Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A type of loan with a high loan value relative to the value of the property used as the collateral

A high-ratio loan is a type of loan with a high loan value relative to the value of the property used as collateral. High-ratio loans usually carry higher interest rates than loans with lower ratios. There is no certain standard for high-ratio loans, but loans with LTV exceeding 80% are typically considered high-ratio loans.

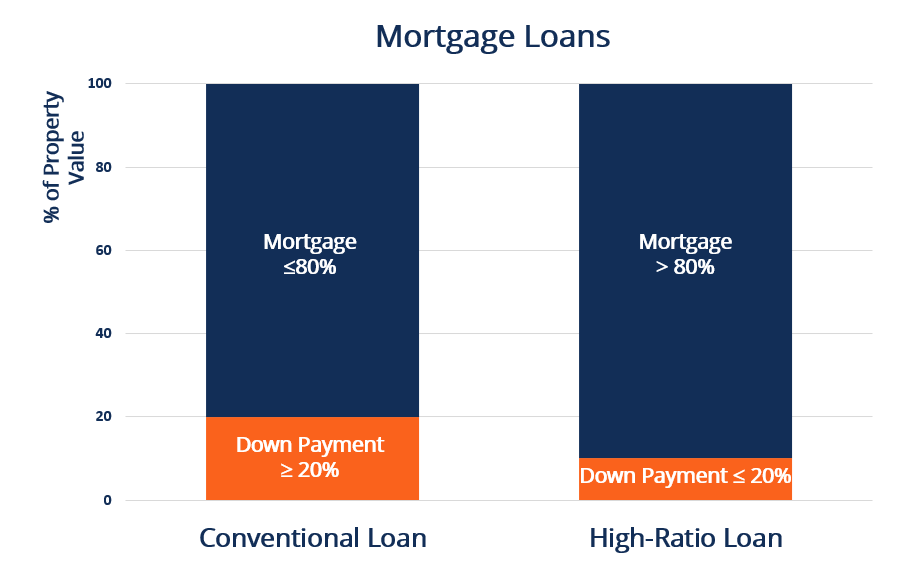

Mortgage loans can be categorized into high-ratio loans and low-ratio (conventional) loans. The ratio here refers to the loan-to-value (LTV) ratio, which is the percentage of the loan amount to the total value of the property purchased and used as collateral.

When the ratio exceeds 80%, the loan is considered to have a high-ratio. High-ratio loans come with a higher level of risk than conventional loans. Thus, lenders usually expect to be compensated with higher interest payments, especially when the borrower’s credit score is low.

Borrowers who cannot afford a large amount of downpayment (conventionally 20% of the property value) need to borrow a high-ratio loan with an LTV ratio above 80%. The Federal Housing Administration (FHA) offers loan programs that make high-ratio loans available to borrowers. The program requires a minimum downpayment of 3.5%. This means that the LTV allowed by the FHA loans can be up to 96.5% (100% – 3.5%).

High-ratio and low-ratio loans are determined by the LTV ratio, which is a commonly used metric to assess credit risk. It is calculated by dividing the borrowing amount by the appraised value of the property.

For example, a borrower plans to make a $300,000 down payment to purchase a house with an appraised value of $1,000,000. The rest, $700,000, will be financed through a mortgage loan. It results in an LTV ratio of 70% (700,000 / 1,000,000), which is lower than the 80% threshold. Thus, the loan can be considered as a conventional loan.

If the borrower plans to make a downpayment of $100,000 for the same house, the LTV ratio increases to 90% with a mortgage amount of $900,000. This brings up the mortgage to the high-ratio loan category.

A higher LTV ratio represents a lower amount of downpayment and a higher level of lending risks. Banks may refuse to lend or ask for a higher interest rate in the case of high-ratio loans.

The highest LTV ratio that a high-ratio loan can reach is 100% theoretically, which means no down payment is made, and all the property will be purchased entirely through borrowing. However, it happens rarely in the real world due to the extremely high credit risk.

Many institutions do not offer mortgages with high LTV ratios. Different institutions impose different upper limits depending on their mortgage program policies. Extra limitations or requirements are usually set for high-ratio loans to mitigate the high risks.

Higher credit scores and private mortgage insurance (PMI) are two common examples. PMI protects the lenders in the case that borrowers default. Borrowers typically must pay premiums for the mortgage insurance when the downpayment is below 20% of the purchase price (high-ratio loans).

Although the premiums for PMI increase the borrowing costs, they offer borrowers who cannot afford a 20% downpayment opportunities to purchase houses. As the mortgage’s been paid down to an LTV ratio below 80%, the mortgage is no longer a high-ratio loan. The borrower is allowed to initiate a PMI cancellation and stop paying the premiums.

In the public sector, FHA offers high-ratio mortgage loans with an LTV ratio up to 96.5%, as mentioned above. However, for the purpose of risk control, the program sets a minimum requirement of credit scores for the higher ratio and requires a mortgage insurance premium (MIP).

Like private sector insurance, borrowers can refinance and remove the MIP when they’ve made regular repayments and brought the LTV ratio below 80%.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: