Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The amount of accounts receivable that a company does not expect to collect

The allowance for doubtful accounts is a contra-asset account that is associated with accounts receivable and serves to reflect the true value of accounts receivable. The amount represents the estimated value of accounts receivable that a company does not expect to receive payment for.

For example, say a company lists 100 customers who purchase on credit, and the total amount owed is $1,000,000. The $1,000,000 will be reported on the balance sheet as accounts receivable. The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay the full amount they owe. Rather than waiting to see exactly how payments work out, the company will debit a bad debt expense and credit allowance for doubtful accounts.

Using the example above, let’s say that a company reports an accounts receivable debit balance of $1,000,000 on June 30. The company anticipates that some customers will not be able to pay the full amount and estimates that $50,000 will not be converted to cash. Additionally, the allowance for doubtful accounts in June starts with a balance of zero.

To account for the estimated $50,000 that will not be converted to cash:

| Date | Account Title | Debit | Credit |

| June 30, 2017 | Bad Debts Expense | $50,000 | |

| Allowance for Doubtful Accounts | $50,000 |

With the account reporting a credit balance of $50,000, the balance sheet will report a net amount of $9,950,000 for accounts receivable. This amount is referred to as the net realizable value of the accounts receivable – the amount that is likely to be turned into cash. The debit to bad debts expense would report credit losses of $50,000 on the company’s June income statement.

Above, we assumed that the allowance for doubtful accounts began with a balance of zero. If, instead, the allowance for uncollectible accounts began with a balance of $10,000 in June, we would make the following adjusting entry instead:

$50,000 – $10,000 = $40,000 (adjusting entry)

| Date | Account Title | Debit | Credit |

| June 30, 2017 | Bad Debts Expense | $40,000 | |

| Allowance for Doubtful Accounts | $40,000 |

Later, a customer who purchased goods totaling $10,000 on June 25 informed the company on August 3 that it already filed for bankruptcy and would not be able to pay the amount owed. The company would then write off the customer’s account balance of $10,000.

To write off the customer’s account balance of $10,000:

| Date | Account Title | Debit | Credit |

| Aug. 3, 2017 | Allowance for Doubtful Accounts | $10,000 | |

| Accounts Receivable | $10,000 |

After writing off the bad account, the net amount for accounts receivable remains the same: $9,950,000 ($9,990,000 – $40,000). In addition, the bad debt expense remains the same and is not affected by the write-off. The bad debt expense recorded on June 30 already anticipated a credit loss.

The customer who filed for bankruptcy on August 3 managed to pay the company back the amount owed on September 10. The company would then reinstate the account that was initially written off on August 3.

To reverse the write-off:

| Date | Account Title | Debit | Credit |

| Sept. 10, 2017 | Accounts Receivable | $10,000 | |

| Allowance for Doubtful Accounts | $10,000 |

To record the amount paid to the company from the customer:

| Date | Account Title | Debit | Credit |

| Sept. 10, 2017 | Cash | $10,000 | |

| Accounts Receivable | $10,000 |

In the example above, we estimated an arbitrary number for the allowance for doubtful accounts. There are two primary methods for estimating the amount of accounts receivable that are not expected to be converted into cash.

The percentage of credit sales method is explained as follows: If a company and the industry reported a long-run average of 2% of credit sales being uncollectible, the company would enter 2% of each period’s credit sales as a debit to bad debts expense and a credit to allowance for doubtful accounts.

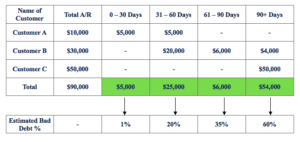

The accounts receivable aging method is a report that lists unpaid customer invoices by date ranges and applies a rate of default to each date range.

Example of an accounts receivable aging chart:

To calculate the allowance for doubtful accounts:

($5000 x 1%) + ($25,000 x 20%) + ($6,000 x 35%) + ($54,000 x 60%) = $39,550

If we assume that the allowance for uncollectible accounts showed a credit balance of $5,000 before adjustment, we will make the following adjusting entry:

$39,550 – $5,000 = $34,550 (adjusting entry)

| Date | Account Title | Debit | Credit |

| Dec. 31, 2017 | Bad Debts Expense | $34,550 | |

| Allowance for Doubtful Accounts | $34,550 |

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Allowance for Doubtful Accounts. In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: