Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Direct costs in producing a good or providing a service

Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct labor cost, and direct factory overheads, and is directly proportional to revenue.

As revenue increases, more resources are required to produce the goods or service. COGS is often the second line item appearing on the income statement, coming right after sales revenue. COGS is deducted from revenue to find gross profit.

Cost of Goods Sold consists of all the costs associated with producing the goods or providing the services offered by the company. For goods, these costs may include the variable costs involved in manufacturing products, such as raw materials and labor.

They may also include fixed costs, such as factory overhead, storage costs, and depending on the relevant accounting policies, sometimes depreciation expense.

COGS does not include general selling expenses, such as management salaries and advertising expenses. These costs will fall below the gross profit line under the selling, general and administrative (SG&A) expense section.

The basic purpose of finding COGS is to calculate the “true cost” of merchandise sold in the period. It doesn’t reflect the cost of goods that are purchased in the period and not being sold or just kept in inventory. It helps management and investors monitor the performance of the business.

The IFRS and US GAAP allow different policies for accounting for inventory and cost of goods sold. Very briefly, there are four main valuation methods for inventory and cost of goods sold.

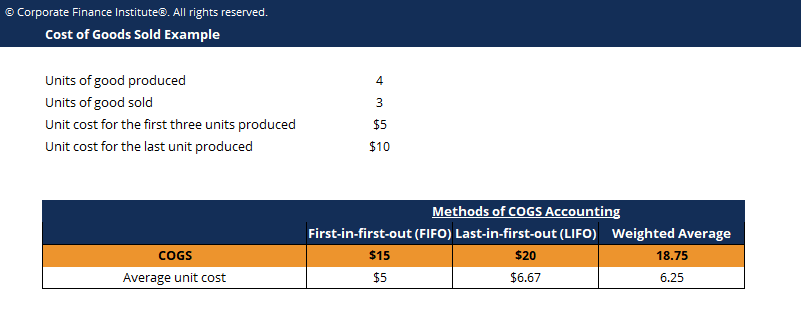

Under FIFO, COGS consists of finished inventory units that were produced first and thus consist of costs incurred first, whereas under LIFO, COGS consists of finished inventory units that were produced last and therefore consist of later or most recent costs. For example, assume that a company purchased materials to produce four units of its goods.

The first three units cost $5 to produce. However, due to rising material prices, the last unit costs $10 to produce. In the subsequent period, the company sold three units. Under FIFO, COGS would consist of the first three units produced, totaling $5 x 3 = $15. Under LIFO, COGS would consist of the last three units produced, totaling $10 x 1 + $5 x 2 = $20.

Under the weighted-average method, the total cost of goods available for sale is divided by the units available for sale to find the unit cost of goods available for sale. This is multiplied by the actual number of goods sold to find the cost of goods sold. In the above example, the weighted average per unit is $25 / 4 = $6.25. Thus, for the three units sold, COGS is equal to $18.75.

Specific identification is special in that it is only used by organizations with specifically identifiable inventory. Costs can be directly attributed and are specifically assigned to the specific unit sold. This type of COGS accounting may apply to car manufacturers, real estate developers, and others.

Depending on the COGS classification used, ending inventory costs will obviously differ.

Learn more about COGS in the video below:

Click the button below to download CFI’s free COGS template!`

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

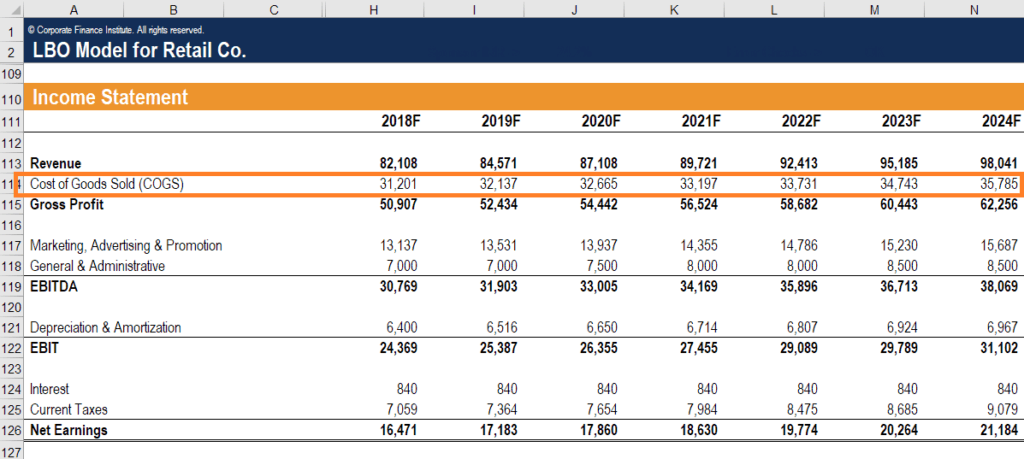

Thank you for reading this guide to accounting for the Cost of Goods Sold. To prepare for the FMVA curriculum, these additional CFI resources will be helpful: