Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A trade credit that gives a 2% discount if payment is received within 10 days

2/10 Net 30 refers to the trade credit offered to a customer for the sale of goods or services. It means that if the amount due is paid within 10 days, the customer will enjoy a 2% discount. Otherwise, the amount is due in full within 30 days.

The CEO of Company A faces decreasing sales due to fierce competition in the marketplace. The CEO believes that the reason sales are declining is due to the company not offering trade credits. In fact, Company A is the only company in the industry that does not offer trade credits to customers. Then Company A sets up a new trade credit term for customers – 2/10 net 30. Customers who purchase on credit are given 30 days to settle their obligation. However, if paid within 10 days, customers enjoy a 2% discount on the goods purchased.

If a customer purchases $10,000 from Company A on the terms 2/10 net 30 and pays within 10 days, the customer only needs to pay $10,000 x 0.98 = $9,800. On the other hand, if the customer pays after 10 days, he must pay the full amount of $10,000.

There are two methods of accounting for discounts: Net method and Gross method.

Let us consider the following example:

A customer of Company A, realizing that the company is offering credit terms of 2/10 net 30, decides to make a purchase of $1,000. The net method and gross method journal entries are provided below:

The net method records the receivables at the sale price less the cash discount. The company would need to make an adjustment for the interest earned if the customer does not take advantage of the discount.

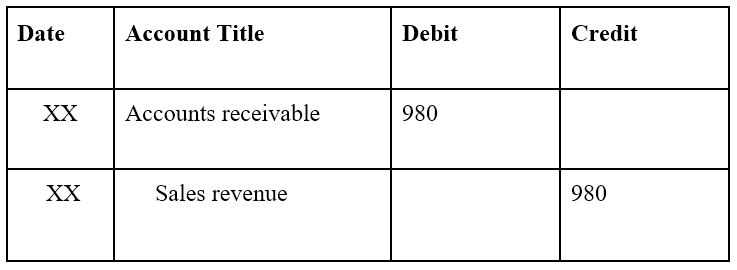

The initial journal entry:

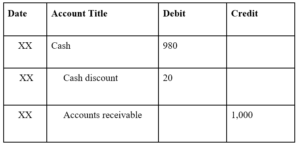

Note: $1,000 x 0.98 = $980. The net method records the receivables at the sale price less the cash discount.

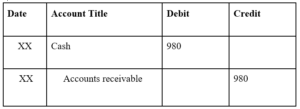

If the customer pays within 10 days and takes advantage of the 2% discount:

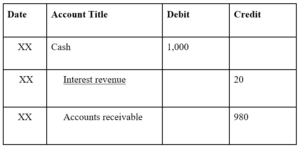

If the customer pays after 10 days and does not take advantage of the 2% discount:

The gross method records the face value of receivables. If the customer takes advantage of the discount, the company will reduce its revenue in the income statement.

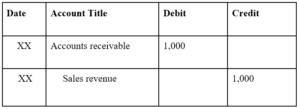

The initial journal entry:

Note: The gross method records the receivables at face value.

If the customer pays within 10 days and takes advantage of the 2% discount:

Note: Cash discount goes on the income statement to reduce revenue.

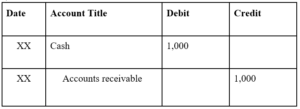

If the customer pays after 10 days and does not take advantage of the 2% discount:

From a supplier’s perspective, trade credit is offered to facilitate more frequent and higher volume purchases. The flexibility in the time of payment attracts more customers and generates more sales for the company.

From a purchaser’s perspective, trade credit allows buyers to make purchases without immediately parting with their cash. Therefore, it also offers flexibility in that buyers can make purchases when there is no cash on hand.

The biggest risk to a supplier when offering trade credit is the potential for bad debt. Since cash does not immediately switch hands in a purchase, the buyer may end up not paying for the purchases. When companies offer trade credit, an allowance for doubtful accounts is set up to anticipate the amount of bad debts from credit purchases.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to 2/10 Net 30. To keep advancing your career, the additional free CFI resources below will be useful: