Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The five different opinions in an independent auditor's report

In the independent auditor’s report, an auditor can issue one of five different opinions:

A clean (unqualified) opinion refers to financial statements that are “presented fairly, in all material respects…”. Deviations from a clean opinion (where the financial statements are not presented fairly) result in a reservation (modification) in the independent auditor’s report.

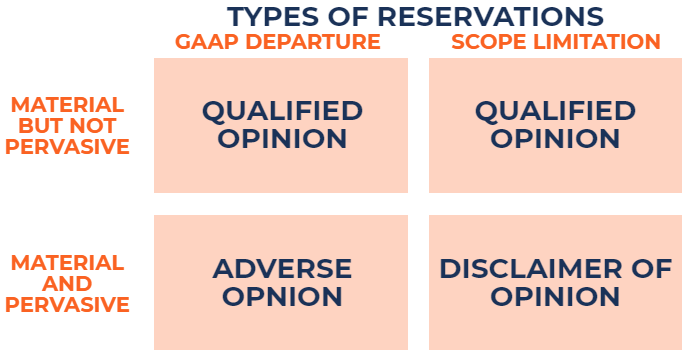

There are two types of reservations:

Situations in which the financial statements deviate from established accounting criteria. For example, a company that uses an incorrect accounting method faces a GAAP departure.

Situations where the auditor is unable to obtain sufficient appropriate audit evidence to base the audit on. This presents a scope limitation.

In addition, the type of opinion, based on the reservation made, depends on two factors:

Misstatements to the financial statements are considered material if the misstatements (individually or in aggregate), are expected to influence the decisions made by users who rely on the financial statements.

Misstatements to the financial statements are considered pervasive if the misstatements affect a substantial portion of the financial statements.

A qualified opinion can be issued due to a GAAP departure or a scope limitation. In both cases, the misstatements are material but not pervasive. In other words, there is a material impact on the financial statements, but the misstatements are not widespread (do not affect a large number of accounts).

The auditor noticed that the inventory of ABC Company faces a write-down due to obsolescence. However, the company refuses to write down the inventory. In such a scenario, a GAAP departure reservation is made. Since only the inventory and cost of goods sold accounts are wrong, a qualified opinion due to a GAAP departure would be issued.

The auditor wants to send out confirmation letters to customers for the accounts receivable balance as audit evidence. However, ABC Company does not want the auditor to do so. In such a scenario, a scope limitation reservation is made. Since the auditor has been unable to verify the accounts receivable, a qualified opinion due to a scope limitation would be issued.

An adverse opinion can only be issued due to a GAAP departure. In such a case, the misstatements are both material and pervasive. In other words, there is a material impact on the financial statements, and the misstatements affect a large number of accounts.

The auditor believes ABC Company faces a going concern issue and is unable to survive another year. The company disagrees and prepares its financial statements on a historical cost basis instead of on a liquidation basis. In such a scenario, a GAAP departure reservation is made. Since ABC Company prepared its financial statements on a historical cost basis, the majority of the company’s accounts are incorrect. An adverse opinion due to a GAAP departure would be issued.

A disclaimer of opinion can only be issued due to a scope limitation. In this case, the misstatements are material and pervasive. In other words, the auditor is unable to collect sufficient appropriate audit evidence to base its audit on and, as a result, a large number of accounts are not verifiable.

The auditor is looking to review the company’s minutes book, which contains important information regarding the board of directors’ meetings and the audit committee. ABC Company does not permit the auditor to review the minutes book. In such a scenario, a disclaimer of opinion reservation is made. Since the auditor is unable to access the minutes book, a majority of the company’s accounts cannot be verified. A disclaimer of opinion due to a scope limitation would be issued.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Auditor Opinions. To keep learning and advancing your career, the following CFI resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: