Rent to Own

Rent now, buy later

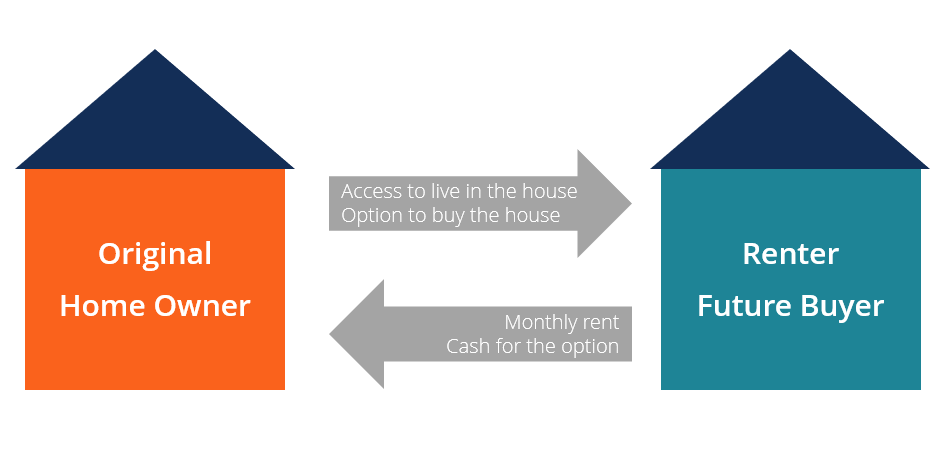

What is Rent to Own?

Rent to Own is a way for someone to immediately move in and be living in a house by paying rent, and later having the option (but not the obligation) to purchase the home from the owner. There are several reasons why renting to own can be attractive for both parties in the transaction.

How Rent to Own Works

Let’s break down the steps of how the rent to own structure works. In the following sections, we will explore what each party’s motivation to enter a rent to own agreement may be, and how the agreement is structured.

#1 Potential buyer can’t get a mortgage

A potential buyer decides they are looking for a place to live and would like to own that place, if possible. They search around for options and find a house they would like to live in. Upon doing further research, they realize the bank will not provide the mortgage they need to purchase the home, but they are optimistic that they will be able to afford it in the future.

#2 The owner (seller) offers an alternative

If the current owner of the house is motivated to strike a deal, they may offer the potential buyer the opportunity to move into the house as a tenant and pay monthly rent, with the option to purchase the house in the future.

#3 Rental agreement and cash for the option to buy

At this point, the potential buyer enters into a rental agreement with the owner of the house and pays upfront cash for the option to buy the house at a future date. The cost of the option is negotiated between the buyer and the seller and may be anywhere between 2% and 7%, but can vary widely.

#4 Specific terms and conditions

There are many specific terms and conditions that can be built into the Rent to Own agreement. The main terms and conditions include:

- The monthly rental rate ($/month)

- The term of the rental agreement (e.g., 3 years)

- Credits from the rent paid towards the purchase of the home (e.g., 20% of all rent paid is credited against the purchase price)

- Cost of the option to buy (e.g., 4% of the value of the property)

- Expiration date of the option (e.g., 3 years after signing the contract)

- Property purchase price (e.g., $1.2 million, or a price to be determined in the future)

- Cost of ending the rental agreement early (e.g., 3-month rent penalty)

- Assignability (e.g., if the option can be sold to another party or not)

- Other terms and conditions as the buyer and seller see fit

Learn About Finance and Financial Analysis

Anyone considering performing their own analysis of a Rent to Own transaction may wish to brush up on their financial analysis skills before jumping in. There is a lot at stake with a transaction like this and it’s important to understand exactly how the economics work.

To learn the fundamentals of accounting, finance, Excel, and financial analysis, CFI has published Free financial training courses to teach you exactly what you need to know.

Check out all of CFI’s financial analyst courses now!

Additional Resources

Thank you for reading this educational guide on a Rent to Own contract for a house. To keep learning with more free resources from CFI, check out these additional guides: