Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A static interest rate that is charged on a liability

A fixed interest rate refers to a static interest rate that is charged on a liability – such as a mortgage, credit card, loan, or corporate bond. A fixed interest rate may apply to a liability’s entire term or over a partial period of its term.

An interest rate is a rate charged for borrowed money and is typically expressed as a per annum percentage. A fixed interest rate is popular with borrowers who want exact certainty on their repayment amounts.

For example, there is exact certainty in determining the monthly repayments of a $50,000 mortgage with a term of 10 years at a fixed interest rate of 5% versus determining the monthly repayments of a $50,000 mortgage with a term of 10 years at a variable interest rate of prime + 2%, with the lower certainty in the variable interest rate stemming from the prime rate.

In a rising overnight rate environment, consumers with mortgages tend to prefer locking into a fixed interest rate over opting for a variable interest rate. Variable interest rates are typically tied to the overnight rate, and as the overnight rate increases, the variable interest rate increases, resulting in higher repayment amounts.

Key advantages:

Key disadvantages:

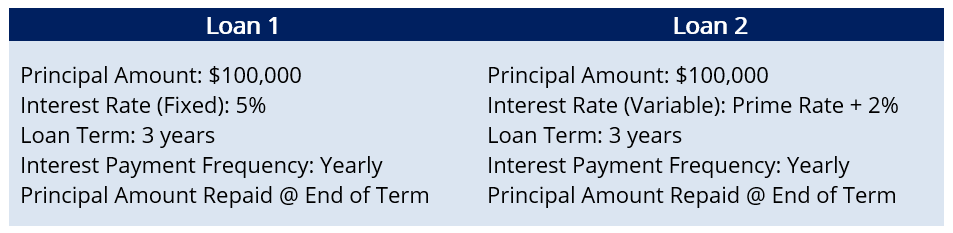

Question 1: Tim is presented with two loan options:

Tim believes that the prime rate will be the following over the next three years:

Given the information provided, which loan option would result in a lower total payment?

Answer: Loan 1 would result in a lower total payment. The calculation for each loan is provided below.

Loan 1: The yearly interest payments are calculated as $100,000 x 5% = $5,000. The yearly payment amount is unchanged each year, as Loan 1 features a fixed interest rate. As such, the total payment is calculated as $5,000 (interest in Year 1) + $5,000 (interest in Year 2) + $105,000 (interest + principal in Year 3) = $115,000.

Loan 2: As Loan 2 features a variable interest rate with a changing prime rate each year, the yearly interest payments differ each year. The total payment is calculated as $4,000 ($100,000 x [2% + 2%] interest in year 1) + $6,000 ($100,000 x [4% + 2%] interest in year 2) + $108,000 ($100,000 x [4% + 2%] interest + principal in year 3) = $118,000.

Question 2: As a financial advisor to Tim, provide a comment regarding the certainty of interest payments under Loan 1 versus Loan 2.

Answer: Loan 1 features a fixed interest rate and, as a result, the yearly interest payments on the loan are certain. On the other hand, Loan 2 features a variable interest rate, which causes uncertainty in the yearly interest payment amounts.

The Government of Canada’s mortgage calculator can help potential borrowers determine mortgage payment amounts, given a fixed interest rate.

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst. In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: