Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Budgeting method where activities are thoroughly analyzed to predict costs

Activity-based budgeting (ABB) is a budgeting method where activities are thoroughly analyzed to predict costs. ABB does not take historical costs into account when creating a budget.

While a traditional budgeting method adjusts previous costs based on inflation or changes in business activity, activity-based budgeting is a much more thorough way of looking at costs.

Every cost incurred by a business will be looked at closely to determine if efficiencies can be created and costs reduced. It can be in the form of a reduction in activity levels or a complete removal of unnecessary activities. Ultimately, ABB aims to analyze business cost drivers and enable the business to become more profitable.

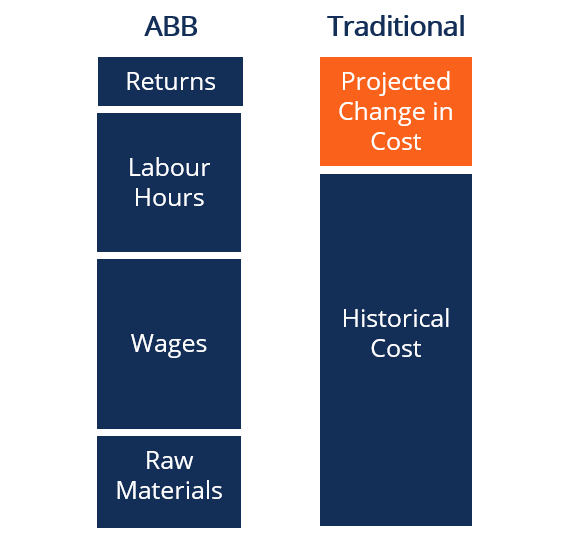

The diagram above demonstrates how ABB budgeting differs from a traditional budgeting method. While a traditional method simply increases or decreases projected costs based on historical values, ABB breaks down costs more gradually.

ABB follows three main steps:

For example, the cost drivers for a manufacturing facility can be the total labor hours and wages paid to employees.

For example, the manufacturing facility may always need three people on the production line, translating to 240 labor hours per week.

For example, wages for warehouse labor can be $12 per hour.

Businesses must analyze their goals and requirements to determine whether an ABB system will make sense to implement. ABB is better suited to new businesses that lack historical costing data that more established businesses have.

For example, a more established retail business, such as Walmart, has made changes to optimize its strategy for profitability over many years. Their profits are going to remain at a relatively even growth rate, and they know exactly what their cost drivers are.

On the other hand, a new start-up doesn’t have years of historical financial information at its disposal. It may be worthwhile for the newer start-up to inspect each cost driver and their corresponding activity levels to make more accurate financial projections.

Relative to other budgeting methods, ABB allows you to see exactly what the associated costs are for each operational activity. It also helps to further break down these costs to determine what can be hurting the profitability of a company.

While other methods of budgeting look at the costs of inputs to perform activities, ABB looks at the outputs that drive costs. In doing so, management can better evaluate different business units relative to each other and allocate capital where they deem to be most profitable.

The biggest disadvantage of implementing ABB is that it is more costly and time-consuming to implement than other budgeting methods. As all costs associated with a business activity are tracked, all technical details must be recorded as they occur.

Furthermore, accountants handling ABB need to have a deep understanding of the business processes. This can be difficult, especially in businesses with complex production cycles. Businesses need to decide if increased forecasting accuracy is worth the extra investment needed to implement an ABB system.

To demonstrate how ABB can be implemented, it is useful to compare it to a traditional budgeting method. Suppose Company ABC expects to sell 1,000 units of its product over the next month, and the product costs $5 to produce. Under activity-based budgeting, the company will estimate the cost of goods sold to be $5,000.

Also, assume Company ABC reported a cost of goods sold at $4,000 last month, with the rate of increase averaging 10% each month in the past. Under the traditional budgeting method, the company will estimate the cost of goods sold in the upcoming month to be $4,400 [$4,000 + ($4,000 x 10%)].

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.