Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A complete evaluation of a company's overall standing in categories such as assets, liabilities, equity, expenses, revenue, and overall profitability

Financial performance is a complete evaluation of a company’s overall standing in categories such as assets, liabilities, equity, expenses, revenue, and overall profitability. It is measured through various business-related formulas that allow users to calculate exact details regarding a company’s potential effectiveness.

For internal users, financial performance is examined to determine their respective companies’ well-being and standing, among other benchmarks. For external users, financial performance is analyzed to dictate potential investment opportunities and to determine if a company is worth their while.

Before calculations can be made on certain financial indicators that establish overall performance, a financial statement analysis must occur.

Financial statement analysis is a process conducted on organizations by internal and external parties to gain a better understanding of how a company is performing. The process consists of analyzing four critical financial statements in a business.

The four statements that are extensively studied are a company’s balance sheet, income statement, cash flow statement, and annual report.

In financial statement analysis, an organization’s balance sheet is looked at to determine the operational efficiency of a business.

Firstly, asset analysis is conducted and is primarily focused on more important assets such as cash and cash equivalents, inventory, and PP&E, which help predict future growth.

Next, long-term and short-term liabilities are examined in order to determine if there are any future liquidity problems or debt-repayment that the organization may not be able to cover.

Lastly, a company’s owner’s equity section is inspected, allowing the user to determine the share capital distributed inside and outside of the organization.

In financial statement analysis, a business’s income statement is investigated to determine overall present and future profitability.

Examining a company’s previous and current fiscal years’ income statements enables the user to determine if there is a trend in revenue and expenses, which in turn shows the potential to increase future profitability.

A cash flow statement is critical in a financial statement analysis in order to identify where the money is generated and spent by the organization.

If one segment of the business is experiencing large outflows, in order to stay viable, the company must be generating inflows through financing or sales of assets.

The last statement, the annual report, provides qualitative information which is useful to further analyze a company’s overall operational and financing activities.

The annual report consists of all the statements listed above but adds additional insights and narratives on critical figures within the organization.

The additional insights and narratives within the annual report include an extensive narrative breakdown of the various business segments, benchmarks, and overall growth.

As a whole, financial performance analysis is critical whether it is conducted for internal or external use because it helps determine a business’s potential future growth, structure, effectiveness, and most importantly, performance.

Through a financial performance analysis, specific financial formulas and ratios are calculated, which, when compared to historical and industry metrics, provide insight into a company’s financial condition and performance.

When calculating financial performance, there are seven critical ratios that are extensively used in the business world to assist and evaluate a company’s overall performance.

The gross profit margin is a ratio that measures the remaining amount of revenue that is left after deducting the cost of sales.

The ratio is useful because it indicates as a percentage the portion of each sales dollar that can be applied to cover a company’s operating expenses.

The working capital measurement is used to determine an organization’s liquid net assets available to fund day-to-day operations.

Determining liquidity in a business is important because it indicates whether a company owns resources that can quickly be converted to cash if needed.

The current ratio is a liquidity ratio that helps a business determine if it owns enough current assets to cover or pay for its current liabilities.

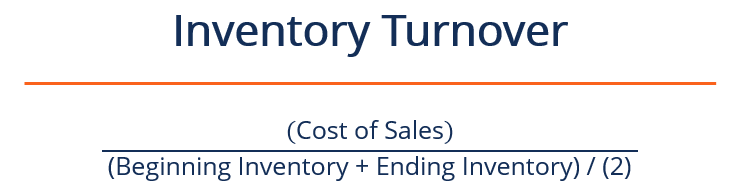

The inventory turnover ratio is an efficiency ratio that is used to measure the number of times a company sells its average inventory in a fiscal year.

The ratio is beneficial because it allows the organization to easily determine if their inventory is in demand, obsolete, or if they are carrying too much.

Leverage is an equity multiplier that is calculated by a business to illustrate how much debt is actually being used to buy assets.

The leverage multiplier remains at one if all assets are financed by equity, but it begins to increase as more and more debt is used to purchase assets.

Return on assets, as the name suggests, helps an organization determine how well its assets are being employed to become more profitable.

If the assets are not being used effectively, the company’s return on assets sum will be low.

Similar to return on assets, the return on equity is a profitability ratio that is used to analyze the equity effectiveness, which, in turn, earns profits for investors.

A higher return on equity suggests that investors are earning at a much more efficient rate, which is more profitable to the business as a whole.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s explanation of Financial Performance. To keep learning and advance your career, the following resources will be helpful: