Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A trading strategy that exploits arbitrage opportunities among three currencies

A triangular arbitrage opportunity is a trading strategy that exploits the arbitrage opportunities that exist among three currencies in a foreign currency exchange. The arbitrage is executed through the consecutive exchange of one currency to another when there are discrepancies in the quoted prices for the given currencies.

A triangular arbitrage opportunity occurs when the exchange rate of a currency does not match the cross-exchange rate. The price discrepancies generally arise from situations when one market is overvalued while another is undervalued.

The nature of foreign currency exchange markets limits the price discrepancies between different currencies to a few cents or even to a fraction of a cent. Therefore, the transactions in a triangular arbitrage opportunity involve trading large amounts of money.

Frequently, the transactions employ margin trading to amplify the returns. In addition, a trader must be aware of the transaction costs. It is possible that high transaction costs may erase gains from the price discrepancies.

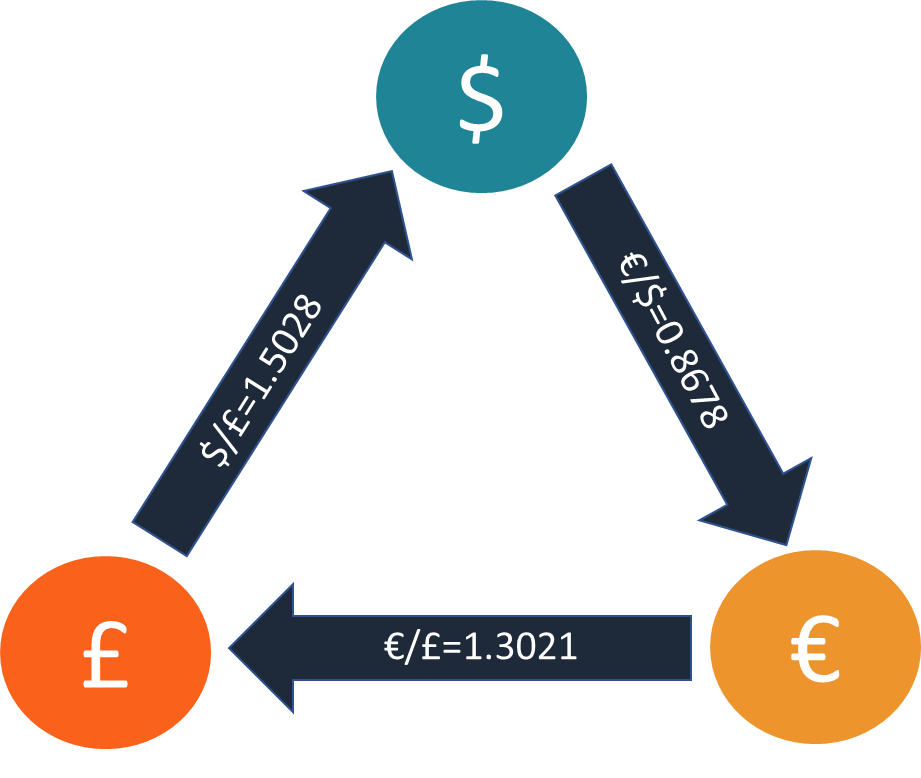

Sam is an FX trader with $1 million on hand. He detects the following exchange rates:

Using the cross-rate formula, Sam determines that the €/£ rate is undervalued. The cross-rate for the pair must be equal:

€/£ = 0.8678 x 1.5028 = 1.3041

Triangular arbitrage can be applied to the three currencies – the US dollar, the euro, and the pound. To execute the triangular arbitrage opportunity, Sam should perform the following transactions:

By utilizing the discrepancies in the price quotations of the three currencies, Sam managed to turn his initial $1,000,000 into $1,001,558.90, with a profit of $1,558.90. Note, that due to the small price discrepancy (only 0.002), even the use of a substantially large capital resulted in relatively small profits. In our simplified example, we did not account for transaction costs. Therefore, in real life, the profit would be even smaller.

Triangular arbitrage opportunities rarely exist in the real world. This can be explained by the nature of foreign currency exchange markets. Forex markets are extremely competitive with a large number of players, such as individual and institutional traders. The competition in the markets constantly corrects the market inefficiencies and arbitrage opportunities do not last long.

Nowadays, triangular arbitrage opportunities are often exploited by high-frequency traders. Using high-speed algorithms, the traders can quickly spot mispricing and immediately execute the necessary transactions. However, the strong presence of high-frequency traders makes the markets even more efficient. Thus, the number of available arbitrage opportunities diminish.

In addition, the triangular arbitrage strategy provides applications in cryptocurrency trading. Cryptocurrency markets and exchanges are still in development, and more arbitrage opportunities exist in such markets relative to the traditional currency markets.

Thank you for reading CFI’s guide on Triangular Arbitrage Opportunity. To keep learning and advancing your career, the following resources will be helpful: