Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

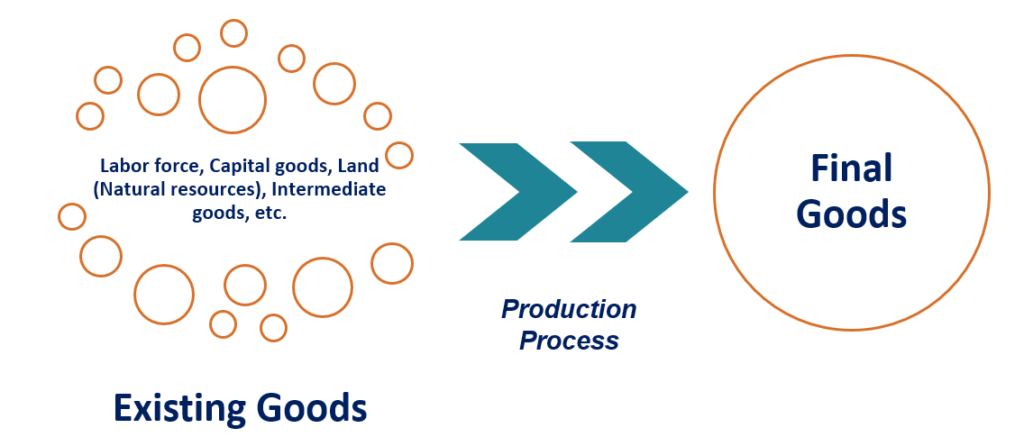

The reduction in the quantity of a factor of production as a result of the production process

Depletion is the reduction in the quantity of a factor of production as a result of the production process. Companies use existing goods and services to create new goods and services. The conversion of existing goods into new goods is known as a production process.

The tax codes of most countries allow businesses to deduct depletion from official tax payments. The depletion deduction is based on the assumption that for certain businesses, accounting profits are greater than real profits. Consider the following example:

Company ABC runs a mining operation that uses heavy machinery (capital) and skilled engineers (labor) to extract shale oil from an oil well (land). The company sells all the oil it extracts in the international oil market. The company is required by law to pay a certain amount of its profits as tax.

For example, the exact tax structure is not important; the tax may be a percentage tax or a lump-sum tax. The oil extraction process reduces the amount of oil available in the oil well for future extraction. It reduces the amount of oil that the company can sell in the future. ABC can, therefore, claim that the profits on which it is paying tax are actually an overestimate of the real profits since the taxed profits do not account for the reduction in future profits.

Percentage depletion refers to when the market value of depletion is assumed to be some constant or varying proportion of a company’s revenue. Therefore, if Company ABC generates $10 million in revenue, and the percentage depletion is 2%, then it can assume that $200,000 of that revenue is a result of resource depletion. The rate is a function of various industry factors. For our example, the rate would depend on various oil industry factors.

Cost depletion allows the value of the depleted natural resource to be spread out over the resource’s lifetime. The computation of the total cost depletion amount requires the following:

Consider the following example: Company ABC owns an oil well that is expected to produce one million oil barrels. The company needs to invest $100,000 before it can extract any oil. In its first year of operation, it extracts 50,000 barrels of oil.

Where:

Therefore, the Depletion Deduction in our example would be 100,000*50,000 / 1,000,000 = 5,000

The general formula for cost depletion substitutes future investment for the initial investment. In the example above, suppose that at the end of the first year, a new company looking to extract oil from Company ABC’s oil well would need to make an initial investment of $80,000.

Therefore, the cost depletion would be given by 80,000*50,000/1,000,000 = 4,000. The general formula assumes that some part of the initial investment is a permanent sunk cost.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: