Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

How "worthy" or deserving an individual or a company is of credit

Creditworthiness, simply put, is how “worthy” or deserving one is of credit. If a lender is confident that the borrower will honor her debt obligation in a timely fashion, the borrower is deemed creditworthy. If a borrower were to evaluate their creditworthiness on her own, it would result in a conflict of interest. Therefore, sophisticated financial intermediaries perform assessments on individuals, corporates, and sovereign governments to determine the associated risk and probability of repayment.

Financial institutions use credit ratings to quantify and decide whether an applicant is eligible for credit. Credit ratings are also used to fix the interest rates and credit limits for existing borrowers. A higher credit rating signifies a lower risk premium for the lender, which then corresponds to lower borrowing costs for the borrower. Across the board, the higher one’s credit rating, the better.

A credit report provides a comprehensive account of the borrower’s total debt, current balances, credit limits, and history of defaults and bankruptcies if any. Due to high levels of asymmetries of information in the market, lenders rely on financial intermediaries to compile and assign credit ratings to borrowers and help filter out bad debtors or “lemons.”

The independent third parties are called credit rating agencies. The rating agencies access potential customers’ credit data and use sophisticated credit scoring systems to quantify a borrower’s likelihood of repaying debt. Lenders usually pay for the services, but borrowers may also request their credit score to gauge their worthiness in the market.

A limited set of credit raters are considered reliable, and it is due to the level of expertise and data consolidation required, which is not publicly available. The so-called “Big Three” rating agencies are and Fitch, Moody’s, and Standard & Poor’s. These agencies rate corporates and sovereign governments on a range of “AAA” or “prime” to “D” or “in default” in descending order of creditworthiness.

Outlook assessments are also provided to indicate future credit ratings, and they can be “positive,” “stable”, or “negative.” A “positive” assessment means the agency is hopeful of upgrading one’s rating, and vice-versa, while “stable” denotes no change.

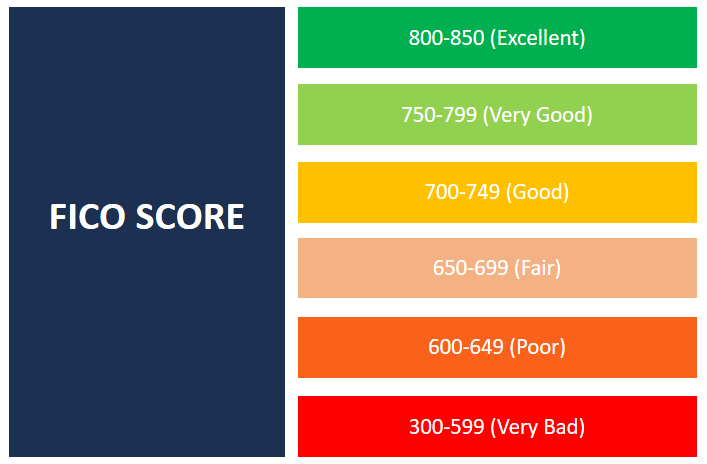

An applicant for a credit card or housing loan may be required to present their credit score at their bank. Credit scores express the same data as ratings, except numerically. A common standard is the FICO score, which consolidates data from credit reporting bureaus – namely Experian, Equifax, and TransUnion – and calculates an individual’s score.

Weights are assigned to key aspects of creditworthiness, which are then used to determine the overall score. They include an individual’s default history, length of said history, total borrowed amount, etc. FICO scores range from 300 – 850, which are grouped into blocks of “Excellent,” “Good,” “Fair,” and “Poor.” Typically, scores above 650 symbolize a good credit history. Borrowers with a score below 650 face a tough time accessing finance, and if they do, it’s usually not at favorable interest rates.

In cases of sovereign borrowers, i.e., national and state governments, ratings are assigned to signify the strength of an economy. Institutional effectiveness, foreign reserves, economic structures, fiscal flexibility, monetary policy, and growth prospects are some of the key factors used to determine their rating. Sovereign ratings impact a country’s ability to borrow internationally, as foreign investors get an idea of the risk associated with government-backed securities.

A poorly rated, undeveloped country may face problems as they may need to pay a higher cost of capital while borrowing for social expenditure. Moreover, poorly rated countries will need to promise a higher rate of return on government bonds in order to convince investors to buy them. Conversely, a higher rated country may be more attractive to foreign investors, which can lead to a cycle of higher economic growth and a further increase in creditworthiness.

Sovereign ratings fluctuate due to political changes. For example, after the announcement of the Brexit referendum in 2016, credit rating agency Moody’s changed the United Kingdom’s outlook in preparation for a prolonged period of uncertainty. Agencies also act as warning systems during a global economic downturn, as they may downgrade countries and deter investors from undertaking risky ventures.

However, the efficiency of the Big Three was questioned following their failure to warn investors in the lead-up to the Asian Financial Crisis in 1997. Moreover, a cautionary downgrade may worsen the economic stability of a country. For example, during the 2010 European Sovereign Debt Crisis, the S&P ratings for Greece and Portugal aggravated the crisis.

Ratings are issued not just to individual entities but also to short-term and long-term debt obligations. The types of debts include asset- and mortgage-backed securities and collateralized debt obligations.

The Big Three agencies were highly criticized in 2008 due to their failure to accurately evaluate the exposure of subprime mortgages in the USA, which eventually triggered the 2008-2009 Global Financial Crisis. Due to the aforementioned reasons, agencies are held responsible for losses accruing as a result of false or inaccurate ratings. There is also an emphasis on transparency since individual agents may try to skew a credit report.

CFI offers the Commercial Banking & Credit Analyst (CBCA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below: