Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A measure of the probability that loan payments will default within a given period, usually one year

Expected Default Frequency (EDF) is a credit measure that was developed by Moody’s Analytics as part of the KMV model. EDF measures the probability that a company will default on payments within a given period by failing to honor the interest and principal payments, usually within a period of one year.

The term “Expected Default Frequency” is trademarked for the probability of default that was derived from Moody’s KMV model. The KMV model was based on the work of three researchers – Stephen Kealhofer, John McQuown, and Oldrich Vasicek. EDF holds that a company defaults when the market value of its assets declines below its liabilities payable. The EDF model measures credit from a one-year to five-year time horizon.

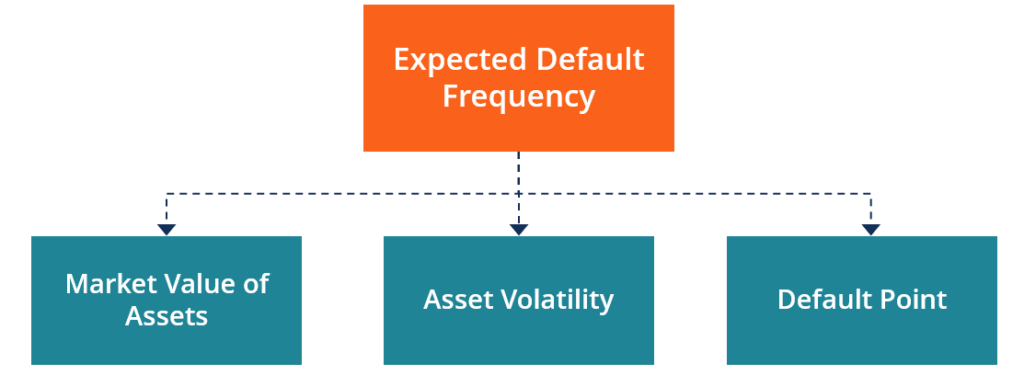

There are three objective factors that determine the Expected Default Frequency measure of a company. They include:

The market value of assets is not a directly observable metric, and Moody’s Analytics developed a model to determine the value. The option-theoretic approach uses the market characteristics of a company’s equity value, as well as the book value of its liabilities, to arrive at the market value of assets. The model treats the equity value of the company as a call option on its underlying assets.

Asset volatility refers to the dispersion of returns of a specific asset (s) owned by a company. Investors view increased volatility as an increase in the risk of investing in specific assets or companies. Volatile assets are considered high risk because their prices are less predictable.

Asset volatility is measured as the standard deviation of returns from the asset or market index. If a company’s assets show higher volatility, there is a greater risk of its value falling below the default, point and investors will be less optimistic about the company’s market value.

Default point is defined as the level of a company’s market value of assets below which it will not be in a position to make scheduled debt payments. The default point is specific to the company being evaluated, and it depends on the company’s liability structure and the value of its assets.

Default probability is the likelihood that a company will not be able to make scheduled repayments over a specified period of time. It provides an estimate of the probability that a borrower will be unable to meet its debt obligations, i.e., principal and interest payments, over a particular time horizon.

The probability of default depends on the borrower’s characteristics, as well as the economic environment. For example, during periods of high inflation, there is a strain on the borrower’s ability to make repayments due to the loss of value of the currency. The default probability of individual borrowers may be determined by looking at their FICO scores, whereas the default probability of business is implied by their credit rating.

The following are the key factors that affect the default probability of a company:

The value of assets refers to the market value of the company’s assets. It is the value that investors would pay to own the asset. In other words, the value of assets equals the current value of future free cash flows generated by the assets and then discounted at the appropriate discount rate.

The asset risk is a measure of the business and industry risk that a company faces. When determining the value of assets, analysts calculate an estimate of the assets based on the fair market value that similar assets would fetch in the market.

Since the value is uncertain, there exists a risk on the asset value, and businesses should measure the asset value in the context of the asset risk.

Leverage occurs when a business uses borrowed funds to invest in its operational activities. Investors use leverage to increase their buying power in the market and amplify the returns obtained from an investment. Rather than issue new shares to raise capital, some entities prefer using debt to finance their activities and increase shareholder value.

A company’s leverage is measured by comparing the market value of assets against the book value of liabilities that it must pay. The default risk increases when the market value of assets declines with an increase in the book value of liabilities.

When the book value of liabilities exceeds the market value of assets, it signals that the value of assets is inadequate to meet future obligations.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: