Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

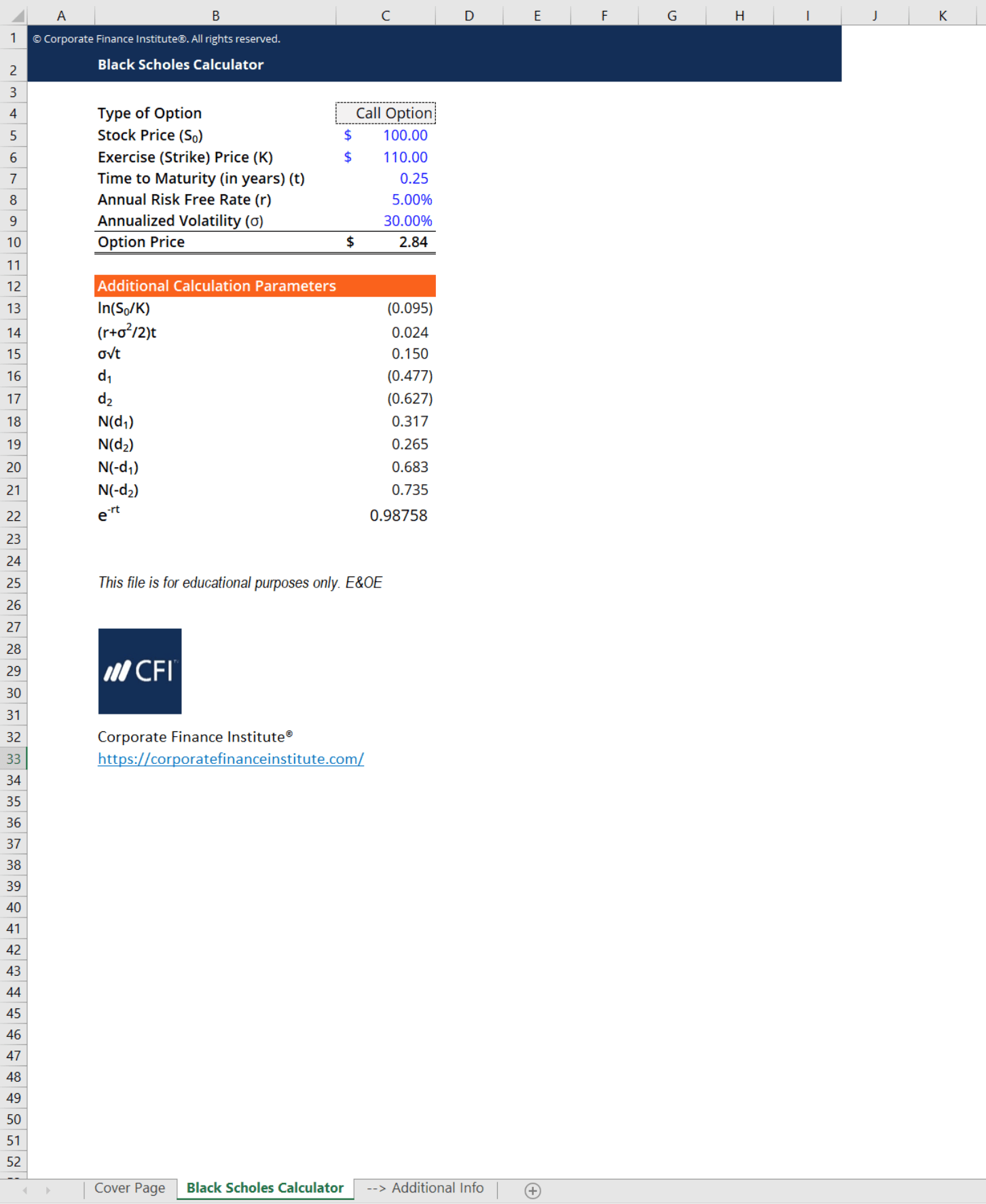

Download our free Black Scholes calculator

This Black Scholes calculator uses the Black-Scholes option pricing method to help you calculate the fair value of a call or put option.

Here is a brief preview of CFI’s Black Scholes calculator.

Download CFI’s Excel template to advance your finance knowledge and perform better financial analysis.

CFI’s Black Scholes calculator uses the Black-Scholes option pricing method. Other option pricing methods include the binomial option pricing model and the Monte-Carlo simulation.

The Black-Scholes option pricing method focuses purely on European options on stocks. European options, which can only be exercised on the expiry date of the option. American options, which can be exercised early, cannot be priced using the Black-Scholes option pricing method.

Using this method, the Black Scholes calculator makes a few assumptions that you will need to remember:

The main variables calculated and used in the Black Scholes calculator are:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the Black-Scholes Calculator. Check out our business templates library to download numerous free Excel modeling, PowerPoint presentation, and Word document templates.