Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An accounting method that records costs after a good is sold or a service is completed

Backflush costing is an accounting method that records costs after a good is sold or a service is completed. Backflush costing is common among companies that use a Just-in-Time inventory management system. It avoids the costly and complicated reporting of all expenses as they occur, and instead “flushes” all expenses in a single entry once the production process is completed.

Companies will estimate the cost to produce each unit of a particular product, assigning a standard cost per unit. At the end of a production cycle, the number of units produced will be multiplied by the standard cost to determine the expense journal entry. The journal entry will be recorded once at the end of the production cycle.

For example, a manufacturer who estimates a standard cost of $5 per product and produces 1,000 units during the production cycle will make an expense journal entry of $5,000 at the end of the cycle.

Backflush costing is generally used by companies that keep low levels of inventory and experience high turnover in inventory. It is because costs are still recorded relatively close to the day they are incurred. Companies with slow inventory turnover tend to record costs as they are incurred, as the product may remain unsold for a longer duration of time.

The backflush costing method works particularly well, where many different costs go into the production of a good. In such an instance, it can simplify the accounting process significantly. As a result, many manufacturing companies with complex production processes use backflush costing. However, companies that sell more customized products are less suited to a backflush costing method, as the unit cost will vary.

Backflush costing allows companies to easily assign costs to corresponding inventory. Only one journal entry needs to be made at the end of the production process to account for all costs designated to the product. Such a process saves companies time needed to record costs during the production process, which lowers accounting costs.

However, companies with slower inventory turnover often can’t use a backflush costing system, as the cost will be recorded too long after it was incurred. Such a costing method often doesn’t conform to GAAP, and therefore can’t always be used. Additionally, it can make a company more difficult to audit.

If an auditor is trying to determine all of the costs linked to a specific product, backflush costing will not be able to provide the information in enough detail. Companies that use the costing method will typically assign a standard cost to each unit of production. The standard cost can vary from reality and may need to be reconciled in future accounting entries.

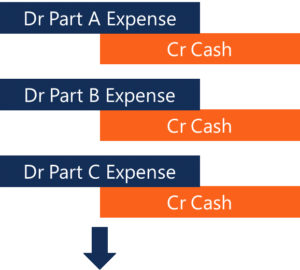

The journal entry for backflush costing is a single entry at the end of the production period based on a standard cost and the number of units produced.

The entry below shows how using other accounting methods can be much more time-consuming. The entries would continue over the life of the production process as costs arise.

A cellular device manufacturer wants to use the backflush costing method to record costs for the development of a new cellphone model. On the first day of the year, they purchase $1,000 of Component A and $500 of Component B. The labor to assemble the phones is $1,000 over the course of the month. The units are shipped to the wholesaler on January 31st.

Using backflush costing, a debit of $2,500 to expenses and $2,500 to cash would be recorded on January 31st.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: