Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An asset account in which the account's balance will either be a zero or a credit (negative) balance

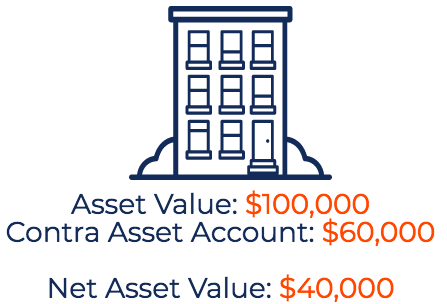

In bookkeeping, a contra asset account is an asset account in which the natural balance of the account will either be a zero or a credit (negative) balance. The account offsets the balance in the respective asset account that it is paired with on the balance sheet.

Normal asset accounts have a debit balance, while contra asset accounts are in a credit balance. Therefore, a contra asset can be regarded as a negative asset account. Offsetting the asset account with its respective contra asset account shows the net balance of that asset.

By reporting contra asset accounts on the balance sheet, users of financial statements can learn more about the assets of a company. For example, if a company just reported equipment at its net amount, users would not be able to observe the purchase price, the amount of depreciation attributed to that equipment, and the remaining useful life. Contra asset accounts allow users to see how much of an asset was written off, its remaining useful life, and the value of the asset.

Some of the most common contra assets include accumulated depreciation, allowance for doubtful accounts, and reserve for obsolete inventory.

Accumulated depreciation is a contra asset account used to record the amount of depreciation to date on a fixed asset. Examples of fixed assets include buildings, machinery, office equipment, furniture, vehicles, etc. The accumulated depreciation account appears on the balance sheet and reduces the gross amount of fixed assets.

Allowance for doubtful accounts (ADA) is a contra asset account used to create an allowance for customers who are not expected to pay the money owed for purchased goods or services. The allowance for doubtful accounts appears on the balance sheet and reduces the amount of receivables.

Reserve for obsolete inventory is a contra asset account used to write down the inventory account if the inventory is considered obsolete. Excess, stored inventory will near the end of its lifespan at some point and, in turn, result in expired or unsellable goods. In this scenario, a write-down is recorded to the reserve for obsolete inventory.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.