Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

The mathematical average of a sequence of returns that have accrued over time

Average return is the mathematical average of a sequence of returns that have accrued over time. In its simplest terms, average return is the total return over a time period divided by the number of periods.

Average return, as in simple average, is calculated by adding a set of numbers into a single sum. Although there are several concepts used to calculate the average return, the arithmetic average return is computed by taking the total sum of numbers divided by the total count of the numbers in the series as given by the following formula:

Investors and market analysts use the average return to determine the past returns for stock or security. The average return is also used to establish the yields of a company’s portfolio.

Annualized return is compounded when reporting the previous returns, while average return ignores compounding. An average annual return is commonly used to measure returns of equity investments.

However, because it compounds, the annual average return is typically not considered an ideal analysis metric; hence, it is infrequently used to evaluate changing returns. Also, the annualized return is computed using a regular mean.

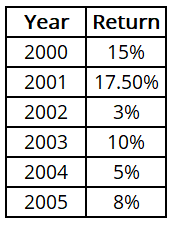

Simple arithmetic mean is one typical example of average return. Consider a mutual investment returns the following every year over six full years, as shown below.

The average return for six years is computed by summing up the annual returns and divided by 6, that is, the annual average return is calculated as below:

Annual Average Return = (15% +17.50% + 3% + 10% + 5% + 8%) / 6 = 9.75%

Alternatively, consider hypothetical returns of Wal-Mart (NYSE: WMT) between 2012 and 2017. The returns on investments for the company are shown in the table below:

The average return for Wal-Mart over six years is calculated using the same approach.

Average Return = (8.9% + 29.1% + 13.3% + 41.7% – 7.6% + 23.5% / 6 = 18.15%

The average growth rate is used to assess an increase or decrease in the value of an investment over a period of time. The growth rate is computed using the growth rate formula:

For example, assume that an investor invested $100,000 in an investment product, and the stock prices fluctuated from $100 to $250. Using the above formula to calculate the average return gives the following:

Growth Rate = ($250 – $150) / $250 = 60%, which means the returns will now be $160,000.

The geometric average proves to be ideal when analyzing average historical returns. What sets the geometric mean apart is that it assumes the actual value invested.

Computation only pays attention to the return values and applies a comparison concept when analyzing the performance of more than a single investment over multiple time periods.

The geometric average return takes care of the outliers resulting from money inflows and outflows over time. For this reason, it is also known as the time-weighted rate of return (TWRR). A further unique feature of the TWRR is that it factors the timing and size of cash flows.

It makes the TWRR a precise measure of returns on a portfolio that has had withdrawals or other transactions – such as receipt of interest payments and deposits. The money-weighted rate of return (MWRR) is the same as the internal rate of return, where zero is the net current value.

Despite its preference as an easy and effective measure for internal returns, the average return has several pitfalls. It does not account for different projects that might require different capital outlays.

In the same vein, it ignores future costs that may affect profit; rather, it only focuses on projected cash flows resulting from a capital injection. Also, average return does not consider the rate of reinvestment; instead, it implicitly assumes that future cash flows can be reinvented at similar rates as the internal rates of return.

This assumption is impractical, given that sometimes the internal rate of return can yield a high number, and the factors for such return may be limited or unavailable in the future. Due to these flaws, investors and analysts opt to use money-weighted return or geometric mean as the alternative metric for analysis.

Thank you for reading CFI’s guide on Average Return. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: