Get Certified for

Capital Markets (CMSA®)

Learn financial analysis & planning, portfolio management, and risk assessment to become a successful financial planner or wealth advisor.

An annuity that is contractually designed to start paying income as soon as the policy has been started

An income annuity, also known as an immediate annuity, is an annuity that is contractually designed to start paying income as soon as the policy is started. Income annuities can be funded as soon as the policy begins. In addition, they may be annuitized immediately, giving the individual extra freedom and a sense of control.

An income annuity generally starts paying one month after the premium is paid and will continue to pay for the individual’s lifetime, albeit avoiding death or cancellation. As for fund remuneration, income units can be either fixed or variable investments.

Commonly, income annuities are purchased by individuals who are nearing or in retirement due to the fact that they provide relatively stable and risk-reduced payouts. In a retirement situation, an income annuity allows the individual to convert a portion of their retirement savings into a constant stream of lifetime payments.

In the most basic sense, an income annuity exists as a way for retirees to replace their monthly wage they would be earning if they chose to continue employment.

To understand the distinguishable traits of income annuities compared to other annuities, we will present the different types of annuities present on the financial market.

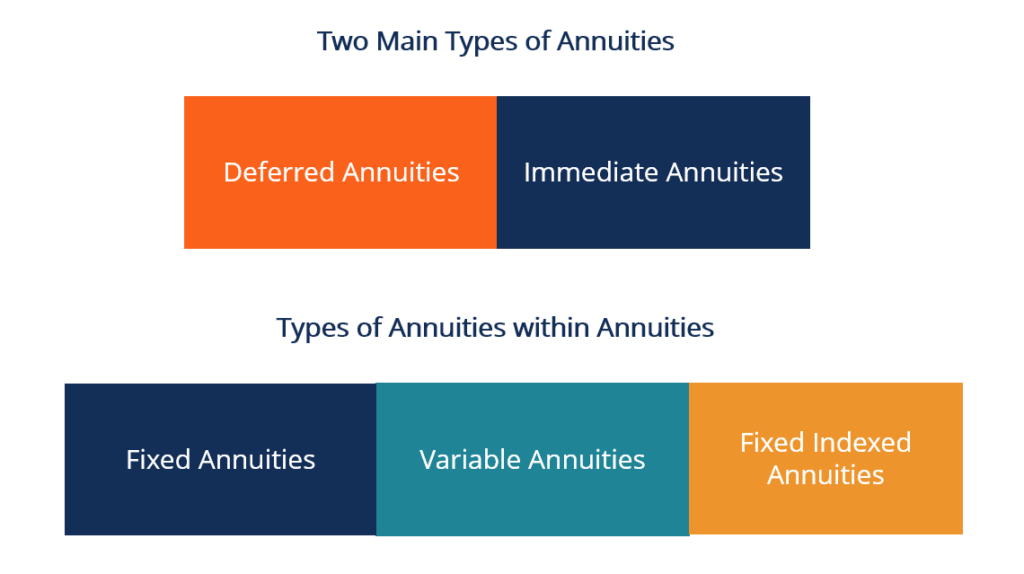

The two basic types of annuities are deferred annuities and immediate annuities.

Deferred Annuities: A type of annuity that begins to pay income at a future date that the owner determines.

Immediate Annuities: An annuity that is annuitized. It means that the annuity will become a stream of income immediately (i.e., an income annuity).

Within the two basic types of annuities, three more classifications exist:

Fixed Annuity: A type of annuity that provides a guaranteed rate of return over a fixed series of incremental payments.

Variable Annuity: An annuity where the performance of the financial market directly determines the amount of income that is received.

Fixed Indexed Annuity: A type of annuity that offers a guaranteed minimum rate of return where total returns directly relate to underlying indexes, such as the Vanguard S&P 500.

Individuals, or annuitants, can purchase income annuity vehicles from financial institutions or legal entities that sell financial instruments.

Unlike some financial instruments that provide a fixed rate over time, an income annuity guarantees lifetime incremental payments regardless of how the market performs. It means the longer the annuitant lives, the larger the overall income accumulates. The guaranteed payments are a key feature of an income annuity because longevity directly correlates to a higher return and additional payments.

If the annuitant were to pass away, most income annuities offer a cash refund death benefit in which the individual’s beneficiary will receive the remaining payouts over time. In some cases, age restrictions may be present, but it is directly based on the type of annuity that is purchased and the overall tax qualifications of the funds the annuitant uses.

As for other retirement lifestyle funding, annuitants can use a variety of sources such as a checking account, savings account, inheritances, investments, and other forms of retirement savings.

In order to determine the capital that should be invested, it may be beneficial to first speak to a professional and weigh the specific needs and situations that relate to you.

Income annuities are permanent contracts, so it is beneficial to know that the annuitant cannot withdraw more than their monthly income until the age of 59.5 years, but it is still not guaranteed.

When selecting a stream of income after retirement, it is beneficial to be aware of the direct benefits that each option provides. Listed below are the advantages of investing in an income annuity:

Listed below are the disadvantages of investing in an income annuity:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: