Asset Protection

A set of techniques, strategies, and laws that aims to protect assets belonging to individuals and businesses against the claims of creditors

What is Asset Protection?

Asset protection refers to a set of techniques, strategies, and laws that aims to protect assets belonging to individuals and businesses against the claims of creditors who are attempting to legally seize the assets.

While creditors engage in developing and planning for the best debt collection strategies, debtors use asset protection planning for additional security. A debtor who owns significant personal assets may choose to use asset protection to shield his/her assets in case of a payment default.

How Does Asset Protection Work?

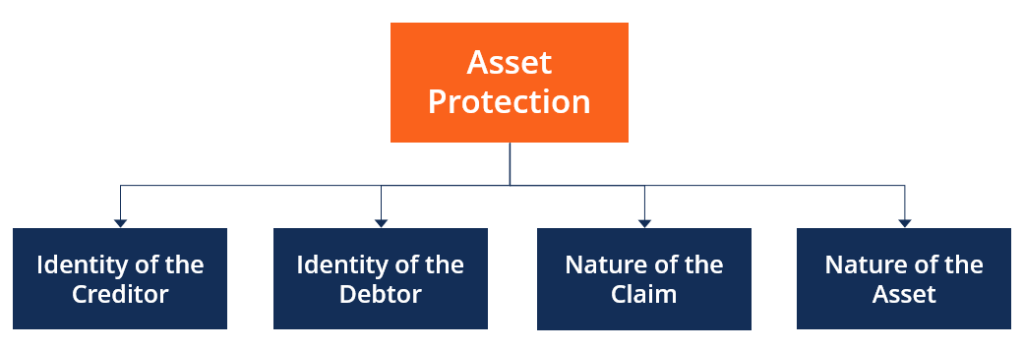

Asset protection planning is based on the analysis of various factors that determine the degree of protection required. The following diagram shows the most important factors:

Identity of the Debtor

If the debtor is an individual, it is important to consider any transmutation agreements (agreements that determine whether properties are equally shared by spouses or separate) between the individual and their spouse. It is also important to consider the likelihood of a lawsuit for each spouse – so that property rights for assets can be transferred to the ‘safer’ individual before lawsuits are filed.

If the debtor is an entity, then the individual who guaranteed the repayment is liable to asset seizure in the event of a lawsuit. For asset protection planning, it is important to take note of any clause that obliges an individual to personally repay an organization’s/entity’s debt and the likelihood of creditors seizing personal assets.

Identity of the Creditor

The identity and type of creditor are important for asset protection planning. If the creditor is a powerful organization, like the government, they are likely to possess more power over asset seizure compared to private lenders. Individuals who are liable to an aggressive creditor may require stronger asset protection strategies and vice versa.

Nature of the Claim

The specific types of claims and limitations included in lending agreements determine the strength and type of asset protection required. For example, dischargeable claims (claims that can be written off or “injuncted” by the court) can be used to protect personal assets in the event of bankruptcy and require a relatively lower degree of asset protection.

Nature of the Asset

Many types of assets are exempt from creditor claims. For example, the homestead exemption protects homeowners from forced home sales for debt repayment. Therefore, it is important to consider the types of assets included in the claims of creditors and the likelihood of each of the assets getting seized in the event of a lawsuit.

Asset Protection Strategies

1. Using Corporations, Limited Partnerships (LPs), and Limited Liability Companies (LLCs)

Owners of corporations, limited partnerships, and limited liability companies (LLCs) are typically protected by the government through limited liability laws, whereby individual owners are not held accountable for the entity or organization’s debt. Using the above types of businesses to borrow credit protects the individual’s personal assets from seizure in the case of a lawsuit.

However, it is often deemed unethical to use the abovementioned methods to protect personal assets. There are many laws regarding fraudulent transfer that hold an individual accountable for deliberately transferring assets to delay or default on debt repayments. Similarly, many laws in the U.S. allow creditors to permeate corporations and LLCs to hold individuals accountable.

2. Using Asset Protection Trusts (APTs)

An asset protection trust (APT) is a type of trust bank that holds assets based on the discretion of the settlor (i.e., the individual investing in the trust) to protect the assets from creditors. It is often used as the strongest method of asset protection.

Assets that are part of APTs are not legally entitled to the owners, who take the form of “beneficiaries that hold equitable interest” in the assets. Thus, the assets are protected from creditors without breaching tax evasion laws.

However, the use of APT comes with many drawbacks. One of them being that it cannot be revoked or overturned after the creation of the trust since it involves the use of legal ownership power, which must be given up for asset protection. Similarly, “spendthrift clauses” in APT agreements block the sale or use of any asset for credit repayment unless it is under certain circumstances.

3. Transferring Property Rights

An individual may transfer the legal right to an asset to their spouse, relative, or a trusted friend to protect it from creditors’ claims. This allows the debtor to possess their asset without the risk of losing it to creditors. However, it also presents a huge risk in case of conflict with family members or friends (e.g., a divorce) since they will legally own the assets.

Through laws, most legal jurisdictions regulate the fraudulent transfer of assets, and the debtor may be held accountable for deliberately delaying/defaulting on a payment, leading to fines and/or time in jail.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: