Get In-Demand Finance Certifications

A consumption tax that is assessed on products at each stage of the production process

Value Added Tax (VAT), also known as Goods and Services Tax (GST) in Canada, is a consumption tax that is assessed on products at each stage of the production process – from labor and raw materials to the sale of the final product.

The VAT is assessed incrementally at each stage of the production process, where value is added. However, it is ultimately passed on to the final retail consumer. For example, if there is a 20% VAT on a product that costs $10, the consumer will end up paying a price of $12.

To calculate the amount of value added tax that must be paid at each stage, take the VAT amount at the latest stage of production and subtract the VAT that’s already been paid. It prevents double taxation and ensures that buyers at each stage get reimbursed for the VAT they’ve previously paid.

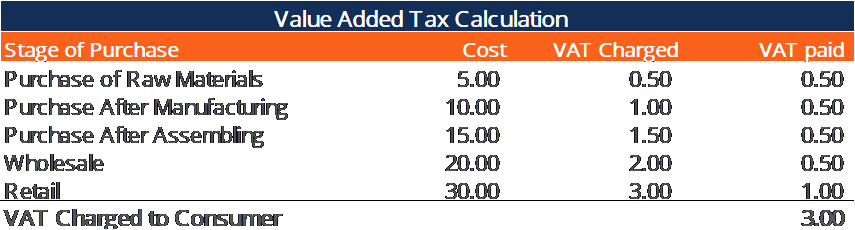

Consider the following example with a 10% VAT assessed at each stage.

A bike manufacturer purchases raw materials for $5.50, which includes a 10% VAT. After completing the manufacturing of the parts, they are purchased by the assembler for $11, which includes a VAT of $1. The manufacturer receives $11, of which he pays $0.50 to the government.

The full $1 VAT is not paid to the government, as the manufacturer will keep the portion of VAT that he already paid to the seller of the raw materials. Since the manufacturer paid $0.50 in VAT to the seller of the raw materials, he will pay only a VAT of $0.50 ($1 – $0.50) to the government (i.e., the incremental VAT).

Similarly, VAT paid at each stage can be calculated by subtracting the VAT that’s already been charged from the VAT at the latest stage of purchase/production.

As already mentioned, the entire VAT is ultimately passed to the final buyer(s), as consumers at the previous stages of purchase are reimbursed for the VAT they’ve paid. As seen below, the final retail consumer pays the entire sum of the VAT paid by the other buyers at prior stages. The final consumer’s VAT can also be calculated by multiplying the price (excl. VAT) by the VAT rate (i.e., $30 * 10% = $3).

Sales tax is very similar to VAT, with the key difference being that sales tax is assessed only once at the final stage of the purchase. Unlike VAT, which is assessed at each stage of purchase/production and paid by every successive buyer, sales tax is paid only once by the final consumer.

A key advantage of VAT over sales tax is that the former can allocate the tax amount to different stages at production based on the value added at that stage. Since sales tax is only paid once by the final buyer, one cannot measure the value added at each production stage. It makes it difficult to track and allocate the sales tax to specific stages of production.

Advocates of VAT argue that adopting a regressive tax system, such as VAT, gives people a stronger incentive to work and earn higher salaries, as they get to keep their income (i.e., they are not taxed more for earning more, which is true with progressive taxes, such as income taxes) and are only taxed when purchasing goods. VAT also makes it harder to evade taxes, as the tax is already embedded in the purchase of goods and services.

However, critics of VAT argue that, unlike the income tax rate, which varies at different levels of income, VAT is a fixed rate for everyone, and thus the poor end up paying a greater VAT rate than the rich, relative to their respective incomes. With VAT, goods and services become more expensive, and the entire tax is passed on to the consumers. It reduces the purchasing power of consumers and may make it difficult for low-income individuals and households to purchase necessities.

Another disadvantage of VAT is that businesses are faced with increased costs due to the administrative burden of calculating taxes at each stage of production. It can be especially challenging for global firms and multinational corporations with global supply chains spanning multiple tax regimes.

Despite the arguments against VAT, it offers some important benefits. The regressive tax can provide strong incentives to work, which can boost the overall gross domestic product (GDP) of an economy. It can also increase government revenues by reducing tax evasion and providing a more timely and efficient framework for collecting taxes.

Thank you for reading CFI’s guide to Value Added Tax (VAT). To keep advancing your career, the additional resources below will be useful: