Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A percentage of the collateral’s value, reflecting the maximum loan amount that a lender is willing to extend to a borrower

An advance rate is a percentage of the collateral’s value, reflecting the maximum loan amount that a lender is willing to extend to a borrower. The advance rate is a lending risk assessment ratio used to determine the maximum loan value a borrower can secure, given the pledged collateral value.

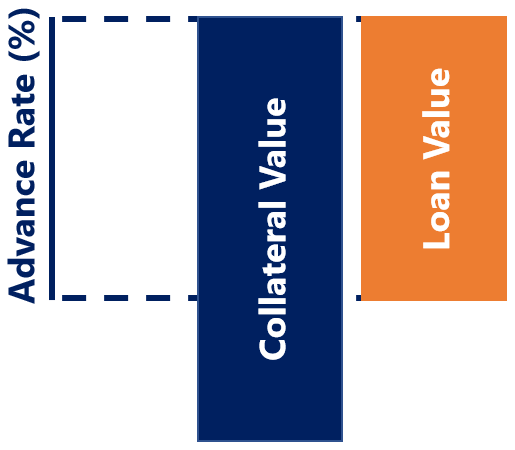

The advance rate formula is presented below:

An advance rate is used by a lender to indicate to a borrower the maximum loan value they are willing to extend to the borrower, given the collateral value.

A higher advance rate indicates higher risk tolerance by the lender, as the loan loss cushion is lower compared to a lower advance rate.

For example, a lender giving an advance rate of 90% on $500,000 in collateral value faces a greater risk of being unable to liquidate the collateral to reclaim loan losses in the event of a loan default versus a lender giving an advance rate of 40% on the same collateral value.

To compensate for greater risk, the required interest rate on a loan generally increases for the borrower as the advance rate increases.

The advance rate is interpreted similarly to the loan-to-value (LTV) ratio, another lending risk assessment ratio that compares a loan’s size to the pledged collateral to determine lending risk.

Question 1: Colin recently pledged collateral valued at $100 to secure a maximum loan amount of $70. What is the implied advance rate by the lender?

Answer: $70 / $100 x 100 = 70%. The implied advance rate by the lender is 70%.

Question 2: Tim lends at an advance rate of 120%. For collateral valued at $100, what would be Tim’s loss if the borrower entirely defaults on its loan?

Answer: With collateral valued at $100 and an advance rate of 120%, the loan value that Tim would extend to a borrower would be $120. If the borrower entirely defaults on its loan and assuming that the collateral is sold at its value of $100, Tim’s loss would be $20.

Question 3: John borrowed $100 at an advance rate of 50%. What is the implied pledged collateral value?

Answer: Given an advance rate of 50% and the maximum loan value of $100, utilizing the advance rate formula, the implied pledged collateral value is $200.

Question 4: Monica recently extended three loans, shown below. As a consultant, based solely on the information provided for each loan, what recommendation(s) can you give Monica?

Answer: A recommendation would be to charge higher interest rates on Loans B and C, as their advance rates are higher than Loan A but with the same interest rate (at 10%).

A higher advance rate indicates a higher risk of inability to liquidate collateral to fully recover loan losses in the event of loan default. To compensate for higher risk, it would be suitable to charge a higher interest rate.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ Program, designed to teach you all the knowledge and skills required to become a skilled credit analyst. The following CFI resources will be helpful in furthering your financial education and advancing your career: