Balloon Payment

A large payment that is due at the end of a loan term

What is a Balloon Payment?

A balloon payment, simply put, is a large payment that is due at the end of a loan term. It is different from a fully amortized loan, where a loan is paid back in small but equal payments.

Balloon Loan vs. Fully Amortized Loan

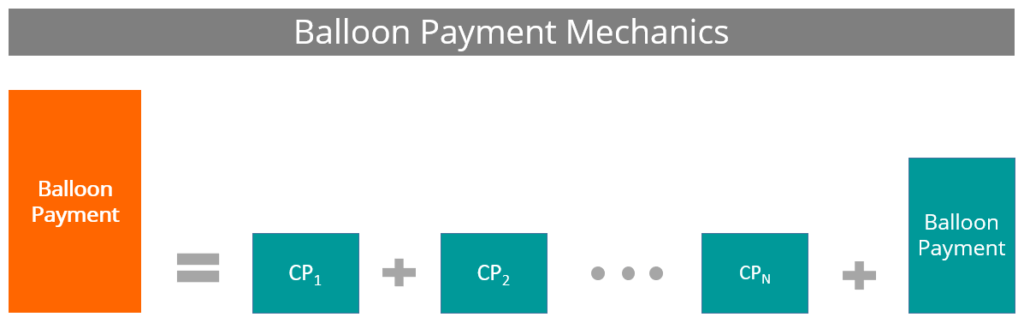

A balloon loan comprises a stream of constant payments followed by a large payment at the end, which is called the balloon payment. In contrast, a fully amortized loan is composed of equal payments, which are paid throughout the life of the loan. The balance at the end of the payments, in such a case, is zero.

Given a similarly sized loan, the constant payments in a balloon loan structure are smaller than those in a fully amortized loan. It is the key benefit of balloon loans.

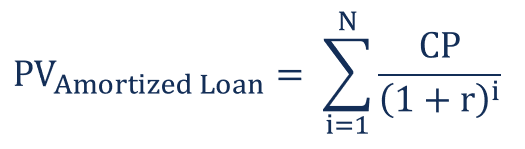

Where:

- CP = Constant payment

- BP = Balloon payment

- N = Number of payments

- r = Discount rate

Where:

- CP = Constant payment

- N = Number of payments

- r = Discount rate

An Application of the Balloon Loan

The balloon loan can be used as an important tool in financial management. Consider an example of a small business that plans to develop a new product. The development requires an investment and will not yield cash flows in the initial years. Using a balloon loan, in such a case, will reduce the financial burden of the business during the development phase since their initial payments are lower.

As the business moves out of the development phase and grows, it can generate sufficient cash flows to service the balloon payment at the end of the loan. It also helps in financial planning, as payments can be modified to meet the current financial conditions of the business.

Calculating the Balloon Payment

We can easily perform balloon payment calculations in Excel. There are two ways of going about the calculation:

Method 1: Given a balloon payment, calculate constant payments.

Method 2: Given a constant payment, calculate the balloon payment.

The choice of the method depends on the certainty of cash flows. For example, if someone is certain about the short-term, then method 2 can be used to determine the balloon payment based on the knowledge of payments.

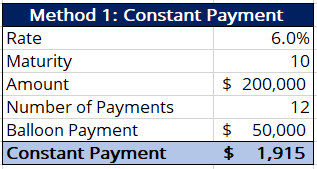

Example: Method 1

Information

- Rate = 6%

- Loan amount = $200,000

- Term = 10 years

- Payment frequency = Monthly

- Balloon payment = $50,000

Constant Payment = PMT(r = 6%/12, nper = 12*10, pv = -200,000, fv = 50,000)

Constant Payment = $1,915

Example: Method 2

Information

- Rate = 6%

- Loan amount = $200,000

- Term = 10 years

- Payment frequency = Monthly

- Constant payment = $2,000

Balloon Payment = FV(r = 6%/12, nper = 12*10, pmt = 2,000, pv = -200,000)

Balloon Payment = $36,121

Important Relationships

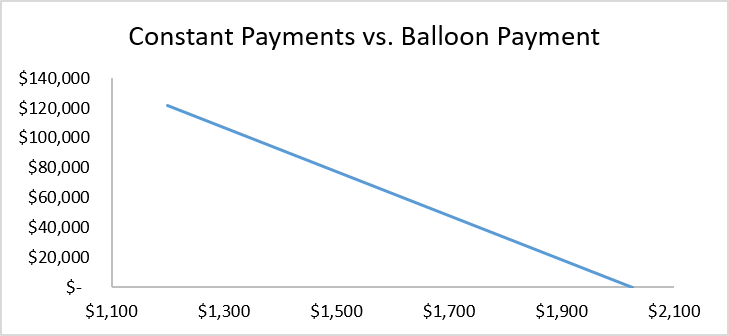

1. Constant Payment

A linear relationship exists between the size of constant payments and balloon payments. As the constant payments go up, the balloon payment falls linearly to zero.

The constant payment, when the balloon payment is 0, is equivalent to the constant payment of an identical fully amortized loan. Hence, a fully amortized loan is a special case of a balloon loan where the balloon payment is equal to zero.

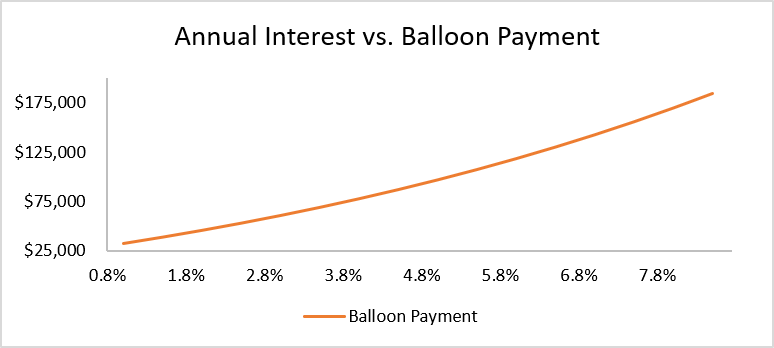

2. Interest Rate

The relationship between the interest rate and the balloon payment is non-linear. It means as interest rates on the loan increase, the balloon payments can become very large. It is important because, at higher interest rates, the reduction in balloon payments requires increasingly higher constant payments, which may affect the financial management of the company.

Both relationships can be seen in the graphs below:

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: