Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment to become a successful financial planner or wealth advisor.

A long-term portfolio strategy that involves choosing asset class allocations and re-balancing the allocations periodically

Strategic asset allocation refers to a long-term portfolio strategy that involves choosing asset class allocations and rebalancing the allocations periodically. Rebalancing occurs when the asset allocation weights materially deviate from the strategic asset allocation weights due to unrealized gains/losses in each asset class.

An SAA strategy is used to diversify a portfolio and generate the highest rate of return at a given level of risk. It is similar to a buy-and-hold strategy in that target asset weights are chosen and maintained over a long period of time. Target allocations in the SAA strategy depend on several factors, including investor risk tolerance, time horizon, and return objectives.

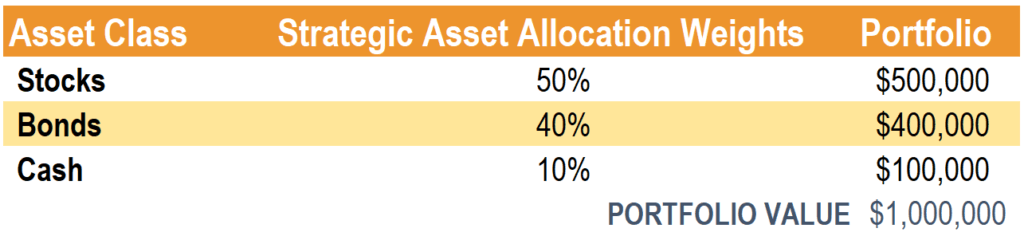

Jeff, in his investment policy statement, indicated that he wants a strategic asset allocation of 50% stocks / 40% bonds / 10% cash. Jeff’s portfolio is valued at $1 million, and he rebalances annually. At the beginning of the year, his portfolio looks as follows:

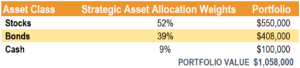

After one year, the stocks generated a return of 10%, while the bonds generated a return of 2%. Jeff’s unbalanced portfolio looks as follows:

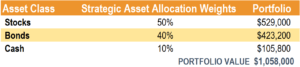

To follow an SAA strategy, Jeff would rebalance the portfolio above to 50% stocks / 40% bonds / 10% cash. He can do so by selling stocks and putting them in bonds and cash. His rebalanced portfolio would look as follows:

Therefore, at the end of the year, the SAA strategy would involve selling $21,000 worth of stocks and putting $15,200 in bonds and $5,800 in cash.

There are many factors that affect strategic asset allocation weights. Below, we will discuss the major factors:

Investors with a high risk tolerance are able to accept higher volatility. Therefore, they will likely put a greater asset class weight on stocks and a lower asset class weight on bonds and cash. Investors with a low risk tolerance would likely place a lower asset class weight on stocks and a higher asset class weight on bonds and cash.

Investors with a longer investment horizon would likely invest in riskier asset classes. The reason is that due to having a longer investment horizon, the investor is able to “weather the storm” and hold during poor market conditions without having to liquidate to meet their retirement or cash needs.

For example, a 20-year-old student would likely follow an SAA strategy consisting mainly of stocks. A senior who is retiring in two years and needs money to fund his retirement would likely adopt a strategic asset allocation consisting mainly of bonds.

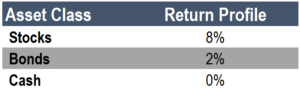

The returns desired from an investor significantly affect strategic asset allocation weights. For example, consider the annual return profile for stocks, bonds, and cash:

If an investor wanted their portfolio to generate an annual expected return of 6.5%, she would be forced to adopt the following weights: 75% stocks / 25% bonds / 0% cash.

Therefore, the return desired by an investor exerts a significant effect on the strategic asset allocation weight. A higher return requires a higher asset allocation to a specific asset class to achieve that desired return.

It is interesting to note that a strategic asset allocation follows a contrarian approach to investing. When an asset class performs well relative to another asset class, the SAA strategy would be to sell positions in that asset class and distribute it to the poorer performing asset classes – following a contrarian strategy. Consider the table below:

As indicated, stocks performed better than bonds, generating a return of 10% versus 5% of bonds. Since stocks performed better, the resulting unbalanced portfolio owns $5.50 in stocks and $5.25 in bonds, resulting in a strategic asset allocation of 51% in stocks and 49% in bonds. To balance the portfolio, the manager must sell the better performing asset class (stocks) and put it into bonds. Therefore, an SAA strategy follows a contrarian approach to investing.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: