Get In-Demand Finance Certifications

Sum of Years Depreciation (SYD)

An alternative accelerated depreciation method

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

What is Sum of Years Depreciation (SYD)?

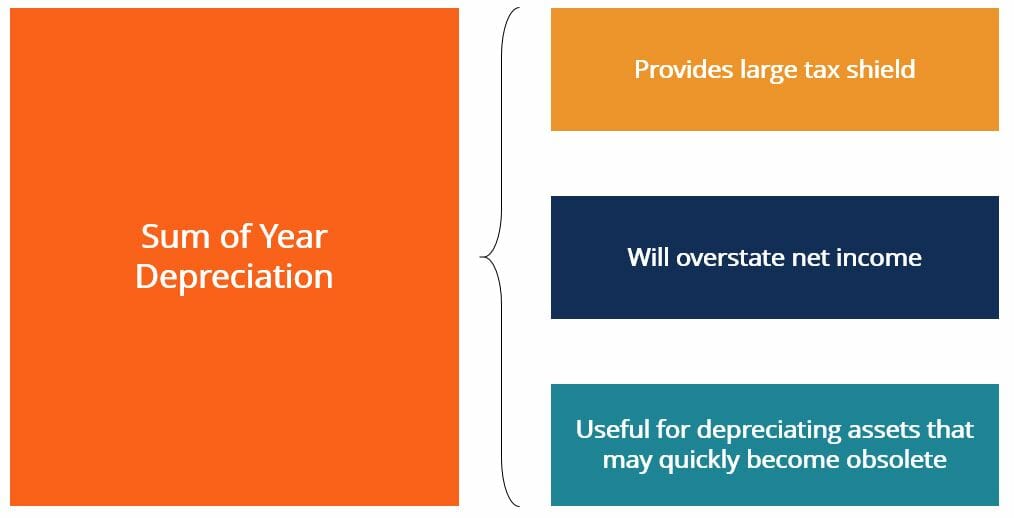

Sum of Years Depreciation (SYD) is a method of accelerated depreciation. Similar to the double declining balance method, sum of years depreciation aims to depreciate a company’s assets at an accelerated rate. Companies may choose the SYD method as the practice will result in a larger depreciation tax shield in the first few years of the asset’s life.

Organizations that face difficult tax environments may choose to depreciate their assets in an accelerated way in order to realize larger tax savings and benefit from the resulting understated net income figure shown on the company’s financial statements in the first few years of owning the assets. In later years, when the depreciation amount is smaller, the net income will be overstated.

The sum of years method of depreciation is also popular with firms that are looking to write off equipment that has a high probability of becoming obsolete before the salvage value is reached. For example, a company may choose this method to depreciate assets such as computers, which may become obsolete very quickly given the rate of technological advancements in the world today.

How It Works

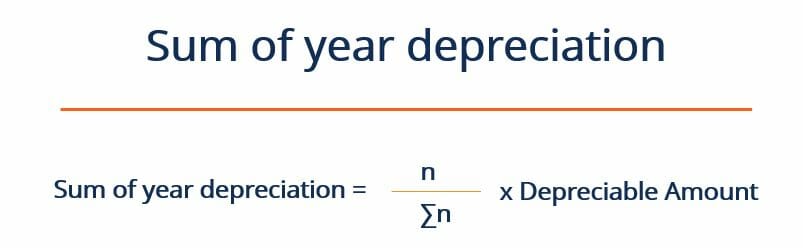

The sum of years depreciation method works by depreciating the asset’s depreciable amount by a depreciation factor unique to each year. The depreciable amount is equal to the asset’s total acquisition cost less the asset’s salvage value. The total acquisition cost refers to the total capital expenditure that the company had to undertake in order to gain possession of said assets.

The total cost would include the purchase price of the asset, any shipping costs associated with moving the asset to the company, and any installation costs. The depreciation factor is the useful life of the asset (in years) divided by the sum of all the useful years. The formula below summarizes the process:

Where:

- n – Useful life of the asset (ex. 4 years)

- ∑n – Sum of years (e.g., 4 years: 1+2+3+4 = 10)

- Depreciable amount – (Total Acquisition Cost – Salvage Value)

Sum of Years Depreciation Example

Consider coffee company Mega Coffee, which is ready to expand into its new office headquarters. The company is considering investing in the latest available computers in order to make sure that its business runs smoothly. The material cost of all the computers is $2,500,000.

However, Mega Coffee needs to pay $100,000 in shipping costs in order to move this massive order of computers across the country in due time. In addition, Mega Coffee is faced with a $400,000 installation charge to ensure that its computers are installed correctly and function at full capacity.

Mega Coffee believes that at the end of the computers’ 5-year useful life, they will be worth $200,000. The company decides to depreciate the assets using the SYD method as it faces a fairly harsh tax environment. Also, there is a high probability that the computers will become obsolete before their useful life is up. Create a depreciation schedule to model how these assets can be depreciated.

Solution

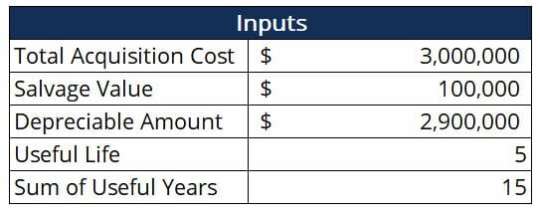

The first step is to identify the main inputs needed for this calculation. These are summarized in the table below:

Where:

- Total acquisition cost – $2,500,000 + $100,000 + $400,000 = $3,000,000

- Depreciable Amount – $3,000,000 – $100,000 = $2,900,000

- Sum of useful years – 1+2+3+4+5 = 15

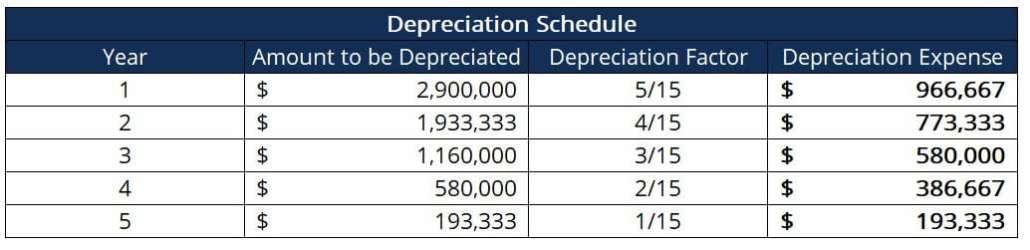

Once we have established the relevant parameters, we can calculate the depreciation expense for each year as follows:

Notice how the depreciation expense in year 1 ($966,667) is about five times greater than the depreciation expense in year 5 ($193,333). Thus, if the computers were to become obsolete after year 3, a huge part of their value would have already been depreciated. It means that the company would have already realized most of the tax benefits associated with depreciation, and thus would be more inclined to invest in more advanced technology.

Additional Resources

Thank you for reading CFI’s guide to Sum of Years Depreciation (SYD). To learn more about related topics, check out the following CFI resources:

0 search results for ‘’

People also search for:

excel

Free

free courses

accounting

ESG

Balance sheet

wacc

Explore Our Certifications

Resources

Popular Courses

Recent Searches