Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The removal of a long-term asset from the company’s accounting records

Asset disposal is the removal of a long-term asset from the company’s accounting records. It is an important concept because capital assets are essential to successful business operations. Moreover, proper accounting of the disposal of an asset is critical to maintaining updated and clean accounting records.

The asset disposal may be a result of several events:

CFI’s Course Accounting Fundamentals shows you how to construct the three fundamental financial statements.

The journal entries required to record the disposal of an asset depend on the situation in which the event occurs.

Let’s consider the following example to analyze the different situations that require an asset disposal.

Motors Inc. owns a machinery asset on its balance sheet worth $3,000.

Motors Inc. estimated the machinery’s useful life to be three years. The annual depreciation expense is $1,000. At the end of the third year, the machinery is fully depreciated, and the asset must be disposed of.

In such a scenario, the asset’s value and the accumulated depreciation must be written off. Initially, the machinery account is a debit account, while the accumulated depreciation is a credit account. To reverse the accounts, the following journal entry must be made:

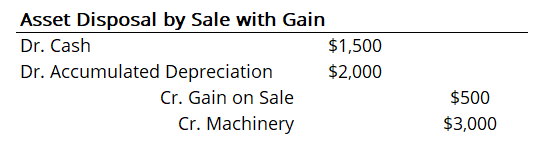

Suppose that at the end of the second year, Motors Inc. decided to sell the machinery to another company. At that time, the accumulated depreciation was $2,000. Therefore, the total book value of the machinery was $1,000 (machinery value minus accumulated depreciation). However, the company agreed to sell the machinery for $1,500. Thus, Motors Inc. must recognize the gain from the sale. The journal entry for the disposal should be:

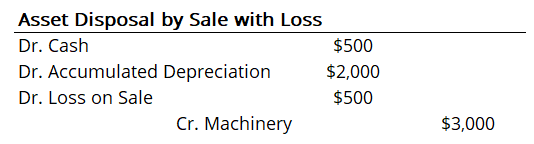

Let’s consider the same situation as in scenario 2, but the selling price was only $500. Thus, there was a loss on the sale. The journal entries should be adjusted accordingly:

The asset disposal results in a direct effect on the company’s financial statements. In all scenarios, this affects the balance sheet by removing a capital asset.

Also, if a company disposes of assets by selling at a gain or loss, the gain or loss should be reported on the income statement.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Asset Disposal. To keep learning and advancing your career, the following CFI resources will be helpful: