Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Stochastic model used to evaluate the volatility of an underlying asset

The Heston model is a stochastic model used to evaluate the volatility of an underlying asset. Like other stochastic models, the Heston model assumes that the volatility of an asset follows a random process rather than a constant or deterministic process.

The Heston model was developed to help price options while accounting for variations in the asset’s price and volatility. When pricing options, one aspect to consider is market volatility and its effects on asset prices.

To account for this volatility, the Heston model was developed to address an asset’s volatility as a stochastic process. As such, it stands out in comparison to other models, including the Black-Scholes model that treats volatility as a constant.

Developed by mathematician Steven Heston in 1993, the Heston model was created to price options, which are a type of financial derivative. Unlike other financial assets such as equities, the value of an option is not based on the value of an asset but rather the change in an underlying asset’s price.

Each option is a contract between a buyer and seller, which gives the holder of the option the right to buy or sell the underlying asset at a specific price. All options have a specific expiration date, at which point the contract must be executed at the previously set price or risk expiring.

However, the volatility of options depends on the price and maturity. Therefore, the Heston model was designed to price an option while accounting for these variations in market volatility.

There are two categories of options: calls and puts. Calls allow the holder to buy at a specific price, and puts allow the holder to sell at a specific price.

Once a call or put option has been purchased, the date at which the holder can buy or sell depends on whether it is an American or European option. American options allow the holder to execute the option anytime before the expiry date, while European options only allow the holder to execute the option on the expiry date. It’s important to note that the Heston model is only capable of pricing European options.

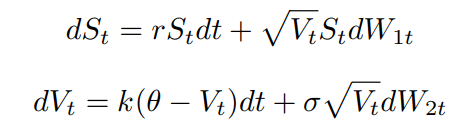

Mathematically, the Heston model assumes that asset prices are determined by a stochastic process. To calculate the underlying price of an asset, the model uses the following equations:

In the equations above, the variables are defined as:

Note that the Brownian motions are random processes that exhibit the following properties:

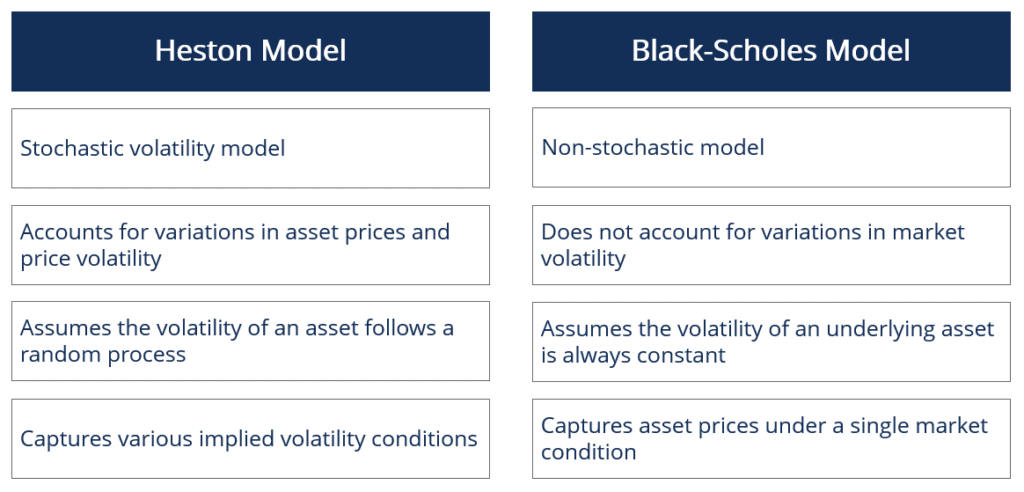

In the realm of quantitative finance, the Black-Scholes model is the most well-known option-pricing model due to its simplicity and widespread use. However, it is not stochastic and therefore assumes that the volatility of an underlying asset is always constant.

Under actual market conditions, the volatility of options tends to vary due to factors such as price and maturity. As such, the model does not account for variations in asset prices and price volatility.

In contrast, the Heston model is a stochastic volatility model and accounts for variations in the asset’s price and volatility. Therefore, this model assumes that the volatility of an asset follows a random process rather than a constant one.

In general, it captures market conditions more accurately than the Black-Scholes model by providing an overview of various implied volatility conditions.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)® certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: