Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

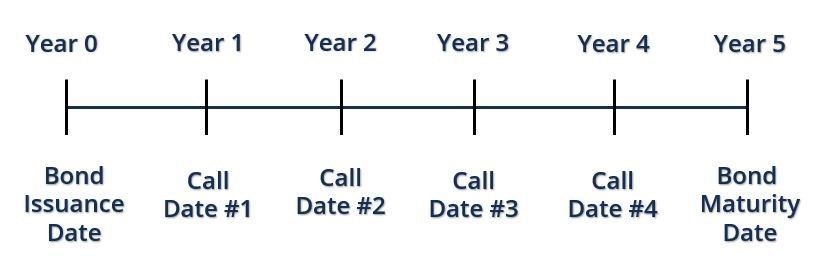

The date when a callable bond can be redeemed for a specific call price before its maturity date

A call date refers to the date when a callable bond can be redeemed for a specific call price before its maturity date. There can be more than one call date where the issuer owns the right to redeem the bond prematurely before the bond’s maturity date.

The callable bond can be redeemed at par or at a premium. The call price that can be redeemed on the call date is predetermined, and the specific details of the date(s) can be found in the bond’s prospectus.

If a callable bond comes with multiple call dates, there will be a call schedule. A call schedule lists all the dates that the bond can be redeemed at specific prices before its maturity date. In the bond’s prospectus, it will specify the value that the bond can be redeemed for each of the call dates.

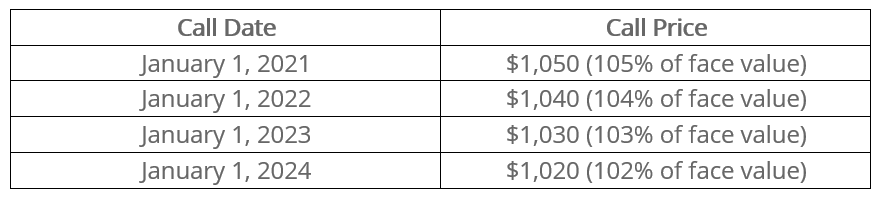

For example, suppose that Company X issued a callable bond on January 1, 2020, with a face value of $1,000, and the bond would mature on January 1, 2025. The callable bond is offered with an interest rate of 10%. Company X is also offering the choice for the bond to be redeemed before the maturity date with the following call schedule:

In the above example, the bond can be redeemed at a small premium because the call price is slightly higher than the bond’s face value of $1,000.

An issuer may want to redeem a bond on the call date if there is a benefit from redeeming the bond before its maturity date.

For example, if interest rates are declining, the bond issuer may want to redeem the bond to avoid paying the investor interest at rates higher than the average market rate. When redeeming the bond, the issuer must pay the investor the call price. After redeeming the bond, the issuer may want to issue the bond again at a lower interest rate.

On the other hand, an issuer may not want to redeem a bond prematurely if interest rates are increasing above the bond’s interest rate. Redeeming the bond early means that the issuer will need to stop paying lower-than-average interest rates to the investor. If the issuer redeems the bond and issues the bond again, the issuer must pay higher interest rates, which is not favorable.

Callable bonds are riskier than non-callable bonds for investors since there is a chance that the issuer may redeem the bond earlier than its maturity date. As a result, the investor may have to reinvest in another bond with a lower interest rate.

In order to compensate for the risk, callable bonds usually offer higher coupon rates and a higher call price when it is redeemed. For example, a callable bond may be issued at a face value of $5,000. When it is redeemed on a call date, it can be redeemed at a slight premium, such as $5,100.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)® certification program. It also offers a variety of lessons and courses for you to continue learning about topics related to investing: