Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

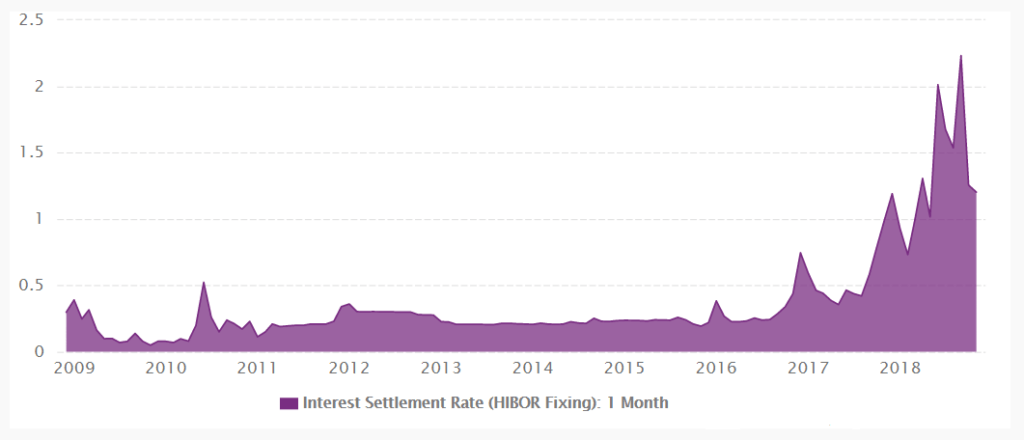

The benchmark interest rate for lending between banks in the Hong Kong interbank market

The Hong Kong Interbank Offered Rate (HIBOR) is the benchmark interest rate that lenders and borrowers use for interbank lending in the Hong Kong market. The reference rate is used on Hong Kong dollar-denominated financial instruments for specified durations ranging from overnight borrowing to one year.

Banks use HIBOR to transfer funds and currencies across other banks and to manage their liquidity. If the bank’s cash reserves fall below the required levels, it borrows funds at the Hong Kong interbank market at the HIBOR rate.

The rate is also used as a reference rate by other banks in the wider Asian economy. HIBOR works in the same way as LIBOR, which is the benchmark interest rate that large banks use to lend to each other short-term loans in the London interbank market.

HIBOR is calculated based on the quotations from 20 designated banks. The banks are selected by the Hong Kong Association of Banks (HKAB) every two years on the recommendation of the Treasury Market Association. The selection process is based on the bank’s reputation, credit standing, and the level of activity in the Hong Kong dollar market. The rates are determined every day at 11:00 a.m., except on Saturdays. Each of the designated banks is required to submit their estimated offer rate that is quoted to other banks in the interbank market.

The highest three quotations and the lowest three contributed values are eliminated, and the remaining 14 quotations are considered in arriving at the HIBOR rate. The “trimmed mean” of the 14 quotations is then calculated, and the result is rounded up to the nearest fifth decimal point where appropriate.

Banks obtain the daily HIBOR fixings on the HKAB’s website, while the rates contributed by the 20 reference banks are available from four main information vendors – Thomson Reuters, Tullett Prebon, Quick, and Bloomberg. The Hong Kong Interbank Clearing Limited is the official calculating agent for the fixings, and it releases the information to the four information vendors.

HIBOR is a market-driven product that is released directly by the banking industry through HKAB. The rate is used in various financial instruments, such as residential mortgage loan contracts, interest rate swaps, HKD forward rate agreements, and syndicated loan agreements. The demand for HIBOR over other benchmark interest rates stems from its important role in interest rate risk management.

Usually, market participants want the flexibility to choose between a floating rate and fixed-rate financial instruments to reduce their risk exposure. However, for the floating-rate instruments to be accepted in the market, there must be a stable floating interest rate benchmark that represents market interest rates. Such a market demand created opportunities for various interest rate benchmarks such as HIBOR in the Hong Kong interbank market.

The main function of HIBOR is to serve as a benchmark reference rate for debt instruments in Hong Kong and the broader Asian markets. Some of the financial instruments that use the rate include mortgages, interest rate swaps, corporate bonds, and other financial instruments.

Take an example of an HKD-denominated floating-rate note that pays coupons based on HIBOR plus a margin of 28 basis points annually. The coupon payment considers the current annual HIBOR rate plus the 28 basis points spread.

Since HIBOR is an annualized rate that changes every year, the coupon rate is reset every year to consider the new HIBOR for the year plus the predetermined basis point spread. For example, if the HIBOR rate at the start of the succeeding year is 5%, the coupon rate will be calculated as 5.28% of the par value of the bond to determine the actual return.

LIBOR and HIBOR represent the interest rates that banks are willing to lend to each other in the interbank market in their respective regions.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: