Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A tax principle that asserts that taxes should be levied based on an individual’s ability to pay the tax

Ability-To-Pay Taxation is a tax principle that asserts that taxes should be levied based on an individual’s ability to pay the tax. In other words, individuals, corporations, partnerships, and other entities who earn a higher income will need to pay more taxes because they have the ability to do so. Many countries, such as the United States and Canada, use an ATP tax system when taxing citizens.

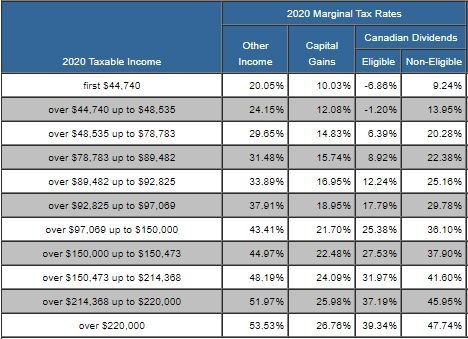

In Canada, our government uses the ability-to-pay principle to impose a progressive tax system. Within the progressive tax system, all taxpayers fall within a particular tax bracket based on their income. A tax bracket is a percentage rate imposed on a range of income. In 2020, the Canadian tax brackets are as follows:

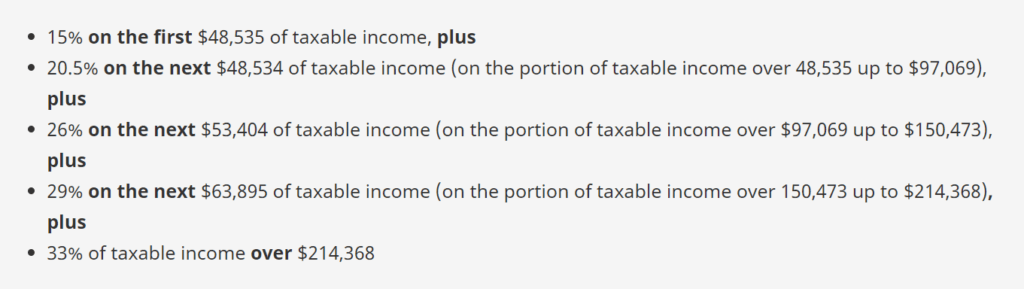

The federal tax rates for 2020 are as follows:

Taxpayers are expected to pay the prevailing tax rate in a specific bracket. In 2020, an individual will need to pay 15% on the first $48,535 of taxable income. Then, they will pay 20.5% on the next $48,534 of taxable income and then 26% on the next $53,404, and so on.

Generally speaking, an individual will not pay all the taxes they are expected to pay due to various tax credits and deductions that the government has made available.

In addition, every individual is provided a personal tax amount. The 2020 personal amount is $13,229 for taxpayers with a net income of $150,473 or less. For incomes above the threshold, the incremental increase from 2019 ($931) is reduced until it becomes $12,298 (the 2019 personal amount).

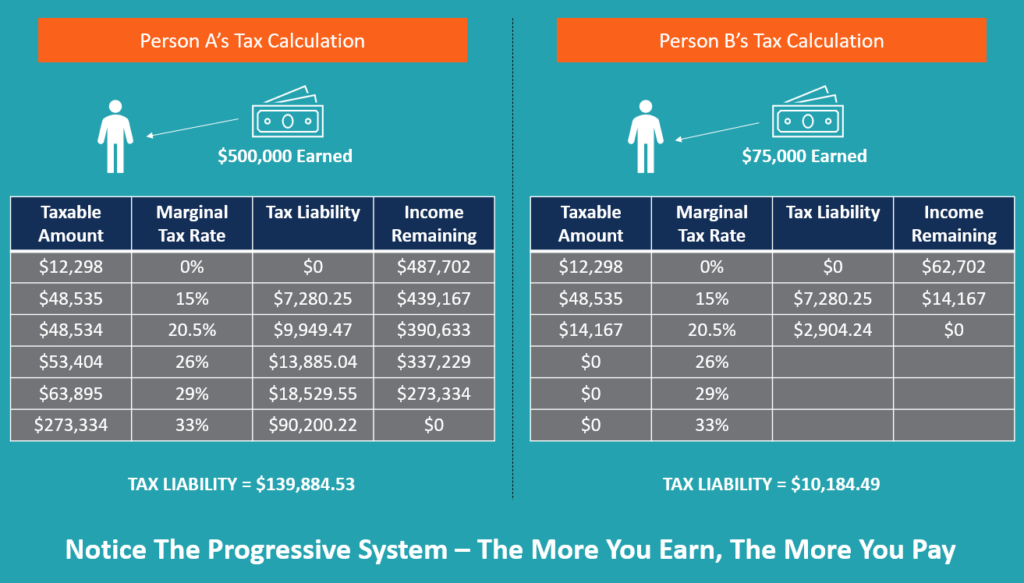

As an example, let us consider two individuals – Person A and Person B. In 2020, Person A is expected to make $500,000, and Person B is expected to make $75,000. According to ability-to-pay taxation, Person A would be expected to pay more tax because they have more income to be able to pay those taxes. The taxes would be calculated as follows:

Person A’s tax liability, based on his income, would be calculated as:

In total, Person A would incur a tax liability of $139,844.90.

Person B’s tax liability, based on his income, would be calculated as:

In total, Person B would incur a tax liability of $9,993.63.

Below is a diagram to summarize the calculations and explanations.

With an ability-to-pay taxation system, individuals with more resources are able to provide more funding for services needed by all. Societies rely on government services, either directly or indirectly, such as police, scientific research, schools, and more.

A different tax system may give rise to some “taxation deadweight loss.” For example, if a flat tax system was implemented, then the tax rate would need to be high enough to ensure enough government revenue for services, but low enough to accommodate low-income earners.

Taxation revenue is “left on the table” and that can lead to reductions in services. In addition, low-income earners most likely need a majority of their income, so an ability-to-pay taxation system allows them to keep a larger percentage of their income to help stimulate the economy.

Because an individual will pay more tax as their income increases, critics of the ability-to-pay taxation system argue that individuals will lose the incentive to earn more. In a sense, the critics argue that high incomes are penalized, even though the funds might have been accumulated through hard work and ingenuity.

When a government taxes its citizens, it makes decisions about how to best spend that money to benefit its citizens. Individuals argue that the services they receive don’t benefit them individually, so their taxes should be put towards services that benefit them (benefit-received taxation).

For example, the government would collect taxes from gasoline to service items, such as roads. All tax revenue that is collected from gasoline should be put towards roads, but it isn’t necessarily the case with ability-to-pay taxation.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: