Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An asset whose worth is equivalent to its salvage value only for accounting purposes

A fully depreciated asset is an accounting term used to describe an asset that is worth the same as its salvage value. An asset can become fully depreciated in two ways:

If the asset’s accumulated depreciation is equivalent to the asset’s original cost, then it is classified as fully depreciated. If an impairment charge equal to the asset’s cost is incurred, then the asset is immediately fully depreciated.

The depreciation expense for accounting does not fully reflect the actual used value of the equipment. It is more of an approximation that gives an estimate of the actual value used. For this reason, there are different methods to estimate the depreciation expense.

When using more conservative accounting practices, it is typical to impose a more aggressive depreciation schedule and recognize expenses earlier. Sometimes, a fully depreciated asset can still provide value to a company. In such a case, the operating profits of a company will increase because no depreciation expenses will be recognized.

Whenever the asset is no longer used by a company or is sold, the asset is removed from the company’s balance sheet.

Since property, plant, and equipment (PP&E) and accumulated depreciation are balance sheet items, the full depreciation of an asset will affect the company’s balance sheet. At the same time, the income statement is impacted because that is where the depreciation expense is recorded. There are two cases for accounting reporting for fully depreciated assets: the fully depreciated asset is still in production use or it is disposed of.

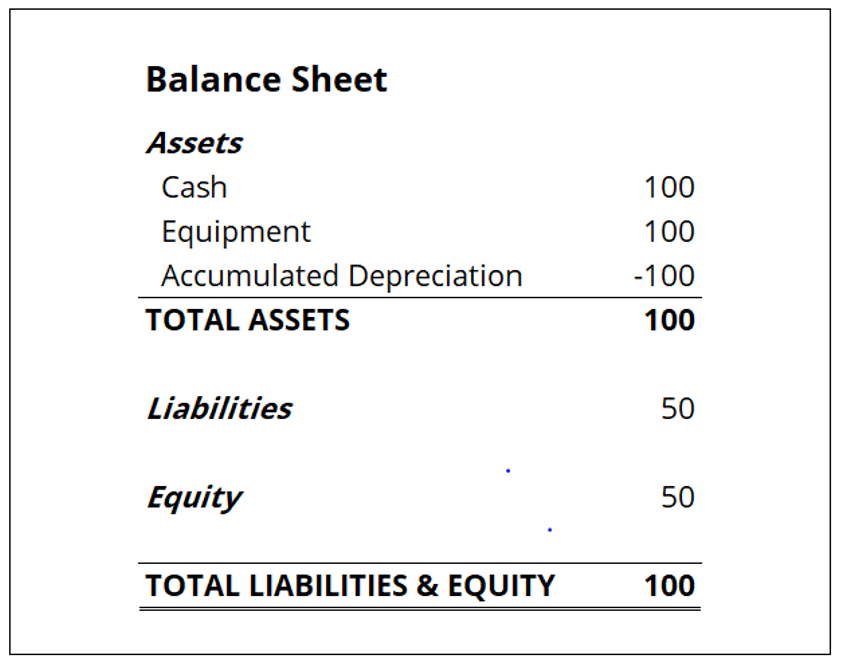

If the asset is still used in the company’s operations, the asset’s account and accumulated depreciation will still be reported on the company’s balance sheet. The reported asset’s value and accumulated depreciation will be equal, but no entry will be required until the asset is disposed of. On the income statement, the operating profit is likely to increase because the depreciation expense will no longer be recorded on the income statement.

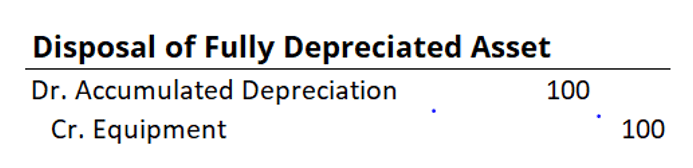

If the fully depreciated asset is disposed of, the asset’s value and accumulated depreciation will be written off from the balance sheet. In such a scenario, the effect on the income statement will be the same as if no depreciation expense happened.

The accounting treatment for the disposal of a completely depreciated asset is a debit to the account for the accumulated depreciation and a credit for the asset account.

Thank you for reading CFI’s guide to Fully Depreciated Asset. To advance your career, check out the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: