Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A statutory notice sent by the Internal Revenue Service when a taxpayer’s return does not match with the IRS records

A notice of deficiency is a statutory notice that is sent by the Internal Revenue Service (IRS) to a taxpayer when there is a discrepancy in the tax return. The document is issued when the IRS proposes a change in the tax return of a taxpayer because it found that the submitted information does not match the information captured in their records. The notice is sent before the IRS assesses a taxpayer for additional types of taxes, such as income tax, estate tax, excise taxes, etc.

A notice of deficiency is triggered when a third-party filer – such as an employer or financial institution – submits information including expenses, income, or a different tax amount to the IRS on behalf of a taxpayer, and the information does not correspond to the information reported by the taxpayer.

Once the information is received, the IRS adjusts the amount of tax due according to the information provided by the third-party filer. The notice of deficiency acts as the first step in reconciling the information deficiency in the IRS taxpayer records.

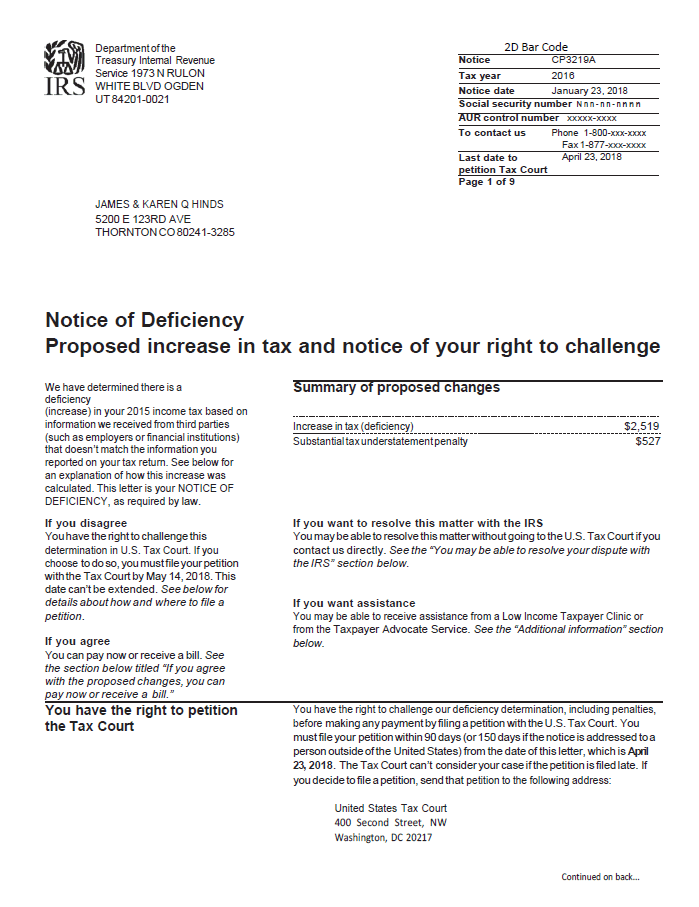

IRS Notice CP3219A is the official name of the notice of deficiency, and it breaks down how the amount of deficiency was calculated and any adjustments that the IRS proposes to make to the taxpayer’s tax return. Usually, before sending the notice of deficiency, the IRS sends Notice CP2000, which is a pre-notification of the discrepancy between the information reported by a taxpayer and the information submitted by a third party.

If the taxpayer fails to respond to the pre-notification, the IRS mails Notice CP3219A with detailed information on how the additional tax was calculated and the adjustments to be made.

The notice is sent when the taxpayer reported or paid the wrong amount of taxes, and the IRS provides a breakdown of the amount of taxes that they owe the IRS. The notice does not always lead to additional taxes, and the IRS may determine that the taxpayer over-reported their income, and the IRS owes the taxpayer a refund.

A notice of deficiency allows the taxpayer 90 days from the date when the notice is sent to dispute the tax assessment in the tax court. Before the 90 days expire, the IRS is barred from initiating any collection activity or assessment for the owed taxes. The notice of deficiency must state the last day when a petition must be filed with the tax court.

IRS Form 5564 is included when the federal tax agency sends the IRS Notice CP3219A. The form is known as a Notice of Deficiency Waiver, and it is used when the taxpayer has no objection to the IRS proposal. If the taxpayer agrees with the IRS proposal, they are required to sign the waiver and mail it to the IRS.

If the taxpayer does not sign the waiver form or file a petition with the tax court within 90 days, the IRS will assess the additional taxes, penalties, and interests indicated in the Notice of Deficiency and send a tax bill to the taxpayer.

If a taxpayer agrees with the IRS proposal but possesses additional information, such as income and expense claims, they are required to amend the original tax return using Form 1040-X.

Listed below are a few options that a taxpayer can take when they do not agree with the IRS proposal:

The first option is to dispute the claim by submitting a petition to the tax court within 90 days from the date when the notice of deficiency is mailed. The tax court is required to reassess the tax liability proposed by the IRS. During the review period, the IRS is barred from assessing the taxpayer or enforcing the collection of tax debts.

The taxpayer can also dispute the tax proposal by providing the IRS with a written statement when filing an appeal. The written statement should include additional information that supports their case, including records of incomes and expenses for the tax year.

The taxpayer can also ask the third party that provided the information – such as an employer or financial institution – to file amended records that indicate the correct information about the taxpayer’s income for the year.

The taxpayer can also call the IRS using the number indicated on the notice to talk directly with an IRS representative. They can ask questions on why they received the notice and provide information for incorrect reporting on the tax return.

However, providing the information over the phone is not enough, and the taxpayer will still need to provide the information by mailing a signed written statement explaining their disagreement with the proposal.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: