Loan Features

The main features of loans include: secured vs. unsecured, amortizing vs. non-amortizing, and fixed-rate vs. variable-rate (floating)

Loan Features

Loans come with different features that can change the security of the loan, the payments on the loan, and the interest rate of the loan. The main features include secured versus unsecured loans, amortizing versus non-amortizing loans, and fixed-rate versus variable-rate (floating) loans.

Secured vs. Unsecured Loans

One loan feature looks at how secure the loan is. In secured loans, the borrower pledges their own assets (called collateral). If the borrower defaults on their loan, indicating that they’re unable to pay their financial obligations, the lender can then use the collateral as a payment for the borrower being unable to repay the loan. Secured loans usually have a lower interest rate since they’re considered to be safer than unsecured loans since collateral can offset the risk of default.

An unsecured loan is given to a borrower who is deemed to be creditworthy and does not require the borrower to pledge assets for collateral. The interest rate offered is typically higher since the risk is usually higher for the lender (if the borrower defaults, there are no assets being pledged which can repay the lender).

Secured Loan Example

An example of a secured loan would be a mortgage where the borrower’s house is used as collateral and may be forfeited if the borrower is unable to pay their mortgage.

Unsecured Loan Example

An example of an unsecured loan would be a line of credit where the borrower is able to borrow money without using collateral.

For more information regarding secured versus unsecured loans, click here.

Amortizing vs. Non-Amortizing

Another loan feature considers the payment structure of the loan.

Amortizing

In amortizing loans, the principal payments are spread out over several periods, which means the principal amount on the loan will decrease with time. The payments can be equal to each period, which would be referred to as equal-amortizing, or they can differ in value. The payment schedule is developed with the intention to have the loan paid off by a certain time.

An amortizing loan decreases the interest expense over the life of the loan since the principal balance is decreasing, resulting in paying interest on a smaller loan amount.

Example

An example of an amortizing loan could be a mortgage. The principal of the loan (the entire amount you borrowed to purchase the property) is slowly paid off each period along with the interest expense (the expense you pay for borrowing the money).

Non-Amortizing

Non-amortizing loans require regular payments, but the payments do not include the principal balance. The principal is paid in full at the end of the loan period.

A non-amortizing loan requires lower monthly payments since the principal is not included in the regular payments. It results in the final payment being much larger since the principal hasn’t been paid off.

Example

An example of a non-amortizing loan could be a credit card. Only the minimum payment is required, which means there is no fixed payment for the amount borrowed or the interest accrued. The statement balance of the credit card can be paid off in full, which could be thought of as the principal balance.

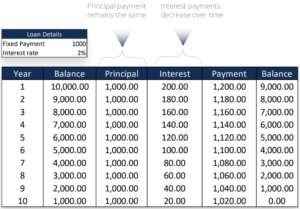

Figure 1 showcases an equal-amortizing loan where the interest expense and a portion of the principal are factored into the “Payment” column. It’s evident that the payments are reducing each period since there is less principal to pay interest on.

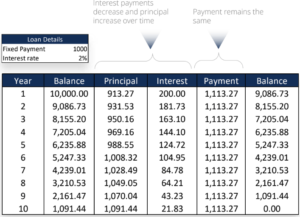

Figure 2 shows a different loan structure where the ‘Payment’ column is unchanged each period. Interest payments decrease over time while principal payments increase.

To learn more about amortization, click here.

Fixed-Rate vs. Variable-Rate (Floating)

The type of interest rate applied to the loan is also considered a loan feature. For fixed-rate loans, the interest rate stays the same and does not fluctuate over the lifetime of the loan. In contrast, a variable-rate loan, also called a floating-rate loan, follows a reference rate that fluctuates over time.

Fixed-Rate

Fixed-rate loans protect the borrower from rising interest rates since they won’t adjust upward if the reference rate were to increase. In addition, fixed-rate loans are worse for the borrower if the interest rate falls. For example, if the rate is 5% and the reference rate falls, the borrower must continue to pay the 5% instead of the lower rate.

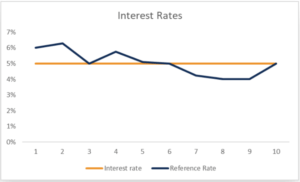

As shown in Figure 3, the fixed-rate loan stays at 5% regardless of the changes to the reference rate.

Variable-Rate (Floating)

A variable-rate loan protects the borrower from falling interest rates because the loan rate will adjust downward with the reference rate. In contrast, this type of loan is worse for the borrower if the interest rate rises since their loan payments will increase in value (due to the reference rate increasing, resulting in a higher interest rate being paid).

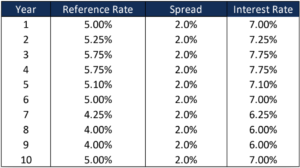

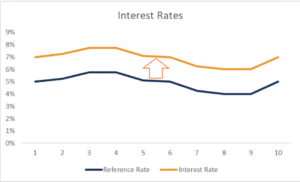

Figure 4 demonstrates how variable-rates can fluctuate. The rate is compared to a reference rate that is then adjusted.

Figure 5 shows how a variable-rate can move, depending on the reference rate. An example of a reference rate could be a recognized benchmark rate, such as the prime rate.

Additional Resources

CFI provides an abundance of course material, including the Financial Modeling Valuation Analyst (FMVA)® certification. Feel free to check out the following resources!

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.