Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A short-term financing option that allows a customer to buy a good or service and pay it off at a later date, without the use of a traditional credit-provider

BNPL (Buy Now, Pay Later) is unsecured consumer credit and an increasingly popular fintech-enabled payment option, most commonly offered on e-commerce platforms. The history of BNPL traces back to the installment plan – a way to pay for large purchases over time by spreading it over a number of smaller payments.

BNPL is a financing alternative for consumers (meaning individuals), but it has also evolved into the business credit space.

BNPL is a form of POS (point of sale) financing, meaning that credit is originated directly at the time and point of sale, as opposed to a customer being required to secure credit from a lender or a credit card provider ahead of their shopping experience.

Notable names in the BNPL space include Affirm, Klarna, and Afterpay.

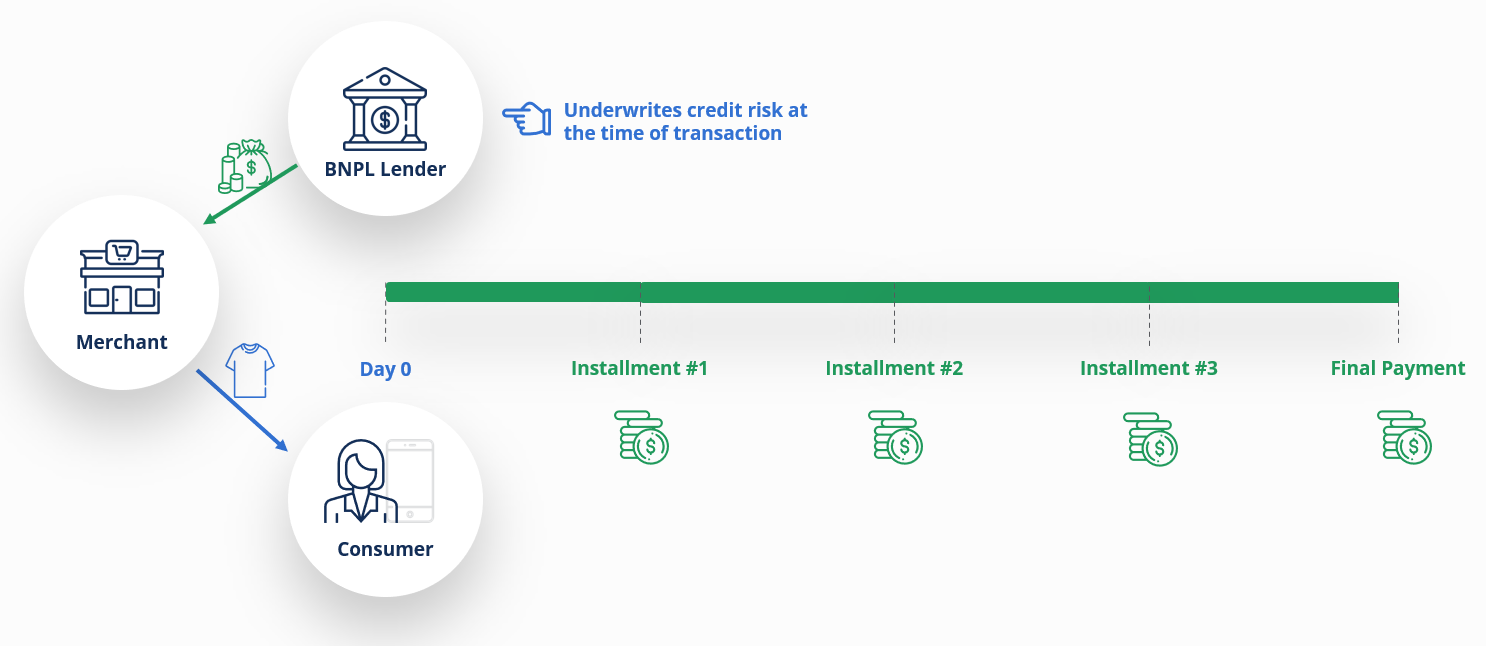

There are three parties involved in a BNPL transaction – a consumer, a merchant, and a financial services provider (usually a fintech).

When checking out, a consumer would traditionally use a credit card (if they had one) or a debit card. With BNPL, they’re able to actually pay a very small amount (and sometimes nothing) up front and instead split the payments for the total purchase through installments over weeks or months.

BNPL is an interesting and attractive way to access credit for consumers that may not have other forms of payment; perhaps a lack of credit history has precluded them from getting a credit card, for example.

Consumers get quick credit decisions from the BNPL provider so they can focus on the shopping experience. The upfront consumer experience is often more efficient than requesting traditional credit from a lender, due to low consumer regulations for BNPL transactions. For example, consumers do not have to disclose much information to the BNPL provider.

BNPL loans tend to be interest-free for the consumer, though, so there’s a financial incentive to leverage this technology even for buyers who have access to alternative credit and payment sources. There’s a psychological risk here when consumers aren’t paying a lot “out of pocket” up front; they are more likely to make a purchase and may also spend more than they would otherwise.

Consider a buyer who intended to purchase $100 worth of some product online but was given the option to instead pay $25 every two weeks for eight weeks. That consumer may instead purchase more goods.

Merchants are constantly looking to increase customers’ average ticket prices. Furthermore, e-Commerce merchants in particular often face “abandoned” shopping carts, meaning the consumer does not go through with a purchase after all. When merchants offer BNPL, customers seem to complete a purchase more often and for larger dollar amounts, so there’s a business case for merchants to consider this option.

Extending credit at the point of sale requires the merchant to underwrite the credit risk themselves along with the administrative costs. This is considerably less attractive than offering their consumer this option by paying a fee to a BNPL partner.

Further, merchants are already giving up margin to Payment Processors for credit card transactions, so substituting fees from one financial services provider to another (in exchange for a potentially larger average ticket price) is a compelling value proposition. Put another way, merchants subsidize their consumers under this financing option in exchange for making more sales and growing higher-value transactions.

In a BNPL transaction, the financial services provider (lender) pays the merchant at the time the transaction occurs, taking on the responsibility of granting credit and collecting payments from the consumer over the course of the BNPL term.

BNPL providers take on the risk of non-repayment from the consumer, both as a payment processor and as a lender. To be compensated for the risks, they pay merchants a discounted amount of the full purchase price. The lender then collects installment payments from the consumer that equal the full amount of the customer’s purchase price.

The difference between what they pay and what they collect over the course of the BNPL term is the lender’s primary source of revenue. Publicly disclosed fees range from 2.5% to 12.5% of the gross merchandise volume[1].

BNPL providers are high-tech companies with high costs to grow their platform and infrastructure. They must offer consumers and merchants compelling reasons to select their services over their competitors. Most cite “proprietary” models to underwrite unsecured credit risk for consumers and do not disclose the approval criteria.

As the industry is relatively new and underwriting is largely automated with some manual review for fraud, it is unknown if their credit quality is sufficiently compensated by the fees and interest they charge to merchants and consumers.

Profitability for BNPL providers remains elusive. In particular, the providers are very quick to charge off non-performing loans when compared to other forms of unsecured credit (account overdrafts, credit cards, etc.).

The source of the funds the providers use to lend to consumers varies (e.g., debt via traditional lenders, merchant deposits and payables, securitized debt via capital markets). The net interest margin of BNPL providers, or the difference between interest paid and interest received, has yet to be tested in a rising interest rate environment.

To generate repeat clients and greater engagement, BNPL providers have expanded to revolving-type credit and other offerings (virtual credit and debits cards, bank accounts, etc.), taking on characteristics of traditional financial institutions. The goal shifts to gaining a greater share of the consumer’s wallet and spending in order to acquire a low cost of funds (consumer deposits) and to also generate recurring loan receivables and interest.

Because BNPL financing is an attractive method of payment for consumers, merchants that implement a BNPL option at checkout are likely to see higher conversion rates, higher average transaction amounts, and thus an increase in overall sales.

BNPL lenders that offer interest-free loans collect the majority of their revenue from the merchants by way of discounting the transaction amount. Some BNPL offer longer-term (months to years) but lower interest loans compared to traditional financing, as the loans are partially subsidized by merchants that are keen on closing the sale, especially on bigger ticket items.

These lenders often collect a low percentage (or sometimes, a flat) fee on each transaction. The other main stream of revenue is late fees if/when the consumer gets behind on their payments.

BNPL firms underwrite and manage credit risk by accessing data in real-time through a retailer’s order management system, where they can assess and manage billings to help avoid potential disputes. Their credit underwriting tends to be heavily reliant upon a consumer’s credit score.

BNPL is subject to network effects. Wider and more mainstream adoption will depend upon the number of consumers that want it, which in turn will require more vendors to offer it (and vice versa).

Similar to how search engine companies pay traffic acquisition costs in order to generate greater search volume and advertising revenue, BNPL providers see merchants as a low-cost channel to acquire a greater number of consumers.

The consumers can then be monetized beyond the original purchase transaction. In fact, some BNPL loans do not require merchant integration at all. Consumers simply elect to use a virtual credit or debit card solution offered directly through the BNPL provider.

BNPL hit the news in a negative light in early July 2022, thanks to Klarna, a noteworthy Swedish BNPL firm.

Klarna raised USD$800 million at a $6.7 billion valuation. This represented an approximately 85% drop in valuation from its high of over $45 billion just a short year earlier.

At least part of the drop was attributable to a rising rate environment and a growing risk-off sentiment globally, both of which put downward pressure on valuations in the technology sector.

But critics of the BNPL model have suggested that this is the market coming to grips with slower-than-anticipated adoption and general business model risks/flaws. Many of these same voices are suggesting that the Klarna situation is predictive of more pain in the sector.

Many critics have voiced concerns about the potential negative impacts of BNPL as it becomes increasingly common among shoppers. Because of the nature of the payment option, consumers may feel a false sense of financial security or value.

As influencer marketing tactics become increasingly prevalent on social media platforms, some fear BNPL options could lead to a surge in impulse shopping and actually even foster a consumer culture that overspends.

Given the relatively unregulated nature of BNPL, there is still much skepticism about its viability as a mainstream financing and/or payment technology. Nevertheless, it’s estimated that in 2021, major US banks lost between USD$8bn and $10bn in revenue to fintechs in the POS financing space[2].

As lenders typically rely on credit reporting agencies, and not all BNPL providers report regularly, there is the potential of an excess amount of credit available to consumers who may not be capable of making all the payments.

That is to say, when lenders underwrite credit, they may mistake the consumer’s total credit capacity if they do not or cannot consider BNPL loans already granted within their approval process. For example, when multiple BNPL providers grant credit to the same consumer, they may be unaware of each other when providing a credit approval.

With household debt at or near record levels in many parts of the world, and hawkish central banks raising rates at a pace not seen in decades, there are critics in the finance community who worry BNPL is throwing gasoline onto a debt-fuelled consumer spending fire that’s already out of control.

As a consumer, it’s important to understand the terms under which a given BNPL loan system operates and to note the potential impact of a BNPL transaction on one’s ability to access credit in the future. Additionally, the ease of access to BNPL as a method of payment means that buyers are less protected against potential scams than they would be by a traditional credit card transaction.

The creditworthiness of a potential customer is usually evaluated in real-time before BNPL financing is extended. BNPL loans don’t require that borrowers go through a drawn-out, more traditional credit approval process, which is part of what makes them so attractive to consumers.

But even when payments are made on time, because many BNPL fintech platforms don’t report to credit reporting agencies the same way more traditional lenders and payment processors do, it doesn’t really help consumers build a credit history.

Similar to using credit cards and other credit facilities, prudent debt management is critical for BNPL consumers. In particular, when using multiple BNPL purchases or providers, consumers must track total debt obligations in order to balance them against cash available for living expenses.

This relative mixed bag of pros and cons has been a drag on more widespread consumer adoption and has created much regulatory uncertainty.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to BNPL. To keep advancing your career, the additional CFI resources below will be useful:

See all Commercial Lending resources