Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

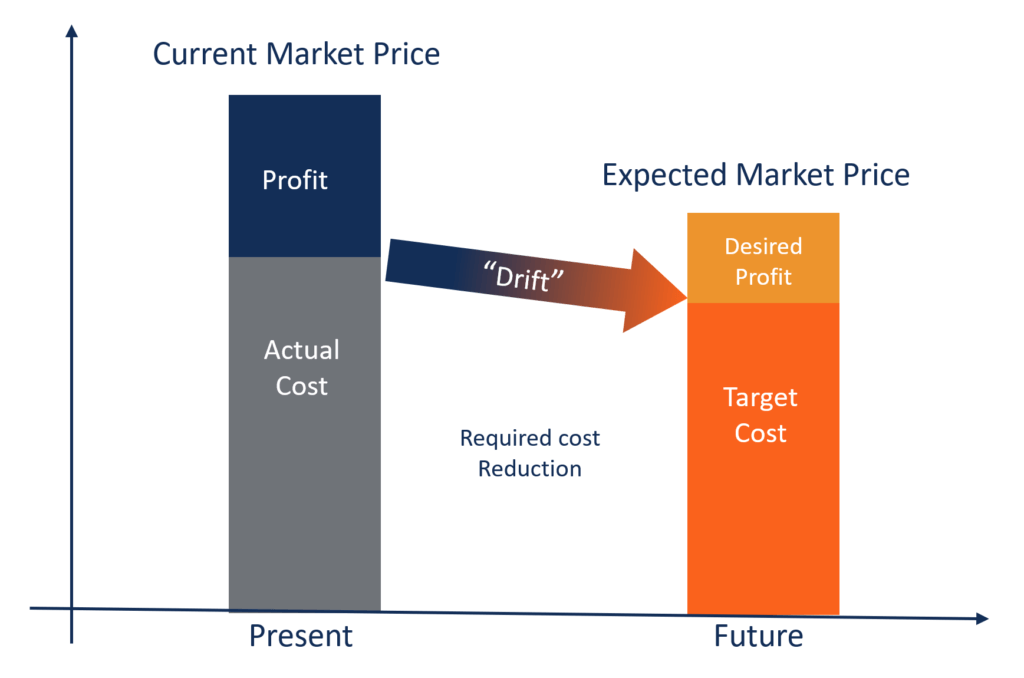

Setting targets for costs according to market conditions

Target costing is not just a method of costing, but rather a management technique wherein prices are determined by market conditions, taking into account several factors, such as homogeneous products, level of competition, no/low switching costs for the end customer, etc. When these factors come into the picture, management wants to control the costs, as they have little or no control over the selling price.

CIMA defines target cost as “a product cost estimate derived from a competitive market price.”

In industries such as FMCG (Fast Moving Consumer Goods), construction, healthcare, and energy, competition is so intense that prices are determined by supply and demand in the market. Producers can’t effectively control selling prices. They can only control, to some extent, their costs, so management’s focus is on influencing every component of product, service, or operational costs.

The key objective of target costing is to enable management to use proactive cost planning, cost management, and cost reduction practices where costs are planned and calculated early in the design and development cycle, rather than during the later stages of product development and production.

ABC Inc. is a big FMCG player that operates in a very competitive market. It sells packaged food to end customers. ABC can only charge $20 per unit. If the company’s intended profit margin is 10% on the selling price, calculate the target cost per unit.

Target Profit Margin = 10% of 20 = $2 per unit

Target Cost = Selling Price – Profit Margin ($20 – $2)

Target Cost = $18 per unit

Click the button below to download our free Target Costing template!

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Target Costing. If you’re interested in advancing your career in corporate finance, these CFI articles will help you on your way:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: