Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A risk management strategy for options trading that aims to create a portfolio with a total vega of zero

Vega neutral is a risk management strategy for options trading that aims to create a portfolio with a total vega of zero. Vega represents the sensitivity of the price of an option to the implied volatility of the underlying asset. It is one of “the Greeks” of options trading.

Understanding the Greeks is necessary for options trading, as they describe different dimensions of risk. Vega measures how much the value of the contract of an option will change when the implied volatility of the underlying asset changed by 1%.

Vega measures the risk of change in implied volatility. When the volatility of an asset increases, the price of the corresponding option increases as well since it is more likely for the asset to hit the strike price.

Different from historical volatility, which indicates the past actual market changes, implied volatility is a forecast of the probability of price movements. It is one of the determinants of option prices. The more (less) the option price changes to a 1% change in implied volatility of the underlying asset, the greater (smaller) the vega of the option is.

Vega can either be positive or negative, depending on the position. Long positions in options come with positive vega, and short positions in options come with negative vega, regardless of the option being a call or put. When option price rises, traders in long positions benefit while the ones in short positions lose if the option is exercised.

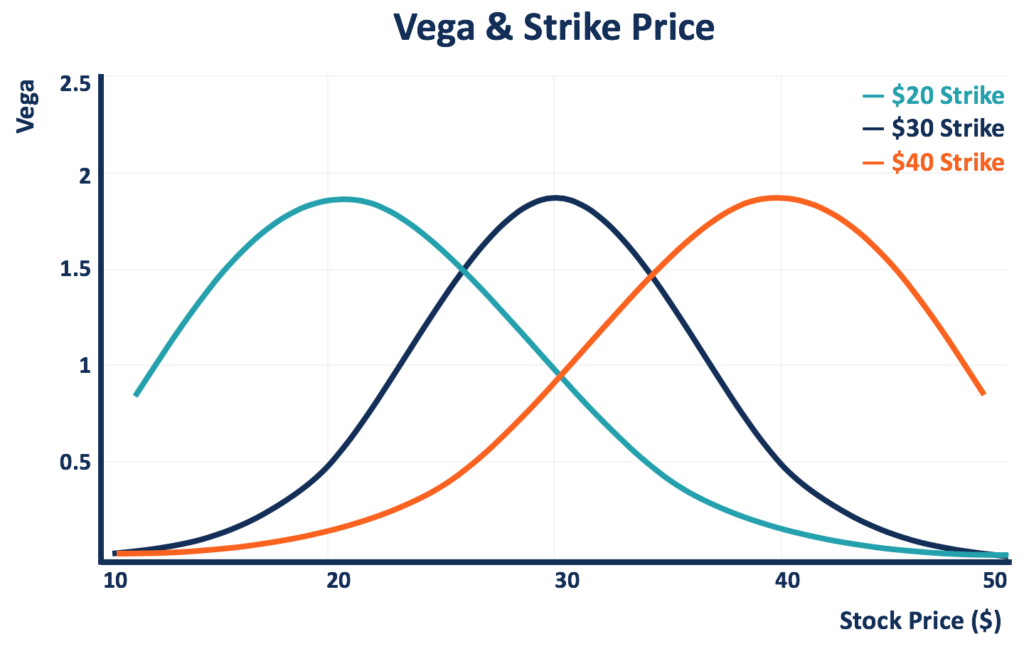

Vega is not linear, and it can be affected by several factors. One is the option strike price. The option price is most sensitive to the changing volatility of the underlying asset when the option is at the money (the strike price equals the spot price).

The diagram below shows the vegas of three options (at long positions) with different strike prices. When the current stock price moves closer to the strike price, the vega of the option increases, and it reaches the highest point when the option is at the money.

Another factor that changes vega is time to expiration. Options traders tend to offer higher premiums to the options expiring in the further future than the ones expiring immediately for the higher probability that the option can hit the strike before expiration. Therefore, as time passes and the option moves closer to the expiration date, its vega decreases.

The diagram below compares the vegas of options with the same strike price ($30) but different days to expiration. The shorter the time to expiration, the lower the vega is. The option with five days to expiration shows the lowest vega, compared to the ones with 15 days and 30 days to expiration.

As a change in the implied volatility of an asset causes risks to the price of the corresponding option, a vega-neutral strategy can be implemented to manage such risk. As mentioned above, vega can be either positive or negative, depending on the position that an options trader takes.

By managing the positions and lots of the options held, an options trader can reach a vega-neutral position where the total vega is zero. At such a position, the changes in the implied volatility no longer affect the total value of the position (for 1% change in implied volatility, the option price will change by 0%), and thus cause no loss.

In a vega-neutral portfolio, the total vega of all the positions in the portfolio sums up to zero. The positive vega from the long positions is perfectly offset by the negative vega from the short positions. An option trader can create such a portfolio by calculating the total vega from all the positions in the portfolio and manage the positions to reach a sum of zero.

Suppose the current portfolio shows a vega of VP, and a trader would like to short N units of options with a per-unit vega of VA. The portfolio will be vega-neutral if N = VP/VA.

For example, a portfolio consists of 200 lots of $50 strike calls with a vega of 5 per unit. The portfolio is exposed to the implied volatility risk with a total vega of 1,000. For a 1% decrease in implied volatility of the underlying asset, the portfolio value will drop by 20%.

The trader will then look for a short position for the same underlying asset at a different strike price to eliminate the risk. If there are $55 strike calls with a vega of 2 per unit, the trader should short 500 lots to reach vega neutrality (new portfolio vega = [200*5] – [5*200] = 0).

The above is a simple example of a vega-neutral portfolio that does not take into account complex conditions, such as different expiration dates or underlying assets. For options with different expiration dates, a time-weighted vega should be used; for options with different underlying assets, the correlation between the implied volatilities of the assets should be taken into consideration.

Vega neutrality can also be reached by implementing or combining other options trading strategies. For example, a commonly used one is to use a risk reversal strategy (a put with one strike against a call with a higher strike), when the put and call show the same vega.

A vega-neutral portfolio neither benefits nor loses when the implied volatility changes. Generally, there are two ways for a vega-neutral portfolio to make profits: from (1) the bid-ask spread of implied volatility or (2) the skew between the volatilities of the calls and puts.

In the bid-ask spread method, a trader can buy options at one implied volatility level and sell other options at the higher implied volatility level (thus, at a higher price). With the proper portion, the portfolio can remain vega-neutral.

In the skew between the volatilities method, if a trader expects that the implied volatility of puts will increase relative to that of calls, as the volatility curve does not shift as a whole, he can implement a vega-neutral risk reversal strategy to make profits.

Thank you for reading CFI’s guide on Vega Neutral. To keep learning and advancing your career, the following resources will be helpful: