Put-Call Parity Calculator

Download CFI's free put-call parity calculator

Put-Call Parity Excel Calculator

This put-call parity calculator shows the relationship between a European call option, put option, and their underlying asset. By inputting information, you can see what any of these variables should be if this parity relationship were to be held.

Below is a quick preview of CFI’s put-call parity calculator:

Download the Free Calculator

Enter your name and email in the form below and download the free calculator now!

About the Put-Call Parity

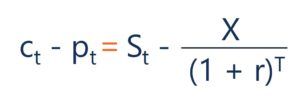

This parity demonstrates how a European call option, put option, and their underlying asset is related. This parity holds only for European options with the same underlying asset, strike price, and expiration date. This concept is important in options pricing. Below is a common version of the equation:

The relationship states that a portfolio consisting of a long position on a call option and a short position on a put option should be equal to a long position on the underlying asset, and a short position on the strike price. The equation can be rearranged in a number of ways to solve for any specific variable.

For example, according to the put-call parity, a long position on the call option should be equal to a portfolio holding a long position on the put option, a long position on the underlying asset and a short position on the strike price. The portfolio can be referred to as the synthetic call option. In the put-call calculator, by entering the information for the put option, underlying asset, and strike price you can easily calculate what the put option should be based on the put-call parity.

This concept is important to understand, because if it does not hold then that could potentially lead to an opportunity for arbitrage. For example, if the price of a call option is less than the synthetic call option, that would mean there is mispricing and you could employ an arbitrage strategy. In this case, you would sell the synthetic call option and buy the actual call option.

Additional Resources

For more resources, check out CFI’s Business Templates Library to download numerous free Excel modeling, PowerPoint presentation, and Word document templates. Also, see all our derivatives resources.