest rates in two regions. If a person holds a long position on a currency pair, they will benefit if their position appreciates.

Similarly, a short position on a currency pair will gain when it depreciates. Traders normally use the interest rate parity to set an expectation of future exchange rates for a currency pair. A currency can either be trading at a premium, discount, or at par with the current market rates.

Summary

- Net interest rate differential (NIRD) occurs when there is a difference in interest rates between two countries or regions.

- NIRD is specifically used in currency markets and is an important aspect of carry trade.

- Foreign currencies are generally traded in the form of pairs, which is denoted as ABC/XYZ. The interest rate differential on the currency position is called the cost of carrying or rolling over the position.

Interest Rate Differential

Interest rate differential is a related concept that is used to generally define the variance in interest rates between two similar assets that include an interest rate attached to them. The assets can take the form of currencies, commodities, fixed-income assets, etc. NIRD is used only for currency markets.

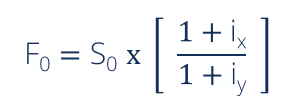

Interest Rate Parity

Interest rate parity states that the interest rate differential between two regions is equal to the difference between the spot exchange rate and the forward exchange rate. The formula for interest rate parity is given below:

Where:

- F0 = Forward Rate

- S0 = Spot Rate

- ix = Interest Rate in Country X

- iy = Interest Rate in Country Y

Spot exchange rates are current exchange rates, whereas future exchange rates are exchange rates that will prevail at some time in the future. The idea of arbitration emerges from the IRP, as people can exploit the interest rate differential (or the difference between the spot and future exchange rates) and generate a profit.

In a perfect world, IRP should not allow for any profits, as the equation above holds true. However, in the real world, traders find mispriced currencies and benefit from the trade.

Currency Carry Trade

Foreign currencies are generally traded in the form of pairs, which is denoted as ABC/XYZ. If a person buys the currency pair CAD/USD, they are actually buying the Canadian dollar and selling the US dollar. Interest is received on the currency you buy, and interest is paid on the currency you sell. Because the interest rate in the U.S. and Canada will most likely be different, the positions traded during the day in the foreign exchange market will achieve a net position of either interest payable or interest receivable.

Normally, all positions are closed at the end of the day, but if a person continues to hold the position, it is technically closed and then reopened the next day. The interest rate differential is charged to your account then. It is known as the cost of carrying or rolling over the position.

Positive Carry

Positive carry occurs when the net interest rate differential on the currency pair held is positive. For example, a person is long AUD/JPY, which means they buy the Australian dollar and sell the Japanese yen. The AUD interest rate is 5%, and the JPY interest rate is 3%. If the spot rate remains constant, the person will make a profit of 2% in the interest rate spread (which is also called positive carry).

Negative Carry

Negative carry occurs when the net interest rate differential on the currency pair held is negative. Taking the same example above, the person is long AUD/JPY, which means they buy the Australian dollar and sell the Japanese yen. The AUD interest rate is 1%, and the JPY interest rate is 4%. If the spot rate remains constant, the person will make a loss of 3% in the interest rate spread (which is also called negative carry).

It is important to note that positive and negative carry will be realized if interest rates do not change in the spot market.

Related Readings

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: