Deferment Period

A length of time where the borrower is not obligated to pay interest and loan payments

What is a Deferment Period?

A deferment period is a length of time where the borrower does not need to pay interest or repay the remaining amount on a loan. Before the loan is issued, a contractual agreement is decided between the lender and the borrower regarding the length of the deferment period.

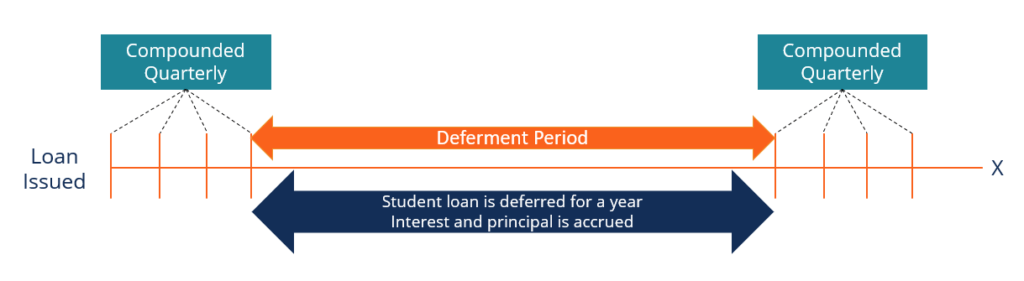

The diagram above depicts a student loan that was deferred after one year of the loan being issued. In such a case, the deferment period was only one year.

Summary

- A deferment period is a length of time where the borrower is not obligated to pay interest and loan payments.

- Grace period differs from deferment in length and when it is applied.

- A deferment period is beneficial because it grants the borrower a breathing room, but it also leaves the borrower in more debt due to accrued payments.

Deferment Period vs. Grace Period

When it comes to loans, borrowers can run into confusion regarding the difference between a deferment period and a grace period. Here are the main differences:

Deferment Period

- As mentioned, a deferment period is a period where the borrower is not obligated to pay the principal or interest on the loan. During the period, interest is accrued on the loan and added to the principal after the deferment period.

- In addition, a contractual agreement regarding the length of the deferment period must be signed between the lender and the borrower. Usually, the borrower must show economic hardship to be granted a deferment period.

- In the case of some loans, a deferment period is automatically applied.

Grace Period

- A grace period is a length of time after the loan due date where the borrower does not need to pay any money towards the loan.

- A grace period is automatically granted, and the borrower will not receive any sort of financial penalty for not paying during the grace period. In most cases, compound interest will be added.

- Conversely, grace periods are generally much shorter in length than a deferment period based on the fact that borrowers are not charged penalties such as late fees.

Types of Deferment Periods

In the financial sector, there is a wide array of loans that can be granted to borrowers. Each type of loan comes with a different application regarding deferment periods. The different types of loans and their varying deferment periods are discussed below:

1. Student loans

Granted during school or after graduation, a deferment period on student loans allow students to gain financial resources. Also, the accrual of interest varies.

In some circumstances, interest does not accrue on student loans and vice versa. Mostly, interest accrues on unsubsidized deferred student loans and does not accrue on subsidized deferred student loans.

2. Insurance

A deferment period exists for employees who are unable to work. During the deferment period, the employee is unable to accumulate benefits, and claim payments are deferred.

3. Mortgages

In most cases, the first payment of a newly established mortgage will be deferred. To put it into simpler terms, a borrower who was granted a loan in June may not be obligated to start making mortgage payments until August.

4. Callable securities

The deferment period is the length of time in which an issuing entity cannot redeem a bond. In addition, the issuer is unable to call the security back during the agreed deferment period.

5. Options

An American vanilla option is a form of option that can be exercised any time before expiration. The payments are deferred until the principal option expires.

Advantages of a Deferment Period

As a borrower, one must be educated on the positives and negatives that deferment periods offer. Listed below are the advantages of a deferment period:

- It postpones the repayment of the loan.

- Additional time is given to improve financial conditions.

- Deferment period reduces the pressure of constant repayment.

- Deferment periods are much longer than grace periods.

- In some cases, it avoids incurring late fees.

- In some cases, it avoids collateral repossession.

Disadvantages of a Deferment Period

- During the deferment period, interest is being accrued.

- The overall loan balance is increased due to accrued interest.

- In some cases, borrowers are subject to additional fees.

- The borrower must prove they are experiencing financial hardship.

- The lender takes a risk by granting a deferment period because the borrower may not be financially stable enough to pay the loan after the deferment period is over.

A deferment period is a feasible option for someone facing economic hardship. It gives the borrower breathing room and allows them to get back on their feet by deferring loan and interest payments. However, the overall loan balance is increased due to the deferral.

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: