Actuarial Gains or Losses

Differences between an employer’s actual pension payments relative to the expected payments

What are Actuarial Gains or Losses?

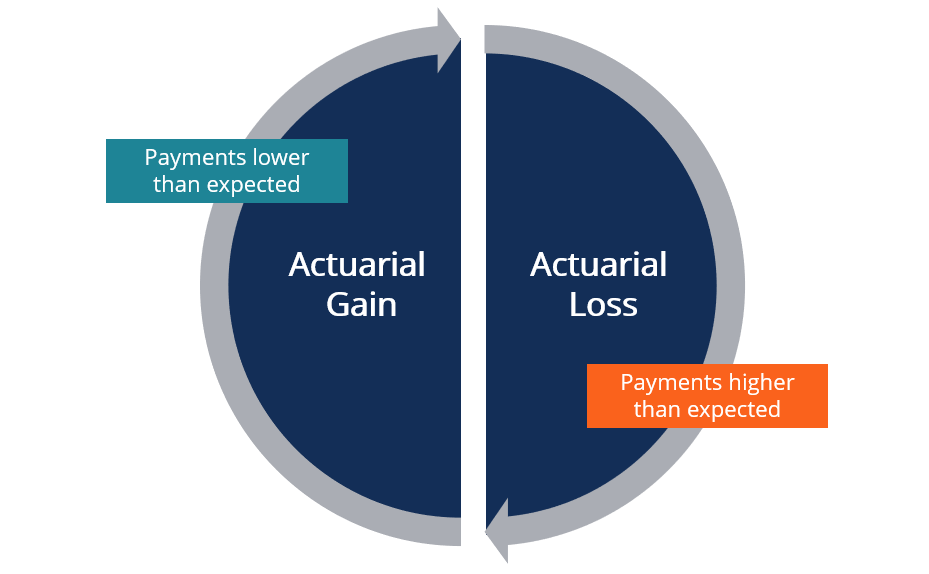

Actuarial gains or losses refer to the differences between an employer’s actual pension payments relative to the expected payments. When the employer’s payments are higher than expected, it is referred to as an actuarial loss.

In contrast, an actuarial gain is when the payments are lower than expected. When actuarial gains or losses occur, employers must make actuarial adjustments to reflect changes to their original pension estimates.

Gains and losses can also arise from adjustments in actuarial assumptions.

Summary

- Actuarial gains or losses refer to the differences between an employer’s actual pension payments relative to the expected payments.

- When the employer’s payments are higher than expected, it results in an actuarial loss. In contrast, an actuarial gain is when the employer’s payments are lower than expected.

- When an actuarial gain or loss is incurred, employers must adjust their estimates in a process known as actuarial adjustment.

Understanding Actuarial Gains or Losses

For many employees, a small percentage of their paycheck is deducted and applied to their pension plans. The pension plan ensures that once an employee retires, they will receive regular pension payments to support their living expenses. Pension plans can vary greatly, with some offering a lump-sum payment at retirement, while other plans provide a lifetime monthly payment.

The payment amount also varies depending on the specifics of the employer’s pension plan. Factors that can affect the payment amount include the individual’s retirement age, annual income, length of contribution, and contribution amount. Often, the employer pension acts as a secondary source of funding in addition to government-provided retirement funds, such as Social Security.

For an employer, the actuarial gain or loss is calculated based on the actual amount that is paid to an employee compared to previous estimates. If an employer pays less than projected, then it incurs an actuarial gain.

For example, actuarial gains can occur if an employee decides to defer their retirement to a later age. In such a case, pension payments that the employer expected to pay out were not paid, resulting in a financial gain for the company.

In contrast, an actuarial loss occurs when the employer pays more than the projected amount. It can occur in instances when employees decide to retire early or a larger number of employees decide to retire than originally projected. In such a case, an employer needs to pay more than originally projected, resulting in a loss. When an actuarial gain or loss is incurred, employers need to adjust their estimates in a process known as actuarial adjustment.

Actuarial Adjustments

Actuarial adjustments are a result of changes to an employer’s expected pension payments. Most commonly, actuarial adjustments are conducted when a company experiences actuarial gains or losses. Typically, companies keep reserves from which pension premiums are paid out. The reserves are based on projections of the pension benefits a company expects to pay out over time.

For example, if several employees decide to retire early, then the corporation would face an actuarial loss as it would be required to pay more in pension benefits than initially projected. In such a case, the corporation would make an actuarial adjustment by increasing its reserves to account for the actuarial loss.

In some cases, actuarial adjustments can affect the employees themselves. In the previous example, employees that retire early may receive decreased pension payments as a result of the employer’s actuarial adjustments.

Accounting for Actuarial Gains or Losses

When actuarial gains or losses occur, a company must adjust its estimated pension payments to present a more accurate projection of its benefit obligations. When the adjustments take place, companies must report their pension obligations and the financial condition of their pension reserves at the end of each annual accounting period.

When accounting for actuarial gains or losses, actuaries take into consideration many factors, such as employee salaries, retirement rates, mortality rates, inflation, and investment returns. The assumptions or factors are accounted for when making actuarial adjustments to an employer’s pension obligations.

When companies adjust for actuarial gains or losses, they must amortize increases or decreases over time such that new changes align with the expected pension payments for current recipients. The disclosure of pension details can also provide investors and regulators with a greater understanding of the financial position of a company.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.