Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An entry made at the end of an accounting period to recognize an income or expense in the period that it is incurred

An adjusting journal entry is usually made at the end of an accounting period to recognize an income or expense in the period that it is incurred. It is a result of accrual accounting and follows the matching and revenue recognition principles.

Generally, adjusting journal entries are made for accruals and deferrals, as well as estimates. Sometimes, they are also used to correct accounting mistakes or adjust the estimates that were previously made.

In accrual accounting, revenues and the corresponding costs should be reported in the same accounting period according to the matching principle. The revenue recognition principle also determines that revenues and expenses must be recorded in the period when they are actually incurred.

However, in practice, revenues might be earned in one period, and the corresponding costs are expensed in another period. Also, cash might not be paid or earned in the same period as the expenses or incomes are incurred. To deal with the mismatches between cash and transactions, deferred or accrued accounts are created to record the cash payments or actual transactions.

At a later time, adjusting entries are made to record the associated revenue and expense recognition, or cash payment. A set of accrual or deferral journal entries with the corresponding adjusting entry provides a complete picture of the transaction and its cash settlement.

Similar to an accrual or deferral entry, an adjusting journal entry also consists of an income statement account, which can be a revenue or expense, and a balance sheet account, which can be an asset or liability.

There are also many non-cash items in accrual accounting for which the value cannot be precisely determined by the cash earned or paid, and estimates need to be made. The entries for these estimates are also adjusting entries, i.e., impairment of non-current assets, depreciation expense and allowance for doubtful accounts.

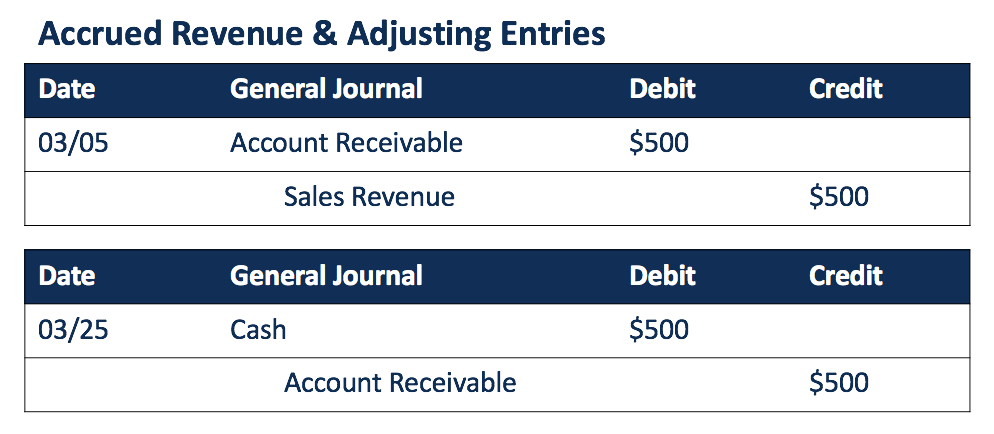

An accrued revenue is the revenue that has been earned (goods or services have been delivered), while the cash has neither been received nor recorded. A typical example is credit sales. The revenue is recognized through an accrued revenue account and a receivable account. When the cash is received at a later time, an adjusting journal entry is made to record the cash receipt for the receivable account.

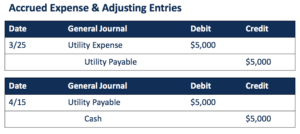

An accrued expense is an expense that has been incurred (goods or services have been consumed) before the cash payment has been made. Examples include utility bills, salaries and taxes, which are usually charged in a later period after they have been incurred.

When the cash is paid, an adjusting entry is made to remove the account payable that was recorded together with the accrued expense previously.

In contrast to accruals, deferrals are cash prepayments that are made prior to the actual consumption or sale of goods and services.

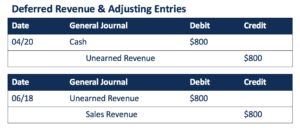

For deferred revenue, the cash received is usually reported with an unearned revenue account. Unearned revenue is a liability created to record the goods or services owed to customers. When the goods or services are actually delivered at a later time, the revenue is recognized and the liability account can be removed.

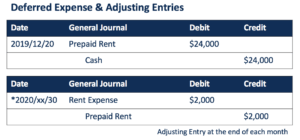

When expenses are prepaid, a debit asset account is created together with the cash payment. The adjusting entry is made when the goods or services are actually consumed, which recognizes the expense and the consumption of the asset.

Prepaid insurance premiums and rent are two common examples of deferred expenses. If the rent is paid in advance for a whole year but recognized on a monthly basis, adjusting entries will be made every month to recognize the portion of prepayment assets consumed in that month.

When the exact value of an item cannot be easily identified, accountants must make estimates, which are also considered adjusting journal entries. Taking into account the estimates for non-cash items, a company can better track all of its revenues and expenses, and the financial statements reflect a more accurate financial picture of the company.

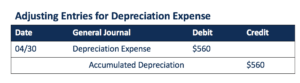

For example, depreciation expense for PP&E is estimated based on depreciation schedules with assumptions on useful life and residual value. Depreciation expense is usually recognized at the end of a month.

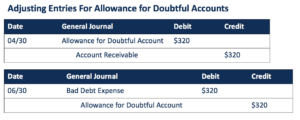

Allowance for doubtful accounts is also an estimated account. It identifies the part of accounts receivable that the company does not expect to be able to collect. It is a contra asset account that reduces the value of the receivables. When it is definite that a certain amount cannot be collected, the previously recorded allowance for the doubtful account is removed, and a bad debt expense is recognized.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.