Bull Call Spread

An options strategy that involves purchasing an in-the-money (ITM) call option and selling an out-of-the-money (OTM) call option with a higher strike price

What is a Bull Call Spread?

A bull call spread, which is an options strategy, is utilized by an investor when he believes a stock will exhibit a moderate increase in price. A bull spread involves purchasing an in-the-money (ITM) call option and selling an out-of-the-money (OTM) call option with a higher strike price but with the same underlying asset and expiration date. A bull call spread should only be used when the market is exhibiting an upward trend.

Formulas for Bull Call Spread

To determine the maximum profit, maximum loss, and break-even point for a bull call spread, refer to the following formulas:

Understanding a Bull Call Spread

Consider the following example:

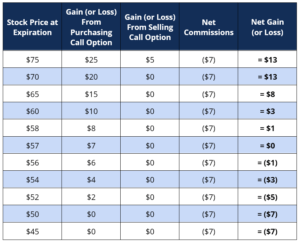

An investor utilizes a bull call spread by purchasing a call option for a premium of $10. The call option comes with a strike price of $50 and expires in July 2020. At the same time, the investor sells a call option for a premium of $3. The call option comes with a strike price of $70 and expires in July 2020. The underlying asset is the same and is currently trading at $50. Summarizing the information above:

In writing the two options, the investor witnessed a cash outflow of $10 from purchasing a call option and a cash inflow of $3 from selling a call option. Netting the amounts together, the investor sees an initial cash outflow of $7 from the two call options.

Now, assume that it is July 2020. The table below illustrates theoretical stock prices at the expiration date.

At a price of $60 or above, the investor’s gain is capped at $3 because both the long call option and short call option is in-the-money. For example, at the stock price of $65:

- The investor would gain through its long call position by being able to purchase at a strike price of $50 and sell at the market price of $65; and

- The investor would lose through its short call position by having to purchase at the market price of $65 and selling it to the option holder at $60.

Factoring in net commissions, the investor would be left with a net gain of $3.

At a price of $50 or below, the investor’s loss is capped at -$7, because both the long call option and short call option are out-of-the-money. For example, at the stock price of $45:

- The investor would not gain from its long call position; and

- The investor would not lose from its short call position.

Factoring in net commissions, the investor would be left with a net loss of $7.

Therefore, in a bull call spread, the investor is:

- Limited to the maximum loss equal to net commissions; and

- Limited to the maximum gain equal to the difference in strike prices between the short and long call and net commissions.

Applying the formulas for a bull call spread:

- Maximum profit = $70 – $50 – $7 = $13

- Maximum loss = $7

- Break-even point = $50 + $7 = $57

The values correspond to the table above.

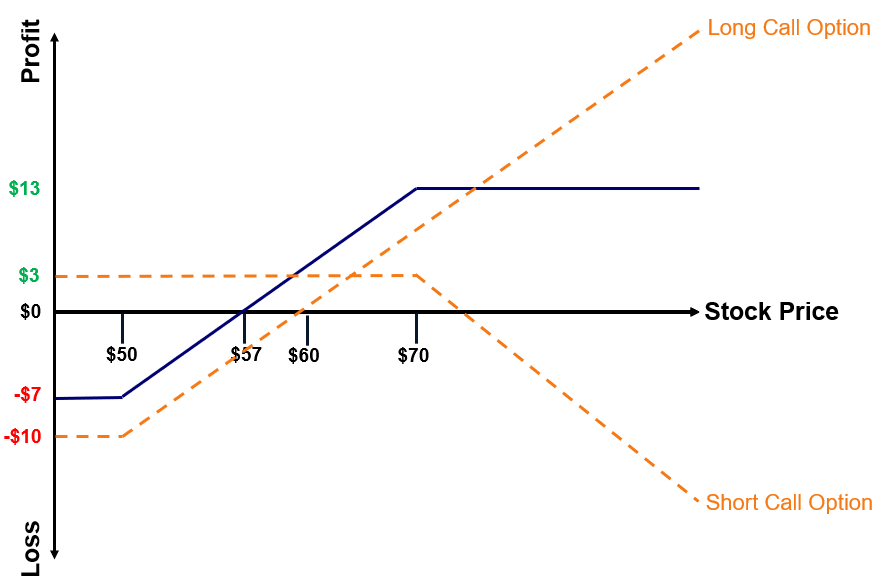

Visual Representation

The comprehensive example above can be visually represented as follows:

Where:

- The blue line represents the pay-off; and

- The dotted yellow lines represent a long call option and a short call option.

Note that the blue line is simply a combination of the two dotted yellow lines.

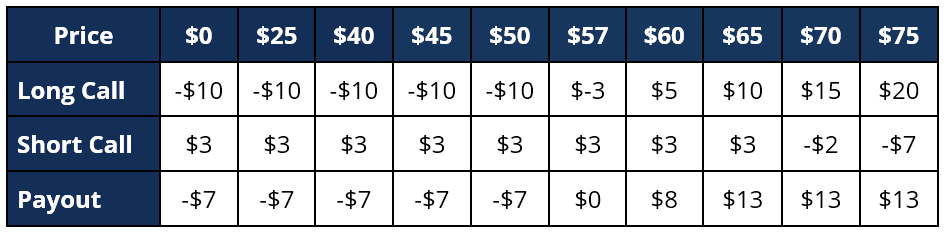

The payout table below corresponds to the visual graph above.

Example of a Bull Call Spread

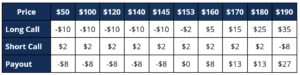

Jorge is looking to utilize a bull call spread on ABC Company. ABC Company is currently trading at a price of $150. He purchases an in-the-money call option for a premium of $10. The strike price for the option is $145 and expires in January 2020. Additionally, Jorge sells an out-of-the-money call option for a premium of $2. The strike price for the option is $180 and expires in January 2020.

What are the maximum payout, maximum loss, and break-even point of the bull call spread above?

The net commission is $8 ($2 OTM Call – $10 ITM Call).

Applying the formulas for a bull call spread, Jorge determines the:

- Maximum profit = $180 – $145 – $8 = $27

- Maximum loss = $8

- Break-even point = $145 + $8 = $153

To confirm, Jorge creates a payout table:

Benefits and Drawbacks of Using a Bull Call Spread

The primary benefit of using a bull call spread is that it costs lower than buying a call option. In the example above, if Jorge only used a call option, he would need to pay a $10 premium. Through using a bull call spread, he only needs to pay a net of $8. In addition to being cheaper, the losses are lower as well. If the stock dropped to $0, Jorge would only realize a loss of $8 versus $10 (if he were to just use a long call option).

However, one significant drawback from using a bull call spread is that potential gains are limited. For example, in the example above, the maximum gain Jorge can realize is only $27 due to the short call option position. Even if the stock price were to skyrocket to $500, Jorge would only be able to realize a gain of $27.

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: