Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A management tool used by accountants to evaluate accounts receivables and identify existing irregularities

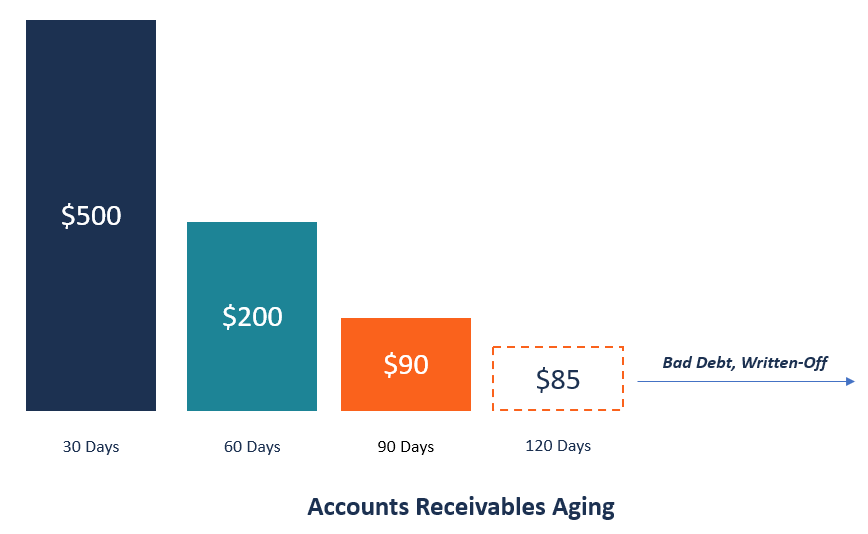

Accounts receivable aging is a cash management technique used by accountants to evaluate the accounts receivable of a company and identify existing irregularities. The aging method categorizes the receivables based on the length of time an invoice has been due, in order to determine which customers to send to collections agencies, who to target for follow-up invoices and which accounts might be completely uncollectible, thus necessitating a write-off.

Creating an aging report for the accounts receivables sorts the unpaid customers and credit memos by date ranges, such as due within 30 days, past due 31 to 60 days, and past due 61 to 90 days. The aging report itemizes each invoice by date and number. Management uses the information to help determine the financial health of the company and to see if the company is taking on more credit risk than it can handle.

Below are a few ways that company management can use an accounts receivable aging report:

One of the ways that management can use accounts receivable aging is to determine the effectiveness of the company’s collections function. If the aging report shows a lot of older receivables, it means that the company’s collection practices are weak.

Some customers tend to not pay their invoices when they are due, and they may wait until the second and third invoice reminders to settle their outstanding balance. If some customers are taking too long to settle pending invoices, the company should review the collection practices so that it follows up on outstanding debts immediately when they fall due.

The report also serves as a basis for management to adjust the credit period for customers and incentivize customers to clear their outstanding dues by giving cash discounts for early payments.

The accounts receivable aging report can also indicate which customers are becoming a credit risk to the company. Older accounts receivable expose the company to higher risk if the debtors are unable to pay their invoices.

If the report shows that some customers are slower payers than others, then the company may decide to review its billing policy or stop doing business with customers who are chronically late payers. Management may also compare its credit risk against industry standards, in order to determine if it is taking too much credit risk or if the risk is within the normal allowed limits in the specific industry.

Management may also use the aging report to estimate potential bad debts during the reporting period. Management evaluates the percentage of an invoice dollar amount that becomes bad debt per period and then applies the percentage to the current period’s aging reports.

For example, assume that Company XYZ allows for a 1% bad debts allowance for the 0 to 30 days period and a 3% bad debts allowance in the 31 to 60 days period. In the current period, the company reports $100,000 accounts receivable in the 0 to 30 days period and $50,000 accounts receivable in the 31 to 60 days period. This means that the allowance for bad debts is $2,500 based on the following calculation:

Allowance for Bad Debts = [($100,000 x1%) + ($50,000 x 3%)]

= $1,000 + $1,500

= $2,500

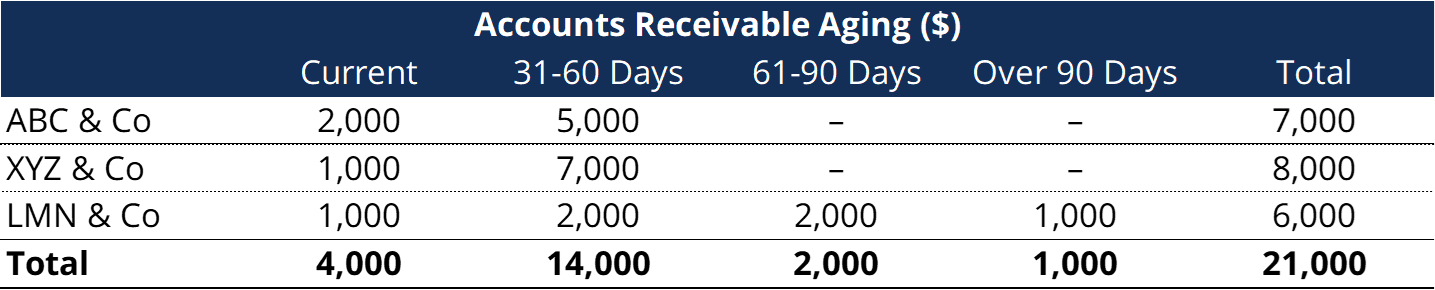

An aging report provides information about specific receivables based on the age of the invoices. It gives the management team a historical overview of the company’s receivables portfolio. It groups outstanding invoices based on the duration they’ve been due and unpaid.

In the example above, if we assume that the company’s credit policy is 60 days, then customers ABC & Co. and XYZ & Co. appear to be within the company’s credit period. However, LMN & Co. appears to delay its payments to the company.

An aging report is used to show current customer invoices and the number of days the invoices have been outstanding. If the company’s billing policy is to allow customers to pay for products and services in the future, the aging report allows the company to keep track of the customers’ invoices and when they are due.

The aging report also shows the total invoices due for each customer when grouped based on the age of the invoice. The company should generate an aging report once a month so management knows the invoices that are coming due. They can then notify customers of invoices that are past their due date.

Although an accounts receivable aging report helps the management team track the financial state of the company, it may provide information that is misleading, depending on the time when the aging report is generated.

For example, most companies bill their customers toward the end of the month, and the aging report is generated days later. This means that the report will show the previous month’s invoices as past the due date, when, in fact, some could have been paid shortly after the aging report was generated.

Also, generating the report before the month ends will show fewer receivables, whereas, in reality, there are more pending receivables. Management should match their credit terms to the periods of the aging reports to get an accurate presentation of the accounts receivable.