Opinion Letter

A letter issued by a legal counsel that facilitates a lender’s due diligence process on a transaction

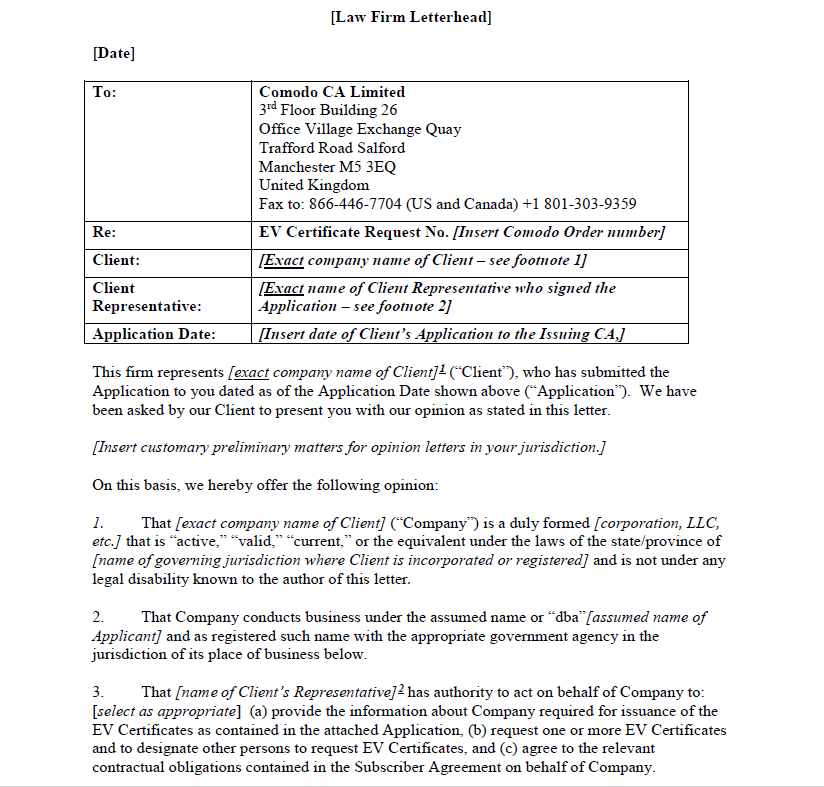

What is an Opinion Letter?

An opinion letter, also called a legal opinion, is a letter issued by a legal counsel that facilitates a lender’s due diligence process in a transaction. The opinion letter is used in credit analysis to help determine whether to lend to a borrower or not.

Lenders often require an opinion letter to act as proof of legal counsel’s advice and conclusions regarding the loan documents relevant to the transaction.

Summary

- Opinion letters signify the completion of a vital part of the due diligence process.

- Lenders and borrowers may both suffer undue consequences if due diligence is not properly completed, thus further showing the importance of the opinion letter.

- Documentation is vital to ensure that loan security is handled properly.

Components of an Opinion Letter

The four key components of a standard opinion letter are:

- List of documents reviewed

- Factual conclusions

- Legal enforceability opinion

- Qualifications

In the opinion letter, a legal counsel will first mention the documents reviewed (the security and loan documents). They will then specify factual conclusions in the opinion letter concerning the loan documents and whether they have been validly authorized, executed, and delivered.

The opinion letter will then typically conclude that the loan documents are enforceable in accordance with the terms of the loan. This is very important, as the legal counsel must ensure that the documents are prepared properly so that the transaction can carry forward. Finally, the legal counsel will also list their qualifications in the opinion letter.

What is the Role of the Legal Counsel?

The legal counsel serves an important role in protecting the interests of both the lender and the borrower. They review all security guarantee documents and determine the enforceability of all legal agreements from the lender’s standpoint.

During the review process, the legal counsel will:

- Ensure the completeness of the prepared documentation

- Determine if the borrower has the legal power to enter into any loan agreement

- Ensure the accuracy of the agreements related to loan security

- Ensure any security has been properly registered and confirm the security position of the lender

From a borrower’s perspective, the legal counsel will advise the borrower on the legal liability that he will be subject to under any loan agreement signed with the lender. They will also provide advice on the enforceability of the agreements, including what rights the lender has in the event of their inability to repay the loan.

If a loan has a personal or corporate guarantor, the legal counsel will typically also advise the guarantor on his rights and duties. The guarantor will be liable to remedy the failure if the borrower fails to make a payment on time. In case the guarantor fails to cover the failure of the borrower, the lender can sue the guarantor.

Importantly, the lender can use its rights against the guarantor even if the borrower has not been pursued. The liability of the guarantor will be either limited or unlimited, as specified in the guarantee agreement.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: