Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Accounting for companies' short-term investments

Trading securities are securities purchased by a company for the purpose of realizing a short-term profit. Companies do not intend to hold such securities for a long period of time; thus, they will only invest if they believe they have a good chance of being compensated for the risk they are taking. A company may choose to speculate on various debt or equity securities if it identifies an undervalued security and wants to capitalize upon the opportunity.

Trading securities purchased by companies are usually securities that are issued within the company’s industry, since these are the securities that industry-leading organizations have the most insight about. Any industry trends or impending news announcements can also influence companies to purchase trading securities.

Trading securities are treated using the fair value method, whereby the value of the securities on the company’s balance sheet is equivalent to their current market value. The securities will be recorded in the currents assets section under the “Short Term Investments” account and will be offset in the shareholder’s equity section under the “Unrealized Proceeds From Sale of Short Term Investments” account.

The Short Term Investments account amount represents the current market value of the securities, and the “Unrealized Proceeds From Sale of Short Term Investments” account represents the cash proceeds that the company would receive if it were to sell the investments at the end of the specified accounting period. The example below assumes that the investments are purchased at the end of the 2017 accounting period:

Changes in the fair value of the trading securities are recorded through journal entries that reflect any increases or decreases in the value of the assets. For instance, in the above example, we see an unrealized loss of $2 billion, as the market value of the trading securities held by the company declined over the course of the holding period.

To account for the change, a company creates journal entries where the loss is debited from a “Trading Securities Market Value Adjustment” account, and credited to the “Unrealized Gain (Loss) On Short Term Investments”. Below is an example of how this may look:

In practice, such journal entries would be completed at the end of the current accounting period that the company is in. In the above example, we assumed that the company’s fiscal year was the same as the calendar year (i.e., beginning on January 1 and ending on December 31). However, it may not always be the case, since companies may opt to follow an accounting year different from the calendar year for any number of reasons, such as seasonality of the business or tax advantages.

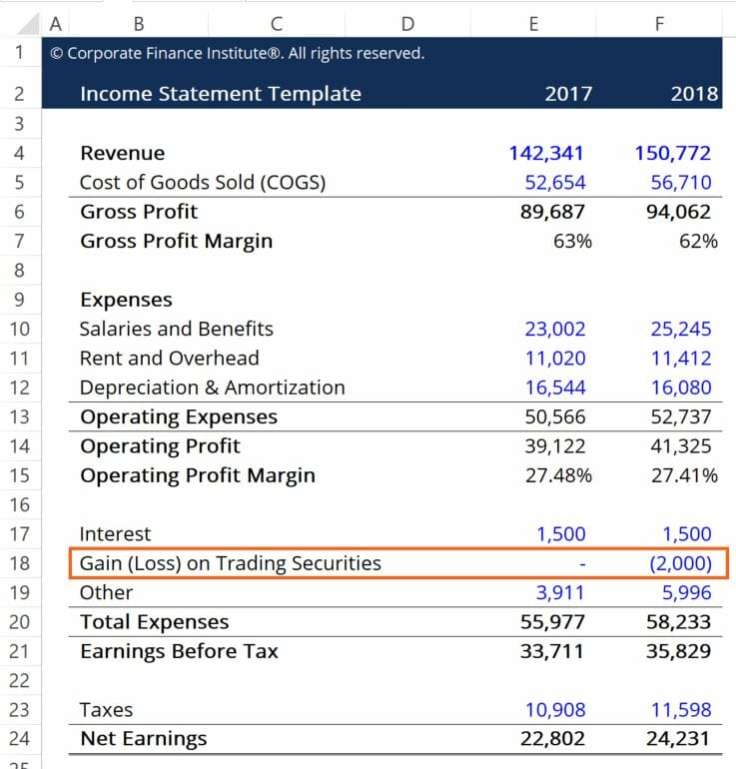

On an income statement, trading securities are recorded at the time of sale. Any gains or losses realized as a result of the securities in question are to be attributed to operating income as a new line item titled “Gain (Loss) on Sale of Trading Securities.”

The gains or losses that are attributable to the trading securities are only recorded at the time of sale since this is when they will materialize. Prior to the sale, the securities can still fluctuate in value – changes that will be captured on the company’s balance sheet. Below is an example of how this would look:

Here, we can see how, in 2017, the investment did not experience any change in value (recall our initial assumption that the investments were purchased at the end of the 2017 accounting period), and that the investments lost value over the course of the 2018 accounting period (as shown by our journal entry).

Thank you for reading CFI’s guide on Trading Securities. To learn more about related topics, check out the following CFI resources: