Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Learn how finance professionals determine the value of a company or asset using structured, proven valuation methods.

In finance, valuation refers to the process of assessing the worth of a company, investment, or asset based on future cash flows, financial statements, and other key indicators. While the stock market reflects current trading prices, valuation focuses on intrinsic value — what something is truly worth based on fundamentals.

Valuation plays a central role in corporate finance, investing, and strategic decision-making. Professionals use various methods to determine whether an asset or business is overvalued or undervalued.

There are many valuation methods, but they all serve the purpose of supporting better business and financial decisions. Common reasons for conducting a valuation include:

Buyers and sellers use business valuation to determine a fair transaction price. It ensures both parties align on value based on the company’s financial standing and future outlook.

A company should only invest in projects that increase its net present value. Companies evaluate potential investments, acquisitions, or expansion strategies by estimating future growth and expected returns. This makes any investment decision essentially a mini-valuation based on the likelihood of future profitability and value creation.

Lenders and investors use valuation to assess a company’s ability to generate future cash flows and service its debt. A credible financial valuation supports funding discussions.

Valuation plays a key role in determining whether a stock or bond is priced appropriately compared to its intrinsic value and comparable assets.

Fair value calculations are required for regulatory compliance, estate planning, and financial reporting.

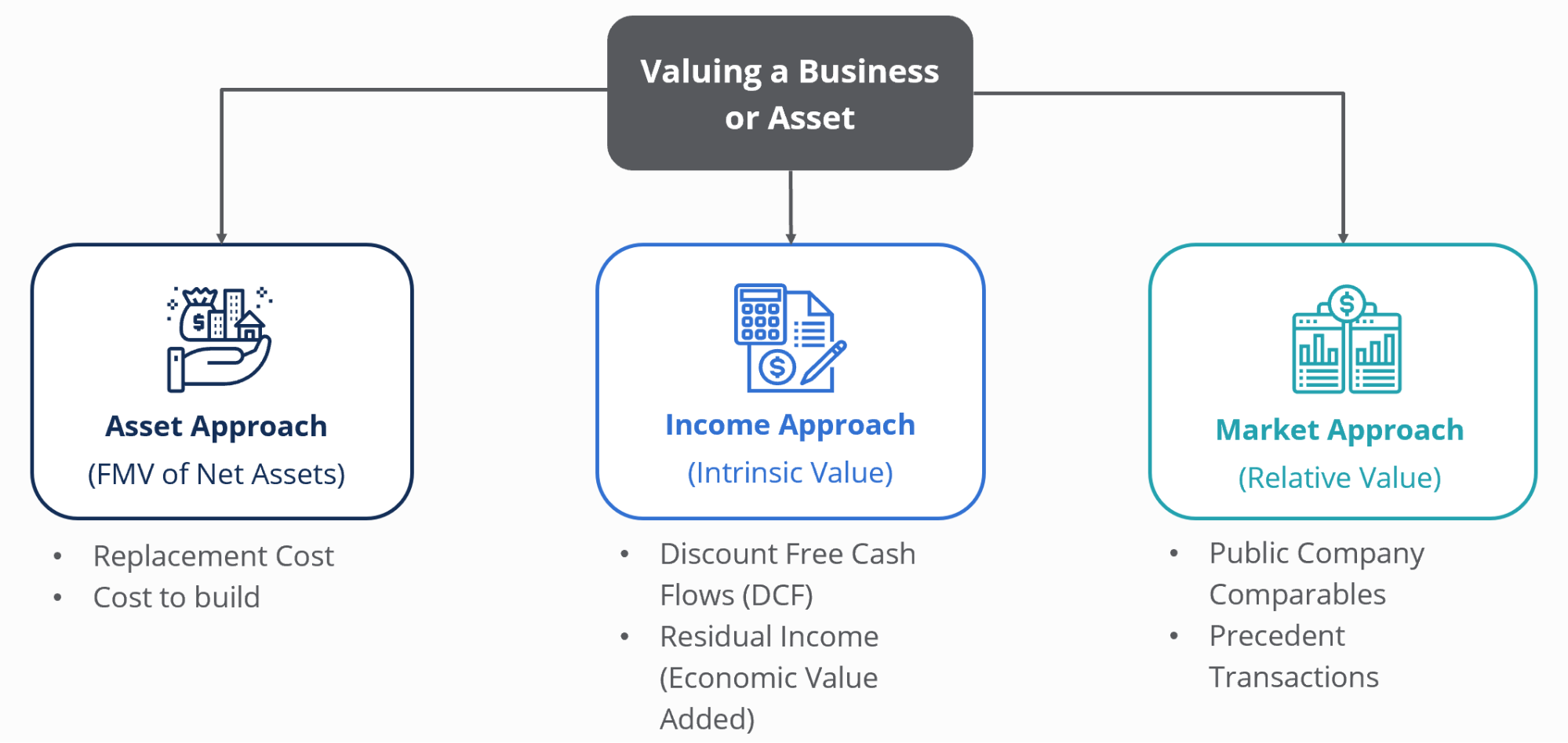

Valuing a company depends on the context, whether it’s for investment, M&A, or internal planning. The three most widely used company valuation methodologies are:

(1) DCF analysis;

(2) Comparable company analysis; and

(3) Precedent transactions.

As shown in the diagram below, when valuing a business or asset, there are three different approaches one can use. These include the asset approach, the income approach, and the market approach:

Discounted cash flow (DCF) analysis is an intrinsic valuation method. It involves forecasting a company’s unlevered free cash flows and discounting them to present value using the firm’s weighted average cost of capital (WACC). The result estimates the company’s intrinsic value.

DCF, also known as discounted cash flow valuation, is one of the most detailed approaches to assessing a company’s future performance.

Comparable company analysis (also called “trading comps”) is a relative valuation method in which you compare the market valuations of similar companies—often referred to as peer companies—to estimate value. Analysts compare multiples like EV/EBITDA or P/E ratios to determine what a business should be worth based on market data.

Comps are effective when similar companies exist and data is accessible, making it one of the most practical business valuation methods.

Precedent transactions analysis is another form of relative valuation where you evaluate the prices paid in recent M&A deals involving similar businesses. These transactions include control premiums and reflect real-world acquisition prices.

Transaction data can provide insight into a company’s fair value in the context of a sale or acquisition.

Analysts often summarize valuation outcomes using a football field chart, which visually compares value ranges across methods such as DCF, comparable analysis, and precedent transactions. Below is an example of a football field graph, which is typically included in an investment banking pitch book.

A football field chart presents a side-by-side comparison of valuation results from different methodologies. It shows the range of values for a company or asset derived from:

The chart helps summarize valuation perspectives in a single visual format, often used in investment banking pitch books and strategic presentations to support decision-making.

As you can see, the graph summarizes the company’s 52-week trading range (it’s stock price, assuming it’s public), the range of prices equity research analysts have for the stock, the range of values from comparable valuation modeling, the range from precedent transaction analysis, and finally the DCF valuation method. The orange dotted line in the middle represents the average valuation from all the methods.

In addition to the primary approaches, analysts may use several other techniques, including:

Many valuation methods may be used together depending on the situation, industry, and availability of data.

A valuation is an estimate of what a business, asset, or investment is worth based on future performance and current financial data.

They are used to support investment, lending, M&A, strategic planning, and tax or legal requirements.

It’s a process used by professionals to estimate economic value and inform decisions about investments and business strategy.

Common approaches include DCF, comparable company analysis, and asset-based valuation methods, each suited to different business types and contexts.

It means applying structured analysis to determine fair value, whether for funding, M&A, internal planning, or compliance.